The Big Idea

It’s all about liquidity, not inflation

This material is a Marketing Communication and does not constitute Independent Investment Research.

When the latest CPI printed up 5% from a year ago and core CPI printed up 3.8%, both above surveyed expectations, interest rates did not go up. Inflation expectations rose, at least based on 10-year breakeven rates. But the market’s view of the real cost of money over the next 10 years dropped that day sharply enough to drag 10-year nominal rates down by nearly 6 bp. Inflation surprise, but lower rates. Inflation is getting all the press, but the real story in rates is liquidity.

As my colleague Stephen Stanley illustrated so well earlier this month, the market has priced in an ample cushion for inflation, Potential for surprise is there, but it would have to be major to push the inflation component of rates off its mark. The CPI declined into May last year, so with this year’s May print the market has seen the strongest base effect on year-over-year CPI. The sprint to vaccinate most Americans and reopen the economy has led to a surge in demand that should eventually abate. On the labor front, for instance, more vaccinations, the opening of schools and the lapse of supplemental unemployment benefits should bring a supply of labor back into the work force sometime this fall. Supply should start to respond in other areas as well. The thing to watch is the path of year-over-year inflation, which should start to decelerate as soon as June. If year-over-year inflation does not slow down, that would likely be the surprise that would push rates higher.

Liquidity remains the bigger issue for the crowd routing for higher rates. One way for inflation to overshoot a single month’s expectations and trigger thoughts of liquidity would be for it to fail to overshoot enough to knock the Fed off its likely path. Global central bank QE, Fed preference for a banking system with high levels of excess reserves, foreign exchange reserves, demand for safe assets and even demographics stand to supply excess cash for years. One clear unknown is whether growth can eventually drive enough demand to borrow to soak up the expected cash and push up the real cost of money. With the consensus among economists looking for above-trend growth through 2022 before a glide back to the post-2008 average real GDP growth of 2%, the answer appears to be “no.” The market seems to agree.

