By the Numbers

SFR operators come out of Covid stronger

This material is a Marketing Communication and does not constitute Independent Investment Research.

SFR operators have come out of Covid stronger than going in, at least based on first quarter results from the biggest public platforms. Both Invitation Homes and American Homes 4 Rent reported higher occupancy, lower turnover, shorter vacancies between tenants and significant rent growth. These and other large single-borrower SFR sponsors are in better position to support their securitizations. Along with a higher mark-to-market value for portfolio properties, the stronger sponsor financials suggest the credit quality of collateral backing most outstanding SFR securitizations has strengthened, too.

The two largest institutional operators, Invitation Homes and American Homes 4 Rent, combined account for 48% of single-family rentals in the US. Despite some differences in geographic footprint, both companies target very similar market sectors and the recent performance of their portfolios have been remarkably in-line. This may not be the case going forward, as their growth strategies meaningfully diverge, with American Homes 4 Rent diving into built-for-rent while Invitation Homes pursues growth primarily through traditional purchase of existing homes.

Invitation Homes

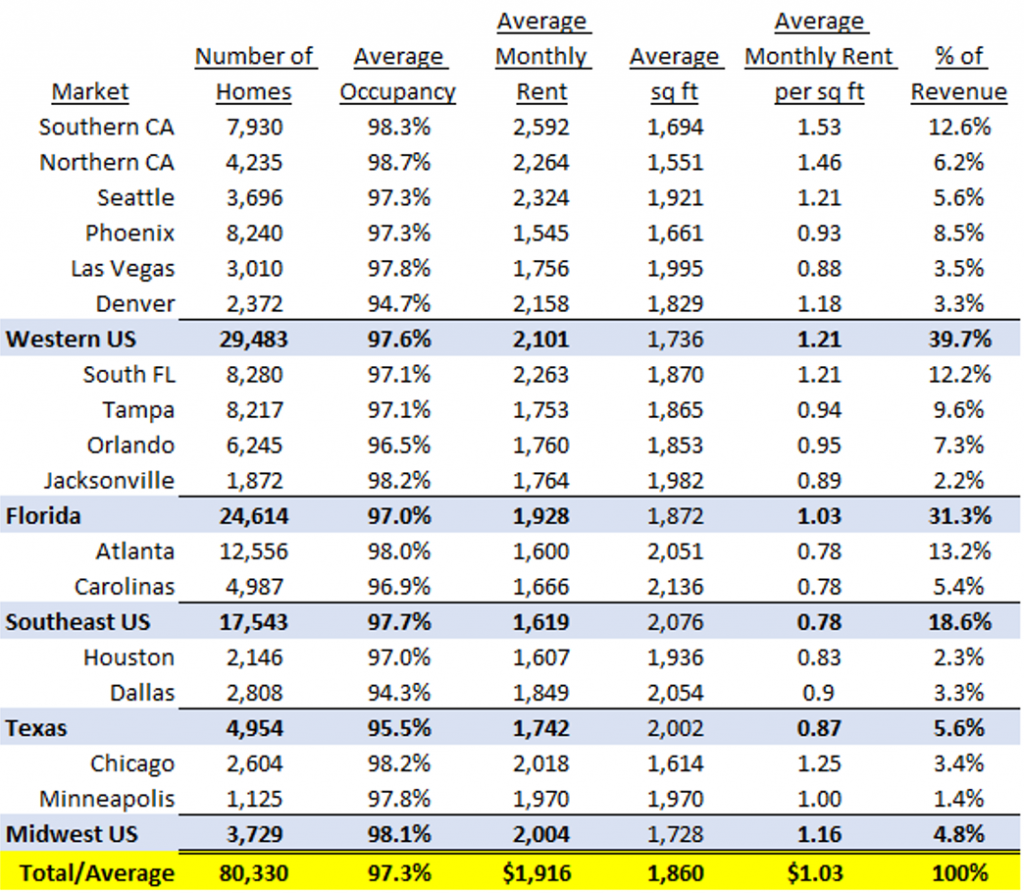

The first institutional operator to stand up a single-family rental business, Invitation Homes, is still the largest. The company owns more than 80,000 homes across 16 markets (Exhibit 1), primarily across the Western United States (40%), Florida (31%) and Southeast United States (19%). Invitation Homes specializes in single-family homes for upper-middle-income renters with average home size of 1,860 square feet, monthly rent of $1,916 and average household incomes of $74,000.

Exhibit 1: Invitation Homes single-family rental portfolio summary

Note: Portfolio summary information for the three months ended 3/31/2021. Totals/averages include 7 houses in Nashville where the company is in the process of exiting the market.

