The Big Idea

Lessons learned from another quarter of returns

Steven Abrahams | July 9, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

Market expectations about net liquidity, not inflation, set the direction for rates in the second quarter. And core demand from outside rather than inside the banking system set the direction for spreads. Those lessons should hold for the next few quarters, or at least until the market gets a clear view of the Fed’s path out of QE. Those lessons also have clear implications for positioning: underweight rates and MBS, overweight corporate and structured credit.

The environment

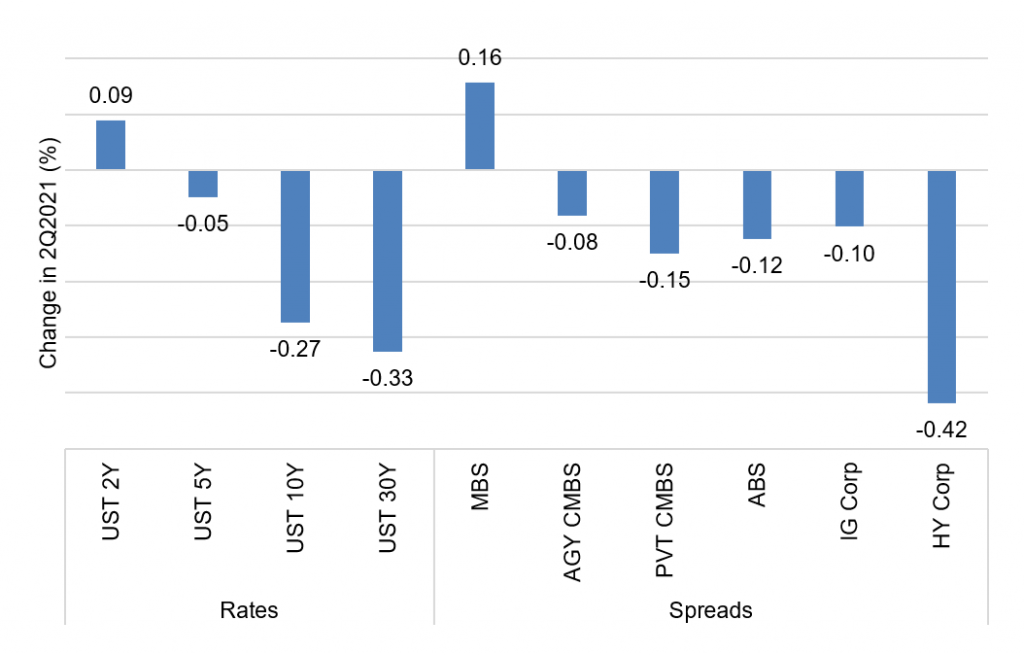

The second quarter showed that market expectations about net liquidity, not inflation, are setting the direction in rates. Breakeven 10-year inflation, for instance, started the quarter around 237 bp and ended the quarter only three basis points lower. But 10-year real rates—the market’s view of where the supply and demand for money will clear for the next decade—dropped from negative 63 bp to negative 87 bp. To slightly oversimplify, the market expects to see lots of money sitting around and not enough growth to soak it up, so the real rate fell. The net result was generally lower nominal rates, although the shortest rates tipped up (Exhibit 1).

Exhibit 1: Changes in rates and spreads through 2Q2021

Source: Bloomberg, Amherst Pierpont Securities

The second quarter also showed that assets with core demand from outside the banking system look likely to deliver much better spread performance than assets that rely on demand from inside the system. In structured and corporate credit where mutual funds, international investors and insurers form core demand, spreads tightened. In agency MBS, where the Fed and banks were the only net buyers from March 2020 through March 2021, the rising chatter about tapering pushed spreads wider over the quarter.

The lessons from rates hold. With peak realized inflation likely behind us and breakeven inflation likely grounded in its current range, the next move in rates should depend on Fed tapering. The Fed is likely to taper faster than it did through 2014, ultimately slowing the flood of cash and falling short of current market expectations for liquidity. Real rates should consequently rise. Nominal rates should rise, too.

The lessons from spreads hold, as well. Softer demand for MBS from the Fed and banks looks set to come just as net MBS supply picks up. Net supply ran below $40 billion a month through most of 2018 and 2019, and above $80 billion a month in the second half of 2020. A strong housing market and rising home prices should keep net MBS supply elevated. Lower demand and higher supply do not bode well for MBS spreads. Corporate and structured credit spreads should do better than MBS. Core demand from mutual funds, international investors and insurers should continue as the economy grows, and the heavy net supply of corporate debt from last year is abating.