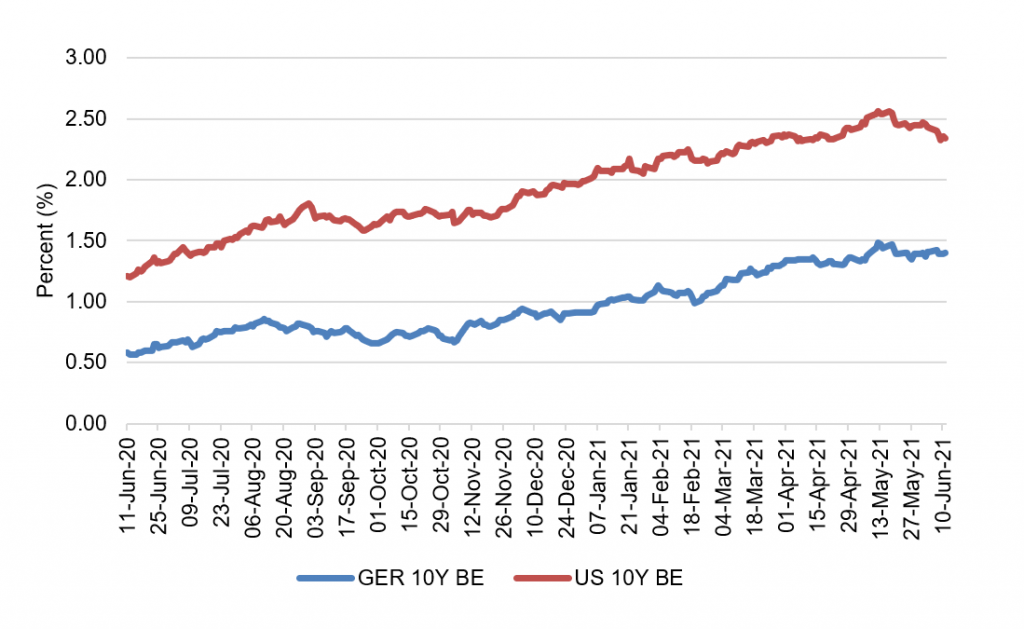

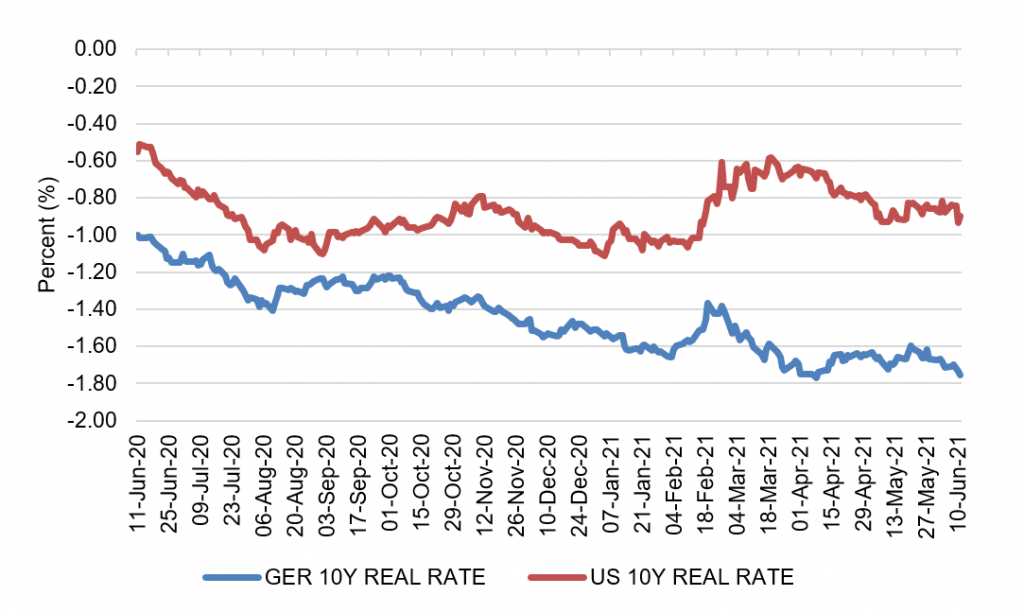

The US is not alone in pricing in rising inflation and a falling real cost of money. German 10-year debt, for example, has more than doubled its implied inflation rate over the last year, and, since September, added inflation expectations in rough parallel with the US (Exhibit 1). German debt also reflects a steadily lower real rate (Exhibit 2). Through February, German 10-year real rates tracked US 10-year real rates but have fallen substantially more since, the recent decoupling arguably reflecting a faster US rebound from Covid with less of a liquidity overhang.

Exhibit 1: Both US and German 10-year debt reflect rising inflation expectations

Source: Bloomberg, Amherst Pierpont Securities

Exhibit 2: Both US and German 10-year debt reflect falling real rates

Source: Bloomberg, Amherst Pierpont Securities

Rates are likely to rise not from steadily pricing in higher inflation but from steadily pricing in a higher real rate. That should start around the same time the Fed starts to take cash out of the system. And that happens not during tapering or its immediate aftermath but when the Fed starts to raise rates and ultimately starts to draw down its QE portfolio and renormalize its balance sheet. Fed funds futures and OIS price in a substantial chance of Fed hikes only starting in 2023, so that should mark the beginning of a slow march to higher real and nominal rates.

* * *

The view in rates

The money markets remain the poster child for excess liquidity. Even though bank liabilities ran roughly flat through May, government money market mutual fund balances rose $119 billion. Overnight Treasury repo and SOFR sit around 1 bp. Recent settings on 3-month LIBOR have dipped to another record at 11.9 bp. Fed reverse repo agreements, offering a 0% rate, stood June 11 at $548 billion.

Concerns about a persistent oversupply of cash also have shaped the longer end of the curve. The 10-year note has finished the most recent session at 1.45%, down 10 bp on the week, despite 10-year breakeven inflation at 2.35%, down 7 bp on the week. The negative 90 bp 10-year real rate implies heavy supply of 10-year cash against limited demand to borrow.

The Treasury yield curve has finished its most recent session with 2s10s at 131 bp, 10 bp flatter from just a week ago. The 5s30s curve has finished at 140 bp, flatter by 5 bp from a week ago.

The view in spreads

MBS spreads have widened notably in recent weeks. The nominal spread between par 30-year MBS and the interpolated 7.5-year Treasury yield closed recently at 70 bp, wider by 8 bp from local tight levels. Refi risk may also be creeping back into MBS. Primary 30-year mortgage rates have dropped below 3.0% in several surveys, and data from the Bureau of Labor Statistics show employment in the mortgage industry up 30% from three years ago, giving originators plenty of capacity to chase loans.

In credit, low rates should continue supporting corporate balance sheet strength. Ratios of EBITDA to interest expense are in the middle of the range despite high ratios of debt to EBITDA. Investor demand for yield should keep spreads relatively tight.

The view in credit

Consumers finished the first quarter of 2021 with net worth up $5 trillion. Aggregate savings jumped again as did home values and investment portfolios. Consumers have not added much debt. Corporate balance sheets have taken on more leverage, although mitigated by strong cash balances and low interest costs. EBITDA-to-interest-expense is at healthy levels. Strong economic growth in 2021 and 2022 should lift most EBITDA and continue easing credit concerns. Eventually, rising interest expense in 2023 should compete with EBITDA growth.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.