By the Numbers

Assessing M&A risk in ‘BBB’ packaged foods

Meredith Contente | June 18, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

After Campbell Soup posted weak fiscal third quarter results, it looks like the right time to check out potential M&A across the ‘BBB’ packaged food space. Pandemic pantry stocking seems to be behind us, and the market has returned to some new version of normal. Names that need M&A to drive growth will likely boost leverage and soften their debt spreads while names set to reduce leverage should hold on spread or tighten. Investors should go underweight M&A mavens CPB and MDLZ, and go overweight the doyennes of deleveraging K, KHC and MCK.

It is no secret that the pandemic played a major role in expediting delevering across the ‘BBB’ packaged food space. Most credits had bloated balance sheets after acquisition sprees from 2018 through 2019. The double-digit sales growth triggered by stay-at-home orders helped to fuel stronger-than-expected free cash flow growth, enabling most credits to hit leverage targets roughly a year ahead of original expectations. But CPB’s results highlight that organic growth looks likely to normalize quickly now that the country has largely lifted Covid restrictions. The packaged food space at best in normal times tends to produce organic growth rates of approximately 1%. However, prior to the pandemic, organic sales were largely in the -1% to flat range, hence the acquisition binge designed to help spur growth.

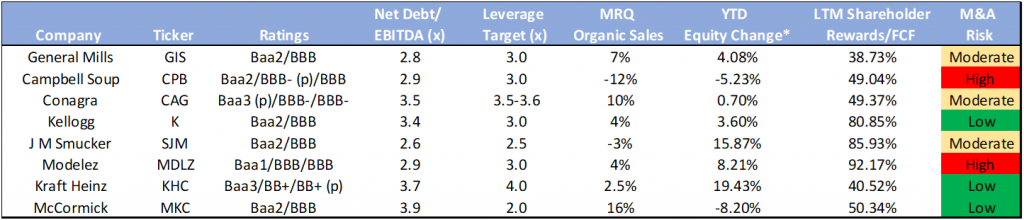

Exhibit 1. BBB Packaged Food Comparison

*as of 6/17/21

Source: Bloomberg; Company Reports; Amherst Pierpont Securities

High risk for M&A

Campbell Soup Company

Based on the metrics in Exhibit 1, we believe CPB will be most at risk for pursuing an M&A transaction as the company is currently below their leverage target and both organic sales and equity performance is now in negative territory. We note that for the nine months ended 5/2/21, organic sales growth for the company was 1% but is expected to decline further for the full year with guidance calling for organic net sales to be in the -1.2% to -0.7% range. While CPB has yet to resume share repurchases, its dividend currently consumes nearly half of its free cash flow generation. An M&A transaction could potentially address both its sales growth and equity performance. Furthermore, we note that while CPB’s EBIT margin of 14.3% was down nearly 300bps from the year ago period, it also contracted roughly 80bps from fiscal 3Q19. Again, an M&A transaction is likely to produce cost synergies which could help to address margin decline.

Mondelez International

While MDLZ does not necessarily fit all of the parameters to pursue an acquisition given than its still producing decent organic sales growth and its equity continues to remain in positive territory, we note that MDLZ management has been very active with pursuing acquisitions as they have announced/completed 4 acquisitions since 2Q20. Management’s acquisition strategy has been to add in high growth markets to drive an accelerated growth rate. While these acquisitions have been of “tuck-in” size, primarily in the snacking space, management noted on its last earnings call that it is looking to execute on further acquisitions in the snacking space, both small and large, if it will accelerate its overall growth rate. That said, we would expect MDLZ to not hesitate to pursue a larger, leveraging transaction as long as it fits its growth parameters. With its leverage below its target rate currently, MDLZ has some flexibility to pursue a more transformational transaction.