Asset returns

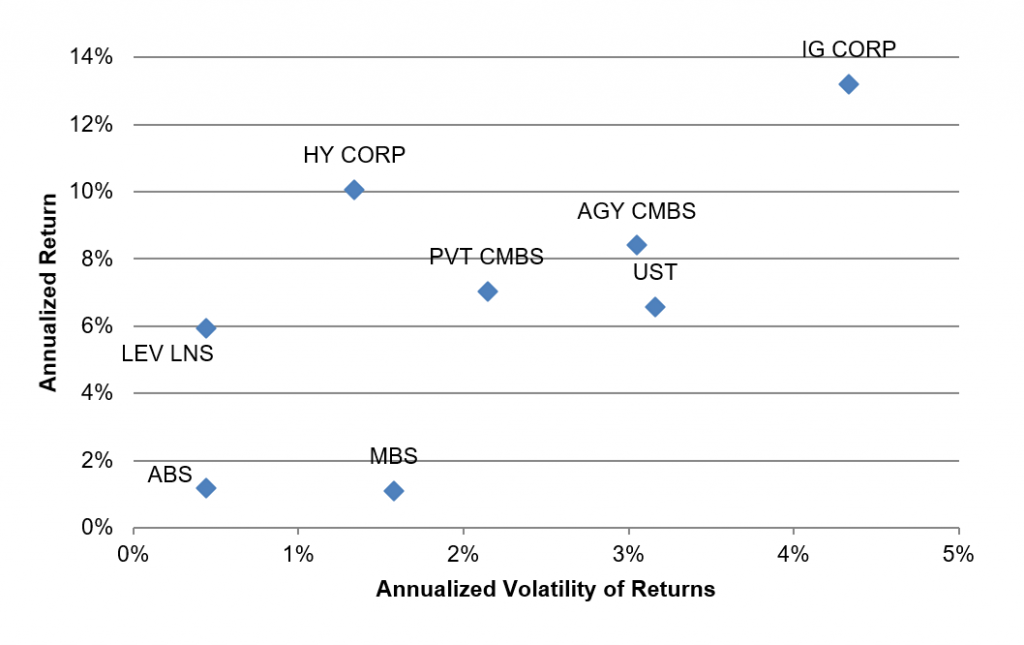

The lesson from asset returns in the second quarter highlighted the importance of different exposures to rates, carry and spreads, especially when it comes to volatility of returns. Investment grade and high yield corporate debt finished with the highest absolute returns, although high yield generated its returns with only a quarter of the volatility (Exhibit 2). Returns on leveraged loans trailed high yield, but loans still generated the highest returns after adjusting for volatility. The most efficient returns for risk taken came from credit. Treasury debt and CMBS finished with moderate results, with MBS and ABS trailing. For portfolios at liberty to shift asset allocations, the right combination of exposures to corporate credit would have outperformed any mix of other assets—either netting higher return with the same risk or equal return with less risk.

