The Big Idea

A JOLTS of reality in the labor market

Stephen Stanley | June 18, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

A series of supply bottlenecks in key industries has produced shortages and price spikes unlike anything seen arguably since the 1970s. And that includes labor, too. After roughly 25 million jobs disappeared last year when much of the economy shut down, normalization has been rocky. With the pandemic quickly fading this year, the demand for workers has rebounded faster than the willingness of people to return to jobs. The April JOLTS data helped crystallize that fact and may have played a role in how Chair Powell described the labor market at the latest FOMC.

Supply and demand in the labor market

Economists, and especially Fed economists, tend to operate mostly on the demand side. The supply side is generally taken as given, and the strength or weakness of the economy is seen as dictated by whether demand is robust or soft. This is especially so for the labor market. For decades, financial market participants have been trained to view the ups and down in the labor market as a function of the demand of firms for workers.

This framework prevails in ways that may not even be obvious at first. For example, the implications are clear in most cases when unemployment rises significantly: workers are being laid off and are not easily finding new jobs. But what about when labor force participation drops? People can decide to quit work or stop looking for a job for any number of reasons. However, economists generally assume that when labor force participation falls, it means that potential workers who were previously actively looking for a job have given up their search efforts because they were not finding viable prospects. In other words, it is a sign of weak labor demand.

Fed narrative for a labor market recovery

It is worth noting the broader context of Fed thinking on the labor market. The labor market had gotten to an unusually tight position in in 2018 and 2019, with the unemployment rate falling to 50-year lows, well below 4%. Even so, wage gains and consumer price inflation remained quite modest, defying the Fed’s Phillips Curve modelling. Fed officials were so impressed by this performance that they concluded that it reflected permanent structural changes to the economy. They altered their monetary policy framework, declaring that they would in the future let the economy run hot, no matter how low the unemployment rate fell, until inflation actually began to accelerate above the 2% target on a sustained basis.

When the pandemic struck last year, and employment sank abruptly, the consensus view among Fed officials was that it would take years for labor demand to recover to pre-pandemic levels. Moreover, even though the labor market was unusually strong immediately before the pandemic, the FOMC declared that it would need to see a full return to pre-pandemic settings for key labor market variables before it would consider lifting rates off of the zero bound. The FOMC projected up until June that policy would remain on hold at least until 2024.

As recently as the FOMC meeting in late April, Chair Powell described the labor market as follows: “For the economy as a whole, payroll employment is 8.4 million below its pre-pandemic level. The unemployment rate remained elevated at 6 percent in March, and this figure understates the shortfall in employment, particularly as participation in the labor market remains notably below pre-pandemic levels.” In the Q&A session, he was asked directly about widespread reports of labor shortages and he downplayed that, noting that in the prior expansion, despite worries about worker shortages, “labor supply generally showed up.”

In short, the Fed narrative was that any shortfall in the level of employment and of labor force participation reflected demand-side weakness, “slack” in the language of Phillips Curve models. The forward guidance language for asset purchases noted that the Fed needed to see “substantial further progress,” which Powell and others defined as significant movement in the level of employment, labor force participation, from the December 2021 levels toward the February 2020 readings.

Most officials framed the disappointing April and May payroll gains as a sign that demand for workers might not be as robust as previously thought, implicitly suggesting that it could take longer to meet the “substantial further progress” standard.

JOLTing the Narrative

Of course, even as early as April, there was ample evidence that the main impediment to job growth was the reticence of workers to take jobs rather than a lack of demand. This is clearly an unusual situation, which is likely why Fed officials were so slow to believe the survey and anecdotal accounts.

However, the evidence continued to accumulate in May and early June, as surveys of businesses emphasized the inability to staff up—most notably, the ISM and NFIB surveys—and Fed officials were undoubtedly inundated by similar accounts from their array of business contacts.

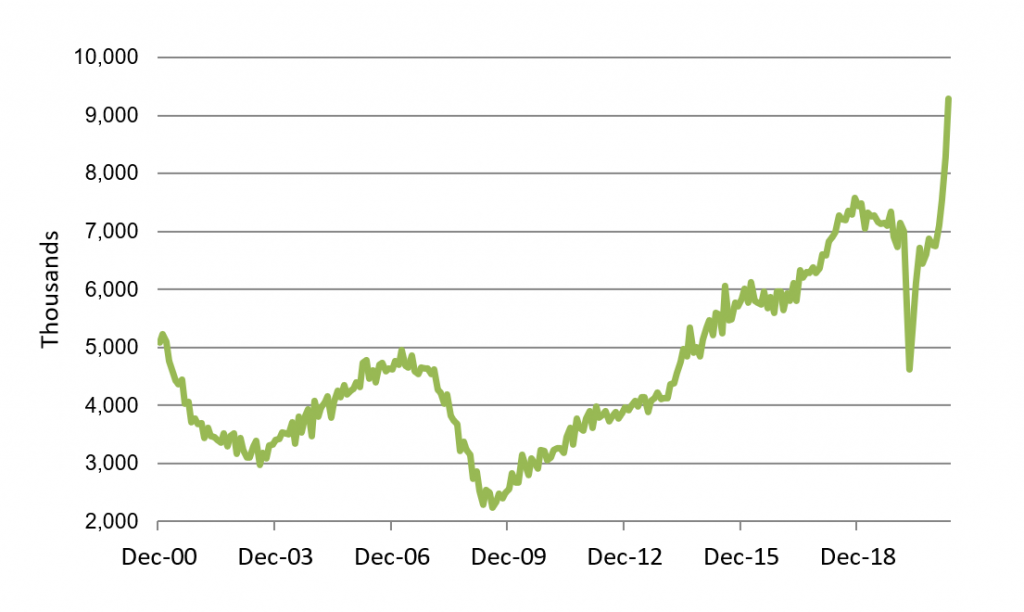

If there was any doubt, the April JOLTS report likely tipped the debate decisively toward a supply-focused explanation. Job openings, which in March had already hit the highest level since 2000, exploded higher by roughly one million, almost 25% higher than the pre-pandemic peak, which was reached at a time when the unemployment rate was well below 4%, as opposed to the current setting close to 6% (Exhibit 1).

