By the Numbers

Cure rates continue to rise in GSE CRT

Chris Helwig | July 23, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Fundamental credit, at least measured by loans rolling out of forbearance, continues to improve across loans referenced in GSE credit risk transfer deals. Nearly two-thirds of loans seriously delinquent last summer have either cured or prepaid through April with that count jumping 15% over the most recently reported three months. Initial concerns that cure rates could fall over time as stronger credits re-performed and weaker credits remained behind seem to have diminished, translating to a strong positive for credit fundamentals across the sector.

Despite improving credit performance, prepayments remain elevated and appear poised to remain so against the backdrop of lower interest rates. So, while nominally large swaths of loans continue to re-perform, that has not necessarily translated to material declines in delinquencies on a percentage basis. Investors in pre-REMIC CRT structures may still be subject to longer lockouts as a result of percentage-based measures employed to calculate cash flow triggers. However, this lockout may be somewhat welcome for holders of premium cash flows with high loss-coverage multiples that are not expected to incur losses; lockout may help insulate against elevated speeds going forward.

Breaking down performance

Through the April remittance, 66.1% of loans referenced in Fannie Mae CAS deals that were seriously delinquent last summer have subsequently cured or prepaid. Cure rates for a comparable population of loans referenced in Freddie Mac STACR deals totaled 68.5% through April and more than 71.3% through May; reporting lags in Freddie Mac deals are one month shorter than those in Fannie Mae transactions.

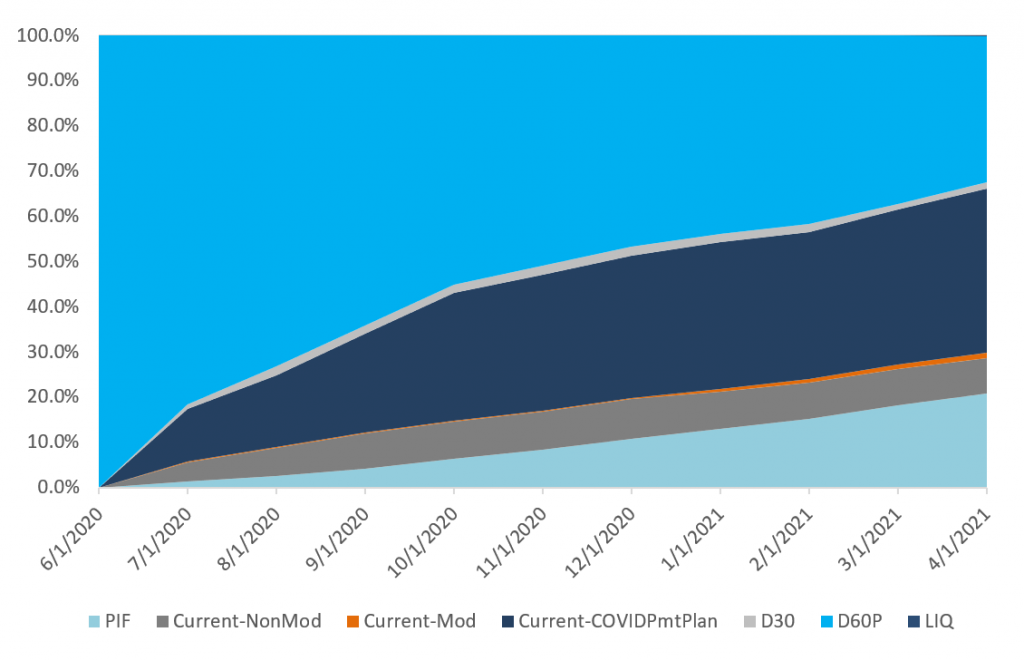

Elevated cure rates appear to be primarily driven by the ability of borrowers to defer arrearages incurred during forbearance to the maturity of the loan. The incidence of deferrals in Fannie Mae reference loans totaled just over 36% with an additional 7.8% of borrowers self-curing. Freddie Mac’s reporting does not distinguish between deferrals and self-cures but they combined to account for 44.6% of delinquent loans that have re-performed (Exhibit 1).

Away from payment deferrals, prepayments were the next largest driver of cures across delinquent loans in both Fannie Mae and Freddie Mac CRT. Over 20% of delinquencies referenced in Fannie Mae CAS transactions cured by prepayment while over 23% of the population of delinquent loans analyzed in Freddie Mac deals prepaid. Given an observation period of just under a year, the analysis suggests that prepayment speeds on loans coming out of forbearance may continue to be upwards of 20 CPR across both cohorts. Conversely, reperformance by modification is extremely muted across both programs as modified loans made up just 1.3% of cures across both programs.