Exhibit 2: Annualized asset returns and volatility in 2Q2021

Source: Bloomberg, Amherst Pierpont Securities

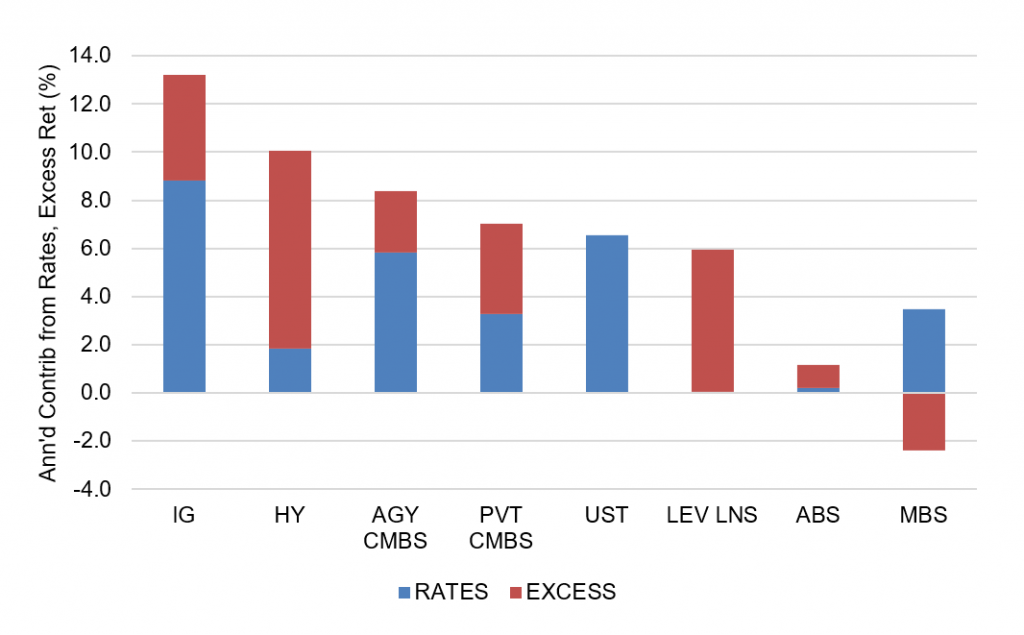

The differences in returns and volatility of returns reflected the different risk exposures. Investment grade credit returns came largely from rates, while high yield returns came largely from carry and spreads (Exhibit 3). Leveraged loan coupons float with LIBOR, so all the return came from carry and spreads. The differences in exposure tie back to differences in return volatility. Carry typically is the most stable component of fixed income return, spread the next most stable and rates the least. That is obviously not always the case, but it is a reasonable expectation. That lines up with the relative efficiency of asset returns in the second quarter.

Exhibit 3: Contributions from rates and from excess return in 2Q21

Source: Bloomberg, Amherst Pierpont Securities

Positioning for the next quarter and beyond

Since March 2020, investors have done well by generally underweighting rates and MBS and overweighting corporate and structured credit. Chalk that up to a market that quickly priced in the Fed impact and bank impact on rates and MBS and left little excess return for other investors. Corporate and structured credit has had much more opportunity. Those broad circumstances still hold, although the market is likely underestimating the pace of Fed tapering.

For portfolios with the flexibility, exposures in rates and MBS should be enough to cover stress case needs for liquidity but return prospects in those sectors do not argue for much more. At some point, real rates should rise high enough (0.50% for 10-year real rates) and nominal rates high enough (2.50% for 10-year nominal rates) to argue for solid long positions. At some point, par 30-year MBS spreads should widen enough (+90 bp to the 7.5-year Treasury curve) to argue for a solid long position.

For now, stay overweight in corporate and structured credit mainly for carry. Sectors Amherst Pierpont particularly likes in investment grade credit:

- In non-financial credits: Communications, energy and technology

- In financial credits: REITs, insurance, finance companies

In structured credit, a few areas stand out:

- Fannie Mae and Freddie Mac credit risk transfers, which have broadly lagged similar corporate credit and offer exposure to consumer balance sheets, which are running at historically strong levels

- Investment grade CLOs, which have lagged CMBS and other similarly rated structured credits and have improving fundamentals behind the underlying loan collateral

Through the third quarter, the market should hear from the FOMC in late July, from Chair Powell in Jackson Hole in August, and again from the FOMC in late September. That should reprice the market as the Fed gets closer to tapering. Underweight rates and MBS and overweight credit should do well.

* * *

The view in rates

On the short end of the rates curve, excess liquidity still shapes the market. Fed RRP balances closed Friday at more than $780 billion. Settings on 3-month LIBOR closed the week at 11.9 bp, tied with the lowest setting ever. The front end is still awash in cash, but the Fed RRP rate of 0.05% has put a floor on money market rates. Fed tapering should keep adding cash to the front end into the second half of 2022, so money market rates look likely to remain low into 2022, as well.

The 10-year note has finished the most recent session at 1.36%. Breakeven 10-year inflation is at 230 bp, with 10-year real rates at negative 94 bp. Expected inflation has remained relatively stable in recent weeks with real rates continuing to drop. The market still sees supply of cash outstripping demand for years. Fed taper should push up real and nominal rates.

The Treasury yield curve has finished its most recent session with 2s10s at 115 bp, 11 bp flatter than two weeks ago. The 5s30s curve has finished at 120 bp, only 3 bp flatter than two weeks ago.

The view in spreads

The timing and pace of tapering and the timing of Fed hikes are the big issues for MBS. Heavy net supply is an issue, too. The market has arguably priced additional risk of soft demand and steady supply. Spreads have widened from their late-May lows. But MBS spreads look vulnerable to going still wider as the Fed likely leans into tapering or tapering-and-hiking faster than the last time.

In credit, low rates should continue supporting corporate balance sheet strength. Ratios of EBITDA to interest expense are in the middle of the range despite high ratios of debt to EBITDA. Investor demand for yield should keep spreads relatively tight. A strong economy should help credit spreads, but relative value flows at money managers could still soften credit spreads if MBS gets wide enough.

The view in credit

Consumers are strong and most corporations in good shape. Fundamental credit should hinge on whether the Fed can orchestrate a soft landing as it starts to tighten financial conditions. Consumers finished the first quarter of 2021 with net worth up $5 trillion. Aggregate savings jumped again as did home values and investment portfolios. Consumers have not added much debt. Corporate balance sheets have taken on more leverage, although mitigated by strong cash balances and low interest costs. EBITDA-to-interest-expense is at healthy levels. Strong economic growth in 2021 and 2022 should lift most EBITDA and continue easing credit concerns. Eventually, rising interest expense in 2023 should compete with EBITDA growth.