The Long and Short

Up in quality with surplus notes

Dan Bruzzo, CFA | June 18, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Insurance company surplus notes let investors move up in ratings while still adding spread over lower-rated notes issued at the senior unsecured level. Following the June Fed meeting, the spread on the Bloomberg Barclays IG corporate bond index closed at 81, the tightest aggregate OAS since March of 2005. Meanwhile, ‘BBB’ credit closed at an OAS of 100, a threshold that has not been reached since even earlier in the decade. With spreads testing these historic levels, and limited compensation for additional risk, up-in-quality makes sense.

While the higher coupon / dollar-price accounts for a portion of the relative valuation of the older, legacy surplus notes, the AA-rated bonds still offer attractive spread to often lower-rated (single-A), senior global notes issued by the large public life insurers (MET, PRU, AFL, etc.). Furthermore, in the low-rate environment, the prospect for potential tender offers on some of the older, higher coupon issues, presents additional opportunity holders. Surplus notes have maintained a large aggregate pick to their senior, publicly issued counterparts. And while that spread has compressed over the past several years with increased risk appetite and price discovery in this segment, these structures provide a means for conservative investors to gain exposure to higher-rated credits in the long-end of the curve, without conceding much spread.

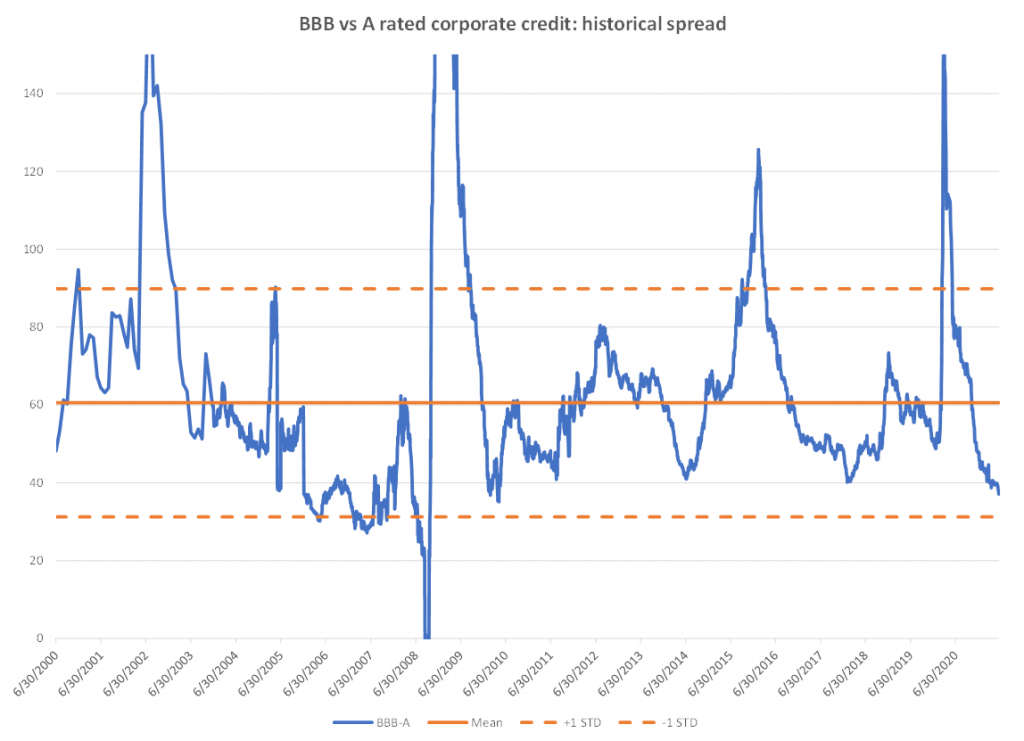

Exhibit 1.