Exhibit 1: Job openings

Source: BLS.

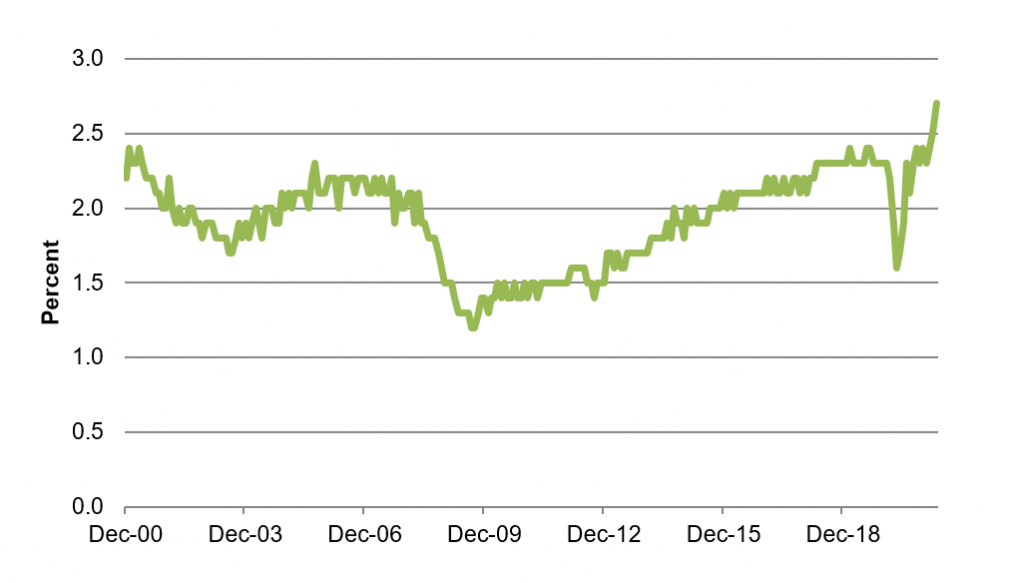

Another measure in the April JOLTS report that underscores the wide and growing supply-demand imbalance in the labor market is the quits rate. This was one of several alternative indicators that then-Chair Yellen used in the mid-2010s to argue that the labor market was softer than the headline unemployment rate suggested. The idea is that when workers are too afraid to quit their jobs—because they are not confident in their ability to find a better opportunity—there is likely hidden slack in the labor market. Like job openings, the quits rate has surged to an all-time high, easily exceeding even the tight labor market 2018-2019 readings (Exhibit 2).

Exhibit 2: JOLTS quit rate

Source: BLS.

These indicators put numbers to a view that I and many other economists have been emphasizing for a few months: the hesitance of workers to take a job is the primary impediment to employment growth right now, not weakness in demand.

Singing a different tune

I think it would be fairly obvious to conclude that the biggest shock and therefore largest driver in the change in the Fed’s tone from the late April FOMC meeting to the June meeting was the surge in inflation in April and May. However, the way that the committee sees the labor market also changed significantly.

In his press conference statement, Powell begins his description of the labor market by reiterating the same thoughts from April: “Employment in this sector [leisure and hospitality] and the economy as a whole remains well below pre-pandemic levels. The unemployment rate remained elevated in May at 5.8 percent, and this figure understates the shortfall in employment, particularly as participation in the labor market has not moved up from the low rates that have prevailed for most of the past year.”

However, from there, he shifted to a discussion of the supply-side impediments. “Factors related to the pandemic, such as caregiving needs, ongoing fears of the virus, and unemployment insurance payments appear to be weighing on employment growth. These factors should wane in coming months against a backdrop of rising vaccinations, leading to more rapid gains in employment.”

When asked about the labor market in the Q&A, he expounded: “In terms of the

near term, you ask as well — so we see a couple of things, a few things that seem likely to be holding back labor supply.” He then discussed the three factors that he had mentioned above. He also indicated that firms may be having trouble quickly finding workers with the right skill set to meet their needs, but I am skeptical of that explanation, since most of the loudest complaints of firms are coming from those who typically hire at the lower end of the pay scale and skill spectrum.

In any case, a number of dovish Fed officials were arguing forcefully during the inter-meeting period that the lower-than-expected payroll gains in April and May would delay the achievement of “substantial further progress.” However, Powell changed the narrative, hinging the labor market outlook on the abatement of the supply side impediments, as health concerns, childcare issues, and the generosity of unemployment benefits should all dissipate over the next few months. As a result, Powell projected “I would expect that we would see strong job creation building up over the summer and going into the fall.”

The decision by the FOMC to acknowledge for the first time that noticeable progress has been made and that it will begin to discuss when that progress will qualify as “substantial” was clearly a result of changes in both the inflation and labor market stories. We will probably never know how important one or the other was in their thinking. Still, while the shocking upside surprises in inflation were probably the biggest contributor, we should not gloss over the significant shift in Chair Powell’s description of the labor market situation, which may have been driven in part by the extreme readings in the April JOLTS report that was released just a week before the June FOMC meeting.