Exhibit 1: Breaking down re-performance across delinquent loans in Fannie Mae CRT

Source: Fannie Mae, eMBS, Amherst Pierpont

Breaking down cures by borrower attributes

Another potential source for optimism around fundamental credit performance across CRT is elevated cure rates even across borrowers with weaker attributes, suggesting that remaining delinquencies are likely not becoming more adversely selected. The most pronounced differences were evident across borrowers’ credit scores with modestly lower cure rates across lower FICO borrowers. Cure rates averaged just over 65.5% across all cohorts analyzed. Lower FICO borrowers modestly underperformed the broader average, but not by much. Borrowers with FICO scores less than 640 have cured at a rate of 56% while borrowers with scores between 640 and 680 have cured at a rate of 58%. Somewhat surprisingly, differences in cure rates across borrowers’ LTV ratios were even more muted. Borrowers with LTVs of 90 or more have cured at a rate of 63% compared to borrowers with LTVs less than 60 who have cured at 67%. Admittedly, these attributes are being viewed in isolation and the analysis does not control for compensating credit characteristics. As a result, pools with larger populations of loans with layered risk may still experience higher default and lower cure rates than those without.

Yet delinquency rates remain elevated on a percentage basis

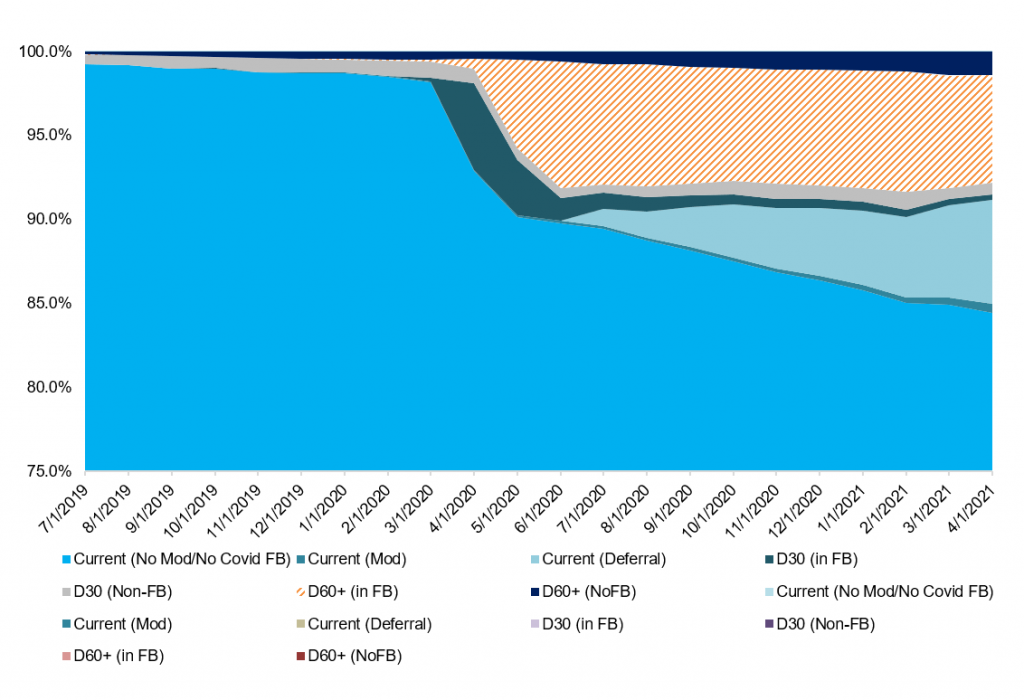

While a majority of loans in forbearance have cured or prepaid across both cohorts as of April, that improvement in credit performance has not amounted to an equivalent improvement in delinquencies measured on a percentage basis. Fast prepayments on deals’ reference pools have outpaced cure rates, in some cases, fairly substantially, reducing the notional denominator faster than loans are curing, keeping percentage delinquency rates elevated. Using the Fannie Mae 2018 vintage as an example, delinquencies on loans in forbearance plans peaked in June of last year at 7.5%. The delinquency percentage on the cohort was as high as 7.2% in February and sits at roughly 6.5% as of April. (Exhibit 2)

Exhibit 2: Percentages of delinquencies on loans in forbearance remain elevated

Source: Fannie Mae, eMBS, Amherst Pierpont

Investment implications

Elevated delinquency rates and longer lockouts may not spell bad news for investors. Investors, particularly those further up in the capital structure in pre-REMIC structures may see longer lockouts as a positive since the lockouts protect IO multiples on premium bonds. The premium bonds otherwise would be curtailed against the backdrop of lower rates and rising prepayment speeds. Pre-REMIC deals do not contain Supplemental Subordination Reduction Amount language, which allow bondholders to receive both scheduled and unscheduled principal irrespective of whether the delinquency trigger is passing as long as the deal meets a total subordination target amount. As a result, mezzanine bonds with higher loss coverage multiples may outperform those in later vintage REMIC structures where elevated delinquency rates do not lock out the structures. Conversely, subordinate investors looking to roll down the credit curve as deals de-lever should continue to favor REMIC structures where deals are passing their SSRA threshold tests.