Source: Amherst Pierpont, Bloomberg/Barclays US Corp Index

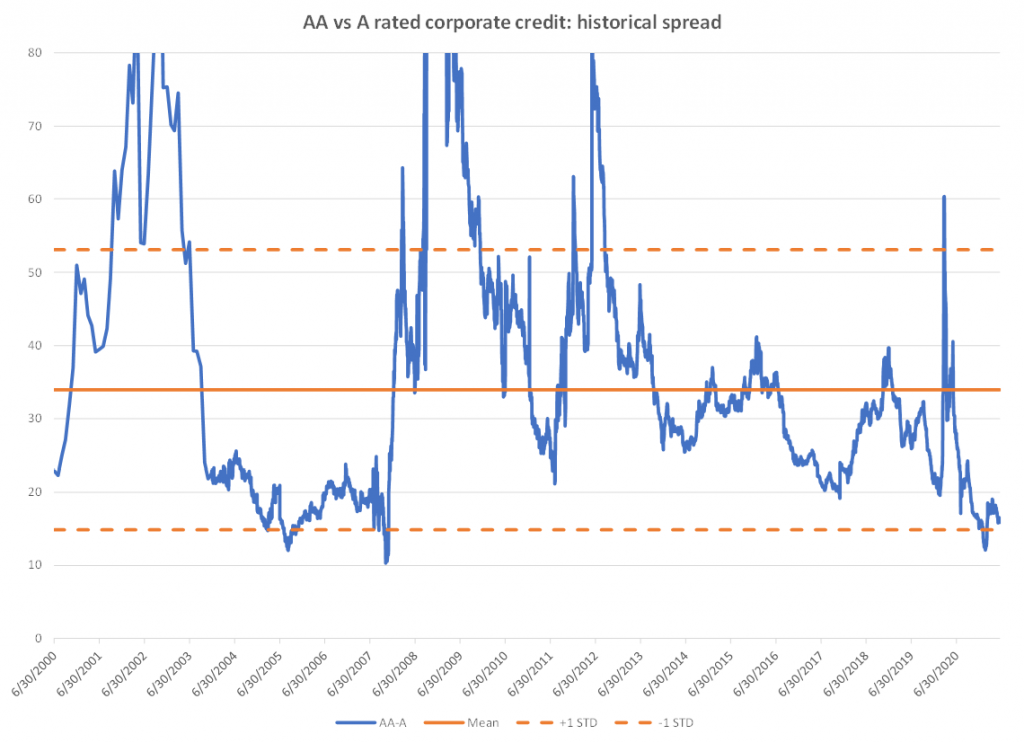

Exhibit 2.

Source: Amherst Pierpont, Bloomberg/Barclays US Corp Index

Insurance surplus notes are somewhat of a niche structure within the broader investment grade insurance universe, but the segment trades with enough regularity that investors can remain active and target the additional spread opportunities available. Once a temporary funding strategy predominantly utilized by mutual companies in the ’90s, these subordinated structures resurfaced over the past decade and have seen enough new issue in the last few years to remain a relevant option for both mutual and public insurance companies seeking to create diversified funding within their capital structures.

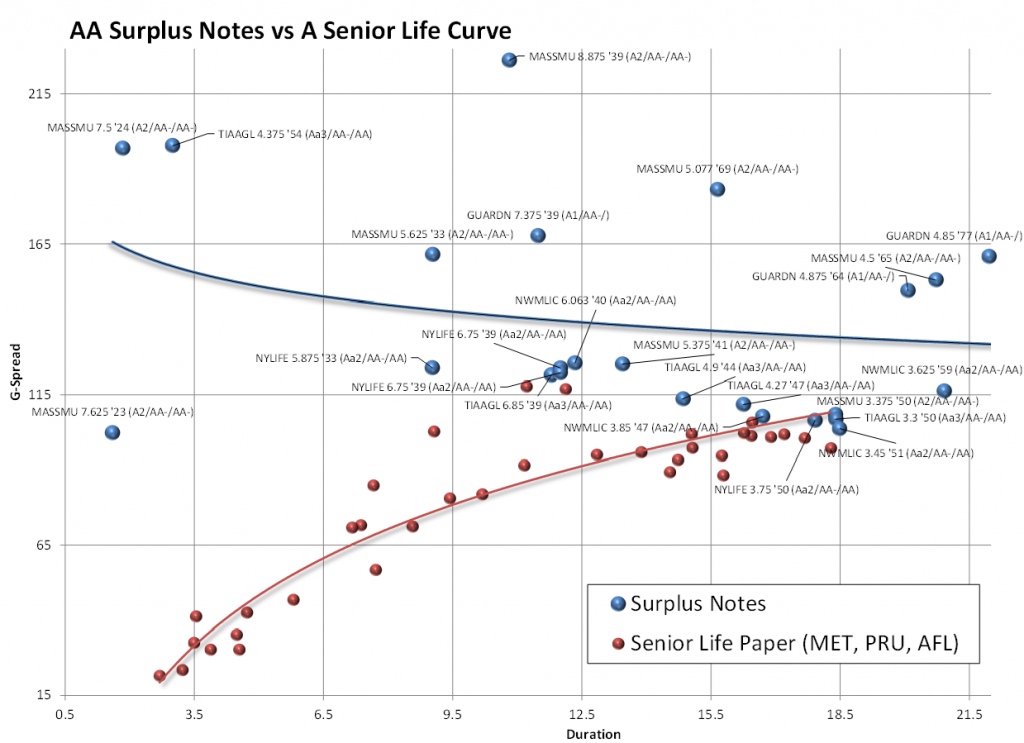

Exhibit 3. AA-rated surplus notes vs lower-rated senior unsecured life insurance paper

Source: Amherst Pierpont, Bloomberg/TRACE – G-Spread indications only

Background on surplus notes

Public and mutual insurance companies utilize surplus notes offerings to diversify capital and attract different types of investors within the public debt markets. Despite their subordinated classifications within the capital structure, in many cases surplus notes are among the only outstanding debt issues for mutual companies. Therefore, they are often only subordinated to insurance company’s policyholders from a priority of payment standpoint. Interestingly for the public insurance companies, since the debt is issued directly out of the insurance operating company, it typically maintains structural seniority to most of the senior unsecured debt issued at the parent company level, though remain subordinated to funding agreement-backed (FA-backed) or guaranteed investment contract (GIC) structures at the operating company. Furthermore, since large mutual insurance companies are conservatively managed, and typically well-capitalized, these subordinated issues frequently maintain higher ratings than even the senior debt levels of some of the largest and higher-rated public insurance companies.