Moderate risk for M&A

General Mills

GIS is now roughly 2 ticks below their leverage target and while organic sales growth has been strong, up 7% in the MRQ and 8% for the nine months ended 2/28/21, GIS is expecting its fiscal 4Q to be much weaker due to difficult yoy comparisons and less pantry stocking. As such, for the full fiscal year, GIS has guided to a 3.5% organic sales growth rate. That would indicate that management is expecting organic sales to fall approximately 10% in fiscal 4Q. While there was no mention of M&A activity on the most recent earnings call, management suggested in the prior quarter that they now have flexibility to pursue M&A as they have proven it the past, with Blue Buffalo acquisition, that it provides a great way to add value. Additionally, they noted that it was not necessary to wait for the pandemic to end to pursue acquisitions given that they had achieved their leverage target already. If no M&A opportunities present themselves, we would expect most excess free cash flow to be directed to share repurchases.

Conagra Brands

CAG’s most recent results exceeded guidance as the company posted organic sales of 9.7%, which was 170bps above the high end of management’s target range. CAG chalked up its outperformance to innovation, particularly in the frozen food space. While fiscal 4Q organic sales are expected to be down in the 10%-12% range due to tough comparisons (organic sales were up 21.5% in fiscal 4Q20), it still translates to full year organic growth in the 5.2%-5.7% range. Additionally, CAG management has provided guidance for fiscal 2022 with organic sales growth in the 1%-2% range. If management can produce organic growth of 1% or higher, there is likely less need to pursue acquisitions and focus more on re-investing in the business via innovation as they have demonstrated good success in the past. CAG management noted on the last earnings call that with the balance sheet at the lower end of their leverage target range, they have increased investments in the business via capex. Management once again reaffirmed its commitment to strong investment grade ratings and maintaining a balanced capital allocation policy.

JM Smucker

SJM is hovering close to its leverage target but noted that it will continue to look to repay debt to return its leverage to its 2.5x target. SJM’s number one priority for free cash flow is to reinvest in the business through capital expenditures in an effort to support growth brands (i.e., Uncrustables). Acquisitions remain at the tail end of priorities but ahead of share repurchases. Management will continue to focus on maintaining a balanced capital allocation policy. For fiscal 2022, SJM is guiding to organic sales growth in the 2% range as they expect to take pricing actions across multiple categories to recover increased commodity and input costs.

Low risk for M&A

Kellogg Company

K’s leverage remains above the company’s target of 3.0x so we expect the company to continue to prioritize debt reduction. We note that K ended the most recent quarter with net debt of $7.3bn which was only down $100 million from the year ago-period. While net leverage has improved from the company’s average of 3.6x, K will need to continue to be proactive in paying down debt to achieve its leverage target. We note that K’s organic growth rate continues to remain solid and management recently revised full year guidance up from previous expectations of down 1% to flat for the year. The revised guidance equates to roughly 3% organic growth on a 2-year CAGR. Additionally, free cash flow guidance was also revised upwards by $100 million, which supports both increased shareholder rewards and further debt reduction.

The Kraft Heinz Company

While KHC is now currently below its leverage target, management continues to remain focused on completing the sale of its natural cheese business (expected to close by 6/30/21) and using divestiture proceeds to further repay debt. We note that KHC recently closed on the sale of its Planter’s business (6/7/21) and subsequently announced a tender offer for up to $2.8bn of debt. While KHC only successfully received just over $1.4bn in the tender, we expect management to continue to look for ways to further reduce debt by either executing on make whole calls or paying down debt as it matures. KHC has roughly $1bn of debt maturing in both 2022 and 2023 and management has explicitly stated that it wants to focus on the natural cadence of leverage reduction. Any acquisitions are likely to be very small in nature and focused on being complementary to existing business lines. Management is focused on returning to full IG status, which will require net leverage to stay below the 4.0x threshold.

McCormick & Company

MKC is still in the process of delevering from its Cholula and FONA acquisitions which pushed leverage close to 4.0x. We expect MKC to look to get closer to its leverage target of 2.0x prior to embarking on any type of leveraging transactions. We believe MKC will look to repay the $1.0bn of debt maturing through 2022 versus refinancing to help bring leverage more in line with its current mid BBB ratings, as leverage currently exceeds the thresholds for the current ratings. Furthermore, management has stated its commitment to maintain its current IG ratings and will curtail share repurchases until its net leverage target has been achieved. Its most recent debt issuance was used to help refinance its commercial paper balance, helping to push out its weighted-average debt maturity.