The Long and Short

Sustainability-linked bonds, a new corporate trend?

This material is a Marketing Communication and does not constitute Independent Investment Research.

The new issue corporate bond market produced three sustainability-linked bonds in recent sessions that pay investors with a coupon step-up if the issuer misses certain environmental, social or governance targets. This could become a new trend, and investors may welcome it. SLB bonds hold management teams accountable for hitting a range of goals from emissions standards to improving employee diversity while getting investors more comfortable with credits that face environmental or social issues. With fixed income investors largely financing capital projects, the accountability seems long overdue. Additionally, SLB issuance could benefit sectors that have difficulty issuing Green bonds, such as energy and mining.

SLB or Green Bond– What’s the Difference?

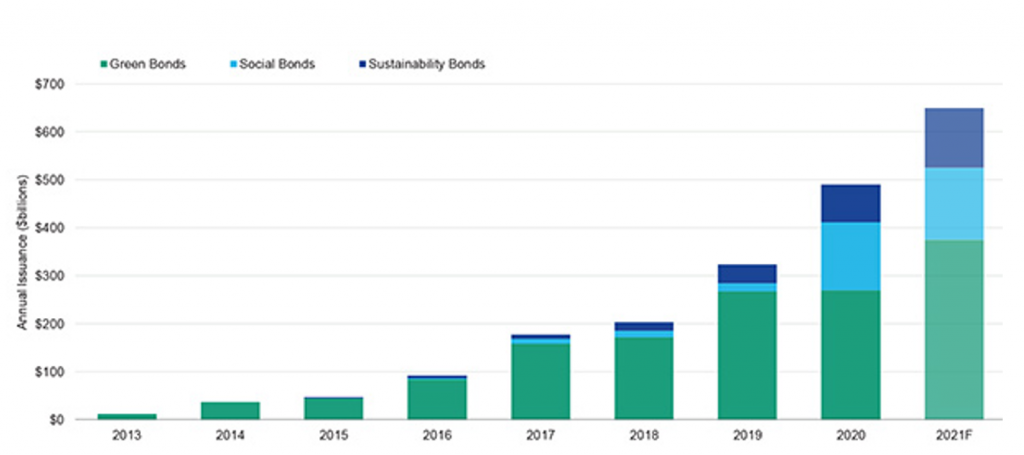

The market has seen a plethora ESG bonds issued over the past year, as demand for these types of issues have increased dramatically given the rise in global awareness of ESG factors. In 2020, we note that approximately $491bn of ESG bonds were issued with Green bonds accounting for over half of ESG issuance. SLB bonds are still relatively new to the market and only accounted for roughly 15% of ESG issuance. In a Green Bond, the proceeds are used to finance a defined ESG project, such as renewable energy or climate change adaptations. However, in an SLB bond, proceeds can be used for general corporate purposes, but the coupon will step at a certain time if key performance indicator thresholds are not achieved. Moody’s forecasts that ESG issuance will hit a new record of $650bn this year with SLB bonds accounting for nearly 20% of the issuance. This translates to SLB issuance growth of 58% from 2020. While global debt volumes are expected to pull back from the record year that the pandemic produced, SLB bonds are likely to continue to increase their share of total global issuance, which we believe will be driven by investor demand and familiarity with the structure.

Exhibit 1. ESG Issuance 2013-2021E

Source: Moody’s Investor Service Inc.

Telus- First Canadian Issuer to Price SLB Bond

Telus (TCN) kicked off the week as the first Canadian issuer to price an SLB bond as part of the company’s SLB framework which was announced earlier this month. TCN has committed to reducing its absolute Scope 1 and Scope 2 greenhouse gas emissions by 46% from 2019 levels. Should TCN fall short of its target by 12/31/30, the bonds will step up 100bps per year. We note that TCN issued C$750mm of the notes and they mature on 11/31/31, so any failure to hit its emission target will only result in one step up. According to TCN, the SLB Framework was approved by the Science Based Targets initiative and is consistent with reductions required to limit global warming to 1.5 degrees Celsius. TCN plans to report annually on its performance in achieving its Sustainability targets, and also plans to obtain independent verification in the form of a limited assurance report on an annual basis. The deal was 3.5x oversubscribed and priced at the tight end of IPT (+137bps).

Enbridge Sees Strong Demand for Inaugural SLB Issuance

Enbridge (ENBCN) priced an inaugural 12yr SLB bond this week, the first in the pipeline sector, that captured investor attention as the order book for the deal was 4x oversubscribed. The new issue differs from TCN’s deal as it has two performance metrics, one related to carbon emissions and the other related to diversity amongst ENBCN’s workforce. Under the first performance metric, the coupon will step up +50bps if ENBCN does not reduce Scope 1 and Scope 2 Emissions intensity by 35% by 12/31/30. Under the second performance metric, the coupon will step up +5bps on 12/31/25 if ethnic or racial minorities account for less than 28% of ENBCN’s workforce. We believe the difference in the coupon steps and targeted deadlines between the performance metrics relates largely to the level of difficulty related to each. ENBCN was able to price the SLB bond 15bps-20bps through IPT (at +105bps) given the demand. We expect the deal to perform well post pricing with demand likely to increase as more investors get familiar with the structure. Post launch, bonds were +3bps tighter.

Mississippi Power Issues 30yr Sustainable Green Bond

Mississippi Power (SO) was also in the market with a sustainable bond, however, we note that the issuance actually looks like a Green bond. The $325mm in proceeds issued are expected to be used to finance/refinance one or more eligible ESG projects. Pending allocation for an ESG project, the company will use the proceeds to redeem $270mm of a Taxable Revenue Bond that matures 10/21/21 and is issued out of Mississippi Business Finance Corp. Since there is no coupon step language associated with key performance metrics, we believe this issuance should be classified as Green bond.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.