Surplus notes are technically hybrid capital – but with limitations

Surplus notes are subordinated to policyholders and all other senior debt instruments outstanding at the operating subsidiary. They are classified as hybrid capital since they technically provide for temporary loss absorption to issuers. While the deals are mostly issued as cumulative, both principal and interest payments must be approved by the insurance company’s state regulators. At the regulator’s discretion, those payments can be delayed without triggering an event of default or cross-default provisions. In the event of a delay in interest payment, interest accrues until regulatory approval is reinstated to the issuer to resume the payments. Since the structures first became prominent roughly 30 years ago, there are very few instances where a delay in payment was implemented among IG issuers.

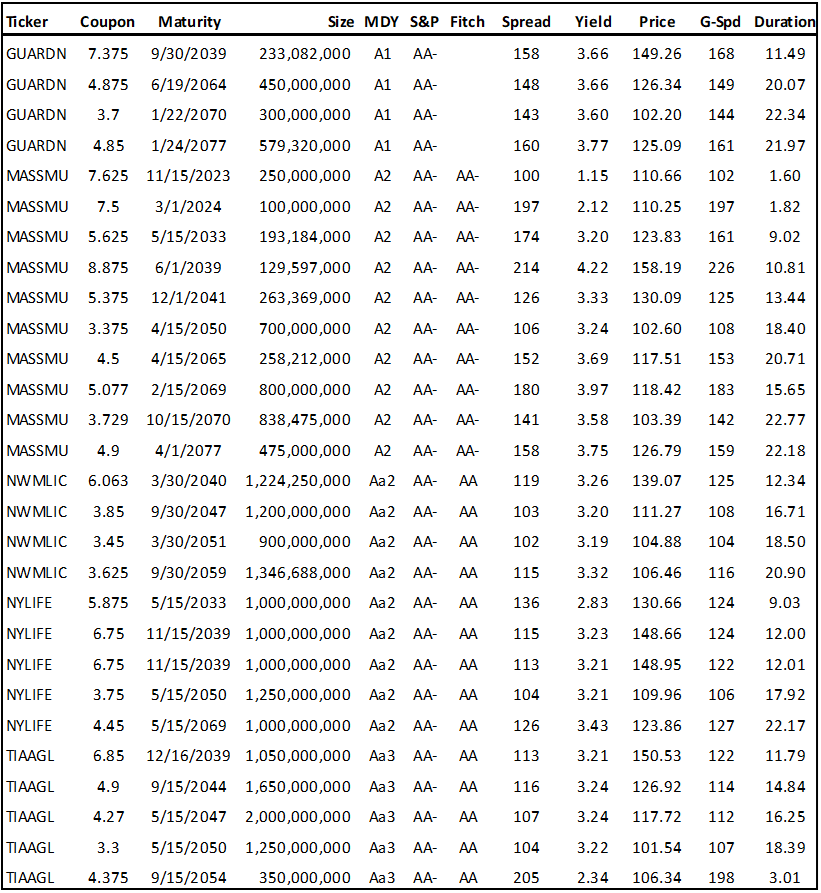

Exhibit 4. AA-rated surplus note universe

Source: Amherst Pierpont, Bloomberg/TRACE – G-Spread indications only

Why surplus notes were originally conceived

Mutual insurance companies are mostly owned by the policyholders themselves. As a result, access to public capital markets was traditionally more limited. This new structure gave non-traditional issuers the opportunity to bolster capital levels and enhance financial flexibility. As with principal and interest payments, the actual issuance must also be approved by the state regulator. The structure was largely dormant for some time but re-emerged after the financial crisis in 2009 as insurance companies looked to bolster capital ratio levels and instill confidence in the markets. Issuance has since been sporadic, with several prominent deals coming over the past few years.

Rating agencies’ approach to surplus notes

Moody’s typically rates surplus notes two notches lower than the operating company’s insurance financial strength (IFS) rating for life insurers, and three notches for property & casualty insurers. S&P also rates two and three notches below the operating company financial strength rating as well. For hybrid treatment, the rating agencies will determine the level of equity credit to the issuer based on the maturity and whether or not the issue is cumulative. However, once the issue is within 20 years to maturity—which is true for many of the original structures from the 90s—Moody’s will automatically treat the issue as 100% debt.