By the Numbers

New FHA loan mods should lift Ginnie Mae speeds

Brian Landy, CFA | July 9, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

A new loan modification program from the Federal Housing Administration looks likely to trigger prepayments of some delinquent loans backing Ginnie Mae MBS. Pools with 5% or higher coupons or with six or more years of seasoning look the most vulnerable. MBS servicers started using the new program in late June, so Ginnie Mae MBS could see the prepayment effect as early as July.

The Federal Housing Administration recently added the Advance Loan Modification program, or ALM, as the new first step in the FHA’s loss mitigation waterfall for loans leaving Covid-19 forbearance. The FHA previously screened loans first for its payment deferral program, also known as a partial claim. A loan receiving a partial claim can remain in an MBS pool, but a servicer must buy out a modified loan. The ALM program consequently should increase the number of loans bought out of pools and the consequent prepayments.

To qualify for ALM, the new loan must lower the borrower’s principal and interest payment by at least 25%. Loans with a sufficiently high note rate, sufficient seasoning or both should qualify for the modification. Most loans in 5.5% coupon pools and higher should qualify, while many loans in 5% pools are on the bubble. Loans in 5% pools that are 12 months or more delinquent currently look a little short of the necessary payment reduction. But if interest rates were to drop 25 bp, roughly a third those loans would qualify.

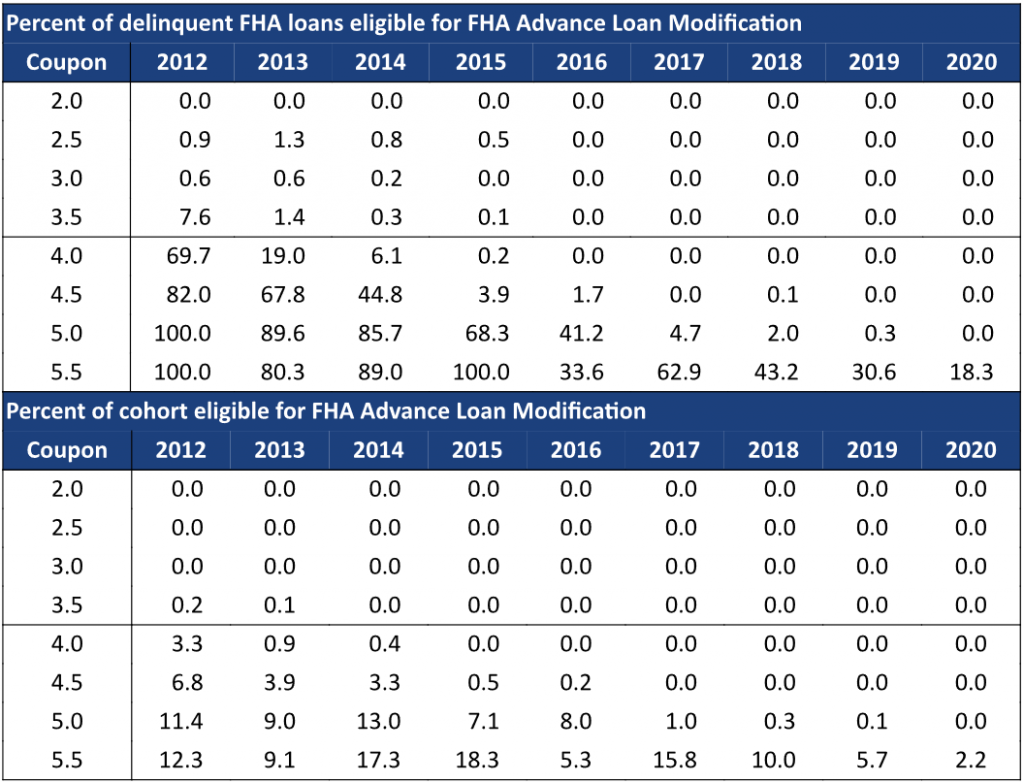

Most of the delinquent FHA loans that currently look eligible for ALM are in high coupons or seasoned pools (Exhibit 1). The top half of the table shows the percent of delinquent FHA loans that would qualify for an ALM assuming a 3% mortgage rate and assuming borrowers use the maximum allowable forbearance. Most delinquent FHA loans in 4% and higher coupon pools originated in 2012 would qualify for ALM, for example. But loans originated after 2016 need to be in a 5.5% coupon pool to achieve a 25% P&I reduction.

Exhibit 1. The ALM targets borrowers with high note rates or seasoning

Percent of delinquent FHA loans and percent of cohort UPB as of 6/1/2021 that would qualify for an Advance Loan Modification assuming maximum use of forbearance and a 3% mortgage rate. Ginnie Mae loan-level data was used to estimate the amount of past-due principal, interest, taxes, and insurance. Taxes and insurance accrue at 12 bp each month.

