The Big Idea

El Salvador | Higher financing risks

This material is a Marketing Communication and does not constitute Independent Investment Research.

El Salvador’s Bukele administration may soon reach a crossroads. Some investors had expected financing constraints would force policy pragmatism from the administration and negotiations with the International Monetary Fund would renew in earnest. But the prospects for an IMF program are now probably close to zero. There has been no progress on tackling the weak fiscal finances necessary for an IMF program and no apparent progress on improving US diplomatic relations, which hinge on a credible approach to corruption, improving transparency and strengthen anti-money laundering regulations. The Central American Bank for Economic Integration is providing support, and the country should have sufficient near-term financing through either voluntary or forced local financing. But there is no coherent medium-term financing or solvency plan without an IMF program. The unofficial debate amongst local participants is now shifting towards worst case scenarios including the possible nationalization of the pension funds. This reaffirms our high conviction underweight and target for distressed yields above 10%.

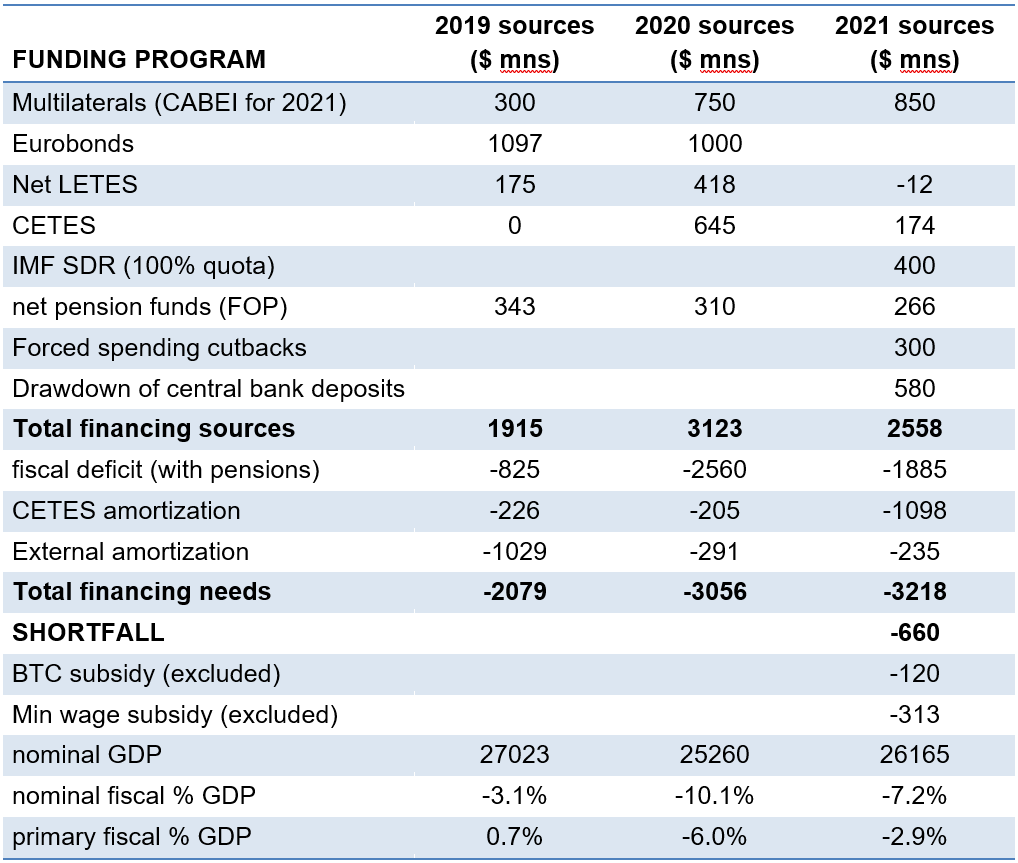

Exhibit 1: El Salvador’s source of funds

Source: https://www.transparenciafiscal.gob.sv/ptf/es/PTF2-Ingresos.html, https://www.laprensagrafica.com/lpgdatos/Ley-Presupuesto-2021–Los-gastos-superan-a-los-ingresos-20210113-0135.html, https://www.bolsadevalores.com.sv/

The consistent underperformance of El Salvador’s Eurobonds shows increasing uncertainty about IMF relations. The market should not underestimate the importance of an IMF program as the gatekeeper to access external credit—either through Washington, DC-based multilaterals or Eurobonds—as well as the anchor for medium-term debt sustainability. The budget now faces an important shortfall with domestic markets saturated and access to external markets restricted. The recently approved $600 million CABEI loan should cover the $646 million September CETES amortization, and the $400 million IMF SDR loan disbursement in August will also provide some budget relief. However, that still leaves an important shortfall, assuming there is regulatory flexibility to shift IMF SDR to budget support. This financing gap also excludes the recent spending commitment for the BTC subsidies ($120 million) and the minimum wage hikes (around $300 million) with still upside risks for BTC public infrastructure.

The obvious alternatives are arrears financing or forced spending cutbacks (around $300 million) and the drawdown of the treasury bank deposits at the central bank ($250 million). There has already been a noticeable cutback in capex spending this year with forced pragmatism probably shifting the full year budget closer to $1.54 billion from $1.885 billion. It is important to remember that you cannot spend what you cannot borrow, so restricted borrowing forces pragmatism to lower the fiscal deficit. The reallocation of the CABEI loans for the maturing CETES will also finance these bulky amortizations and leave much lower rollover and financing risks for the remainder of the year, assuming successful LETES auctions.

The financing stress shifts back to the budget in the fourth quarter of this year after having exhausted the IMF, CABEI loans and residual stock of central bank cash deposits. The next list of alternatives are increasingly heterodox options. Those include revising regulations to voluntarily expand capacity for local funding or quickly shifting to coercive alternatives such as forced local funding if investor sentiment deteriorates. The legislative majority could easily revise regulations that allows for a higher issuance cap for LETES (25% of current revenues) concurrent with a reduction in liquidity requirements. If unable to increase sufficient demand, then typically the strategy shifts to more coercive alternatives. This explains the latest local press headlines about the forced nationalization of the pension funds under the earlier stated official intentions of “reforming” the pension system.

The markets are already discounting higher risk premiums that are near our 10% to 10.5% targets. However, the underperformance may continue with potential for adverse headline shocks and higher policy risks. The heterodox funding alternatives may reduce near-term financing risks, but, similar to Argentina, may worsen medium-term debt sustainability if the alternatives lower foreign investment, lower growth prospects and yet provide no obvious commitment to fiscal consolidation. The initial reallocation of pension funds would provide only temporary support in front of a declining stock of USD liquidity. It will also be critical to monitor if there if any backlash to investor sentiment with dollarization particularly vulnerable to capital flight that may worsen liquidity/rollover risks.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.