The Big Idea

Province Buenos Aires | Almost there

This material is a Marketing Communication and does not constitute Independent Investment Research.

There has been of an agreement with the largest bondholder and others on revised restructuring terms from the Province of Buenos Aires. It aligns with Amherst Pierpont’s standing long recommendation, our view of declining deal risk and our expected recovery value near 50. Investors should stay overweight after restructuring. The markets should quickly realize the technical benefits of the BUENOS’37A for its higher average 6.2% coupons and the same asymmetric upside optionality as the sovereign.

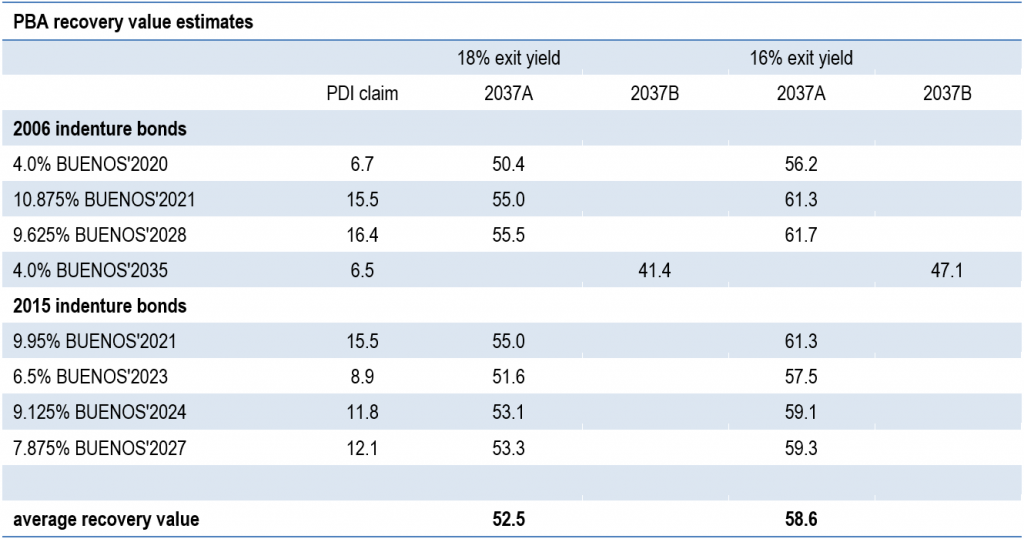

The revised terms offer a 52.5 weighted recovery value at an 18% discount rate, with the Province conceding to higher coupons, a partial past due interest cash payment through June 30 and stronger indentures. The expiration date was again extended through August 13 with prospects for an imminent closure with bondholders. The latest announcements have allowed for knee-jerk 3-point gains in the latter phase of what has been our core recommendation since March 2021 at price lows of 40. Investors should continue holding long exposure for the high implied 18% exit yields. That translates into high current yield with a more carry than the sovereign and with the same asymmetric positive optionality and benchmark $5.3 billion liquidity of the Buenos’37A. These attractive technical attributes could argue for spread convergence to the sovereign for closer to 16% than 18% exit yields or, alternatively, outperformance after the launch of the Buenos’2037A.

Source: https://www.prnewswire.com/news-releases/the-province-of-buenos-aires–agreement-with-certain-bondholders-301338433.html

The deal risk is quickly declining on the agreement with the largest bondholder and others on friendlier terms. It is not clear what the remaining stumbling blocks are after the Province of Buenos Aires conceded to higher average coupons and a partial upfront cash PDI payment. The AdHoc committee statement shows some tension on not having engaged in these latest rounds of discussions and, as such, not having endorsed the revised terms. However, the average recovery value of 52.5 from the latest offer compares favorably to the 51.8 of the June AdHoc counteroffer and near complete agreement to their counter-proposed terms. This does not suggest a protracted stalemate but rather an imminent resolution with Minister Lopez announcing majority acceptance rate above the 66% 2015 CAC thresholds, though not quite reaching the higher 2006 CAC thresholds. There are also coercive incentives to motivate participation for risk of forfeiting PDI. Holders who do not validly tender and consent in the invitation will not receive any PDI, and consenting holders of any series for which the requisite majority is obtained to modify 100% of the series will be entitled to receive a pro rata allocation of the PDI corresponding to the eligible bonds held by non-consenting holders.

There were no last-minute surprises or relative value implications with similar higher percentage recovery value across the curve. The press release suggests an upgrade to a stronger indenture perhaps similar to the 2006 versus 2015 bonds to “strengthen the effectiveness of the contractual framework” that adjusts the documentation to creditor proposals. The PDI cash component was slightly higher at 10% versus the June counterproposal of 9.25% and realignment to almost the same creditor proposed cash stream on coupon payments. The break-through was the previous concession for say a 25% haircut on the average 8.2% coupons opposed to the first offer of a 50% haircut. The single series bond 2037A reaffirms a uniform recovery value with PDI the main differentiation across the bonds. The only exception was the 2035 for exchange into the 2037B for lower 41.4 recovery value.

Investors should stay overweight after restructuring. The markets should quickly realize the technical benefits of the BUENOS’37A for its higher average 6.2% coupons and the same asymmetric upside optionality as the sovereign. The implied 18% exit yields may seem reasonable with a 125 bp spread premium to the similar duration ARGENT’38 and a “Kicillof” risk premium to the interpolated Province of Cordoba curve. However, this translates into a low cash price of 46.9 against restructured provincial bonds of 57-77 and much higher current yield of 8.31% for the Buenos’37A with only Jujuy’27 close at 8.06%. The unrestructured City of Buenos Aires and Santa Fe province also offer high current yield at 7.5%-9.3% but with much higher cash prices of 74 to 94. The 8.3% current yield post September step-up for the Buenos’37A would also quickly increase to 11.2% in 2023 as coupons step up to 5.25% in 2023, 6.375% in 2024 and then stabilizing at 6.625% thereafter.

There is also no comparison for liquidity with a high concentration of the defaulted USD bonds into one single series 2037A for a hefty tranche of $5.3 billion. There is nothing that comes close to that benchmark liquidity among the provinces with a tranche that could rival 10-year and 30-year benchmarks in Colombia and Mexico. The Province of Buenos Aires would still be off-index; however, it would no longer be penalized for its illiquidity while also discouraging short-sellers for its higher relative coupons to the sovereign. The bottom line is that the large size would attract relative valuation comparisons to the sovereign whereby the Province of Buenos Aires provides higher coupons and similar upside optionality on the high correlation to the sovereign. The substitution out of the sovereign and into corporates or provinces has been a successful investment strategy with dominant outperformance of the off-index bonds and the difference between YTD profits versus YTD losses. The performing status of the Buenos’37A could also attract more conservative investors after having cured the default post-restructuring. These attractive technical attributes could argue for spread convergence to the sovereign for closer to 16% than 18% exit yields or alternatively outperformance post launch of the Buenos’2037A.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.