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities

The change in prepayment speeds depends on the effectiveness of the ALM program and how many delinquent FHA borrowers are in each cohort. This is shown in the bottom half of the exhibit. Delinquency rates generally increase at higher coupons, and the biggest speed increase will come in 5.0% and higher coupons. Some of those cohorts have over 15% of their unpaid principal balance potentially eligible for an ALM. Seasoned cohorts tend to have fewer delinquent loans, so the effect on speeds is reduced. For example, the 4% 2012 and 5% 2015 both have roughly 70% of their delinquent loans qualify for the ALM. But this affects only 3.3% of the UPB in the 4% cohort, compared to 7.1% of the UPB in the 5% cohort.

A larger number of FHA borrowers may ultimately get an ALM. Many borrowers are slightly above the payment reduction threshold and susceptible to small changes in current conditions. Interest rates could fall, or borrowers might use less than the maximum forbearance allowed.

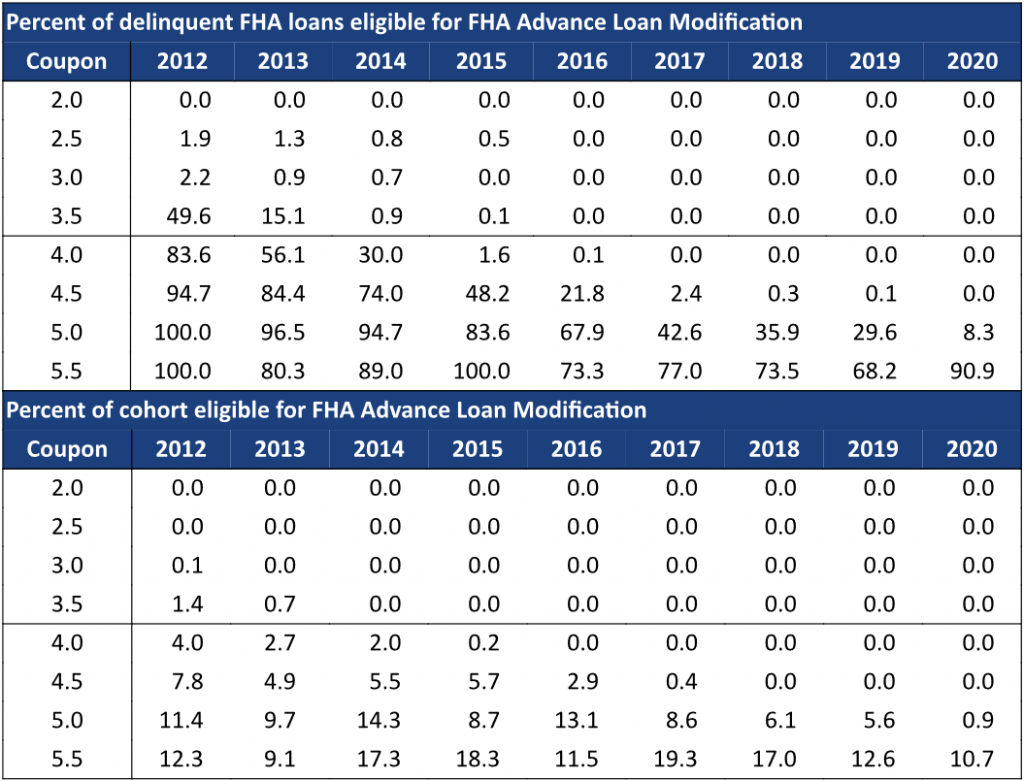

The percentage of loans that qualify for an ALM jumps considerably if mortgage rates fall 25 bp to 2.75% (Exhibit 2). For example, roughly one-third of 2018 and 2019 vintage 5% delinquent loans qualify, compared to less than 2% at the current 3% mortgage rate. Those cohorts contain roughly 100,000 FHA loans, of which nearly 15,000 are delinquent. That is a sizeable number of loans that would become a mandatory buyout. For example, at a 3% mortgage rate only 0.1% of UPB in the 5% 2019 cohort appears likely to receive an ALM. But if mortgage rates fall to 2.75% that jumps to 5.6% of the cohort UPB.

Exhibit 2. More delinquent borrowers can get ALM if mortgage rates hit 2.75%

Percent of delinquent FHA loans and percent of cohort UPB as of 6/1/2021 that would qualify for an Advance Loan Modification assuming maximum use of forbearance and a 2.75% mortgage rate. Ginnie Mae loan-level data was used to estimate the amount of past-due principal, interest, taxes, and insurance. Taxes and insurance accrue at 12 bp each month.

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities

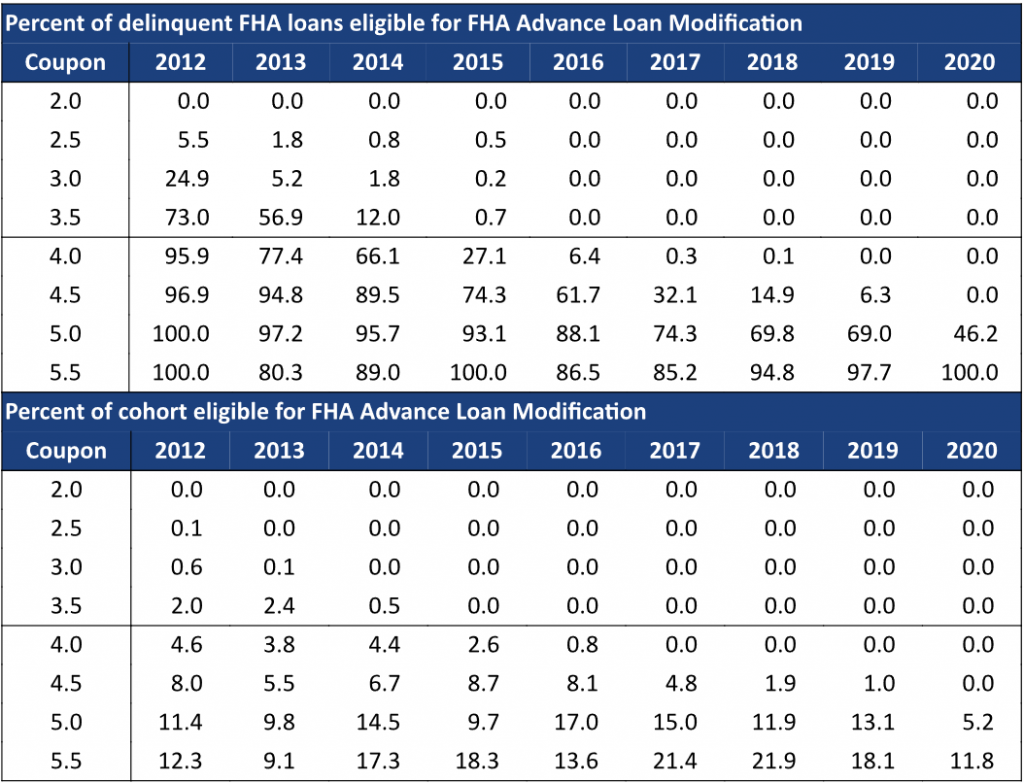

Another way to measure how many loans are on the bubble is to use a more lenient P&I requirement (Exhibit 3). This table shows the percent of delinquent borrowers that would qualify for an ALM if it required a 20% P&I reduction instead of a 25% P&I reduction. This exhibit assumes a 3% mortgage rate. The number of loans that are eligible increases sharply. For example, the 2018 and 2019 vintage 5%s jump to almost 70% eligibility and over 10% of those cohorts would be likely to prepay because of the ALM. Small changes in in mortgage rates, or if borrowers use less than the maximum amount of forbearance, could push many borrowers into an ALM.

Exhibit 3. Many borrowers are close to the P&I threshold

FHA loans as of 6/1/2021 that would qualify for an Advance Loan Modification assuming maximum use of forbearance, a 3.0% mortgage rate, and requiring the new P&I payment to be less than or equal to 80% of the contractual P&I payment. Ginnie Mae loan-level data was used to estimate the amount of past-due principal, interest, taxes, and insurance. Taxes and insurance accrue at 12 bp each month.

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities

The ALM program should keep buyouts elevated longer. Some servicers have been more aggressive at buying out delinquent loans than others, and they are running out of supply of delinquent loans. Absent any other changes, this would have led to buyout burnout. Other servicers have not been exercising their buyout option and might have allowed loans to cure without a buyout. The ALM should force a buyout of some of those loans, increasing speeds of servicers that have been slow to buyout.

ALM details

The FHA has designed the Advance Loan Modification to be easy for servicers to administer. All borrowers that are at least 90 days delinquent and on a Covid-19 forbearance plan must be reviewed for an ALM within 30 days of the expiration of forbearance. The servicer must send the loan modification documents to all borrowers that are eligible, and the servicer does not need to contact the borrower before sending the documents. Borrowers that do not qualify or decline the offer must be evaluated for other loss mitigation options. However, most borrowers that receive this offer are likely to accept it.

The FHA has asked servicers to review for ALM all borrowers that, as of June 25, are at least 90 days delinquent and have not yet received another loss mitigation offer. This includes all borrowers that have exited or requested to exit Covid-19 forbearance, all borrowers whose Covid-19 forbearance will expire by August 24, and all borrowers that are not on Covid-19 forbearance. Servicers may begin to use the ALM immediately and must implement it by August 24.

The modification rolls delinquent interest, taxes, and insurance into the principal balance of the new loan. The interest rate on the new loan is modified to match Freddie Mac’s Primary Mortgage Market Survey rate rounded to the nearest one-eight percent. The loan is re-amortized over 360 months. The borrower is eligible for the modification and must be sent the modification offer if the new principal and interest payment is at least 25% lower than the contractual principal and interest payment.

The FHA also extended the maximum length some borrowers can remain in Covid-19 forbearance. Borrowers that entered forbearance between July 1, 2020 and September 30, 2020 can now request a single 3-month extension, for a total of 15 months. Borrowers are now allowed to enter forbearance between July 1, 2021 and September 30, 2021 but can only use a maximum of six months.