Source: Invitation Homes Q1 2021 10-Q, Amherst Pierpont Securities

The performance of the single-family rental sector, which had already been strong due to the structural shortage in housing a decade in the making, has improved sharply over the course of the pandemic. Analysis of Invitation Homes recent quarterly results illustrates several trends seen across the sector (Exhibit 2):

- Demand for detached single-family homes due to the pandemic has increased occupancy rates

- Average monthly rent growth increased by 3.5% year-over-year, while rent growth for new leases at Invitation Homes climbed 8.0% year-over-year during the quarter ended March 31, 2021, compared to a 2.0% year-over-year increase during the first quarter of 2020

- Turnover rates declined as fewer tenants moved, in part due to the rapid price appreciation of single-family homes for sale and the shrinking of supply, keeping more prospective new home buyers out of the market, and

- The average number of days a single-family rental property goes unoccupied as tenants turn over has dropped

Exhibit 2: Invitation Homes single-family rental performance metrics

Note: average monthly rent represents average monthly rental income per home for all occupied properties over the measurement period and reflects the impact of non-service rent concessions and contractual rent increases amortized over the life of the related lease.

Source: Invitation Homes Q1 2021 10-Q, Amherst Pierpont Securities

On the downside, the Covid-19 pandemic has raised uncollected rents. The company has experienced an increase in uncollected rents as some tenants have struggled with loss of income due to the economic shutdowns. Prior to the pandemic Invitation Homes had 0.4% of gross rental income not collected during the first quarter of 2020. Bad debt rose to 2.3% of rental income during the first quarter of 2021.

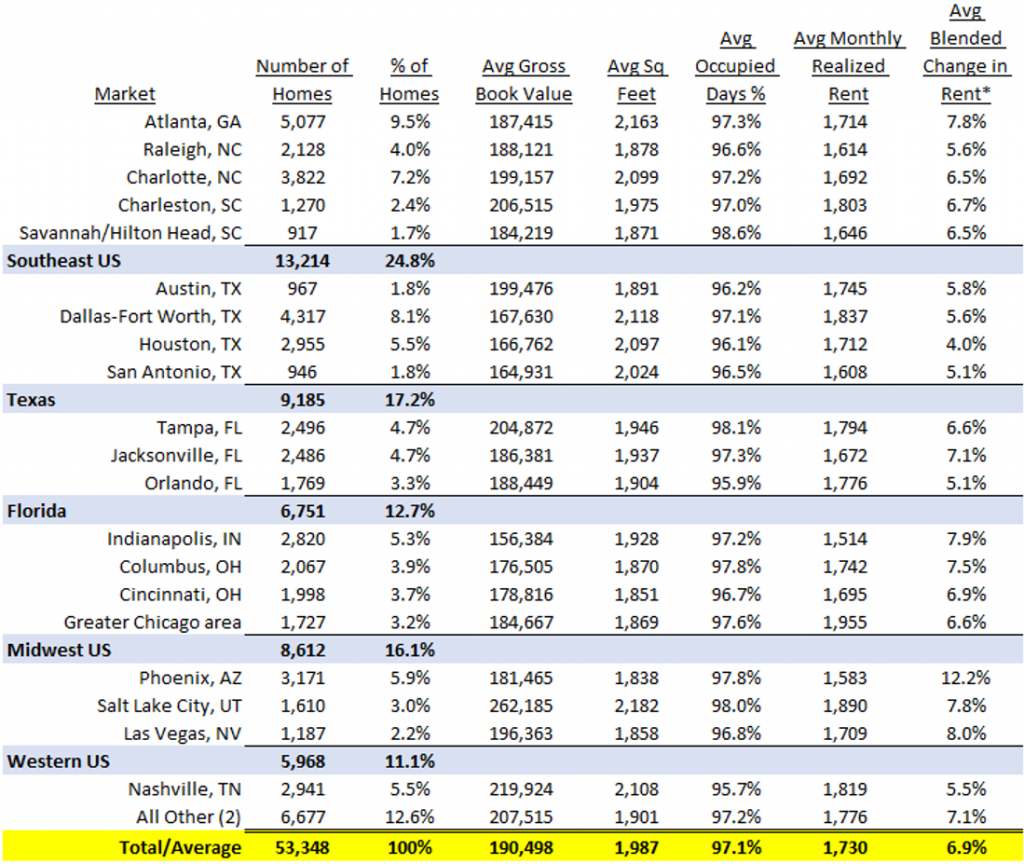

American Homes 4 Rent pushes towards “built-for-rent”

The performance and metrics of the second largest single-family rental operator, American Homes 4 Rent, are very similar to that of Invitation Homes over the past year. This is not surprising as American Homes 4 Rent targets a similar market segment with average home size just under 2,000 square feet and average monthly rent of $1,730. Performance through the first quarter of this year is quite similar (Exhibit 3):

- Average occupancy rates rose to 97.1% for the first quarter of 2021, while tenant turnover declined

- Average blended rent rose 6.9% while average monthly realized rent—similar to Invitation Homes average monthly rent growth—increased by 3.3% during the quarter

- Overall revenue growth was also higher, though it was modestly offset by an increase in uncollectible rents due to the pandemic.

Exhibit 3: American Homes 4 Rent single-family rental portfolio summary

Note: *Average blended change in rent represents the % change in rent on all non-month-to-month lease renewals and re-leases during the 3 months ended 3/31/2021, compared to the annual rent of the previously expired comparable long-term lease for each property. Data as of the three month period ended 3/31/2021.

Source: American Homes 4 Rent Q1 2021 10-Q, Amherst Pierpont Securities

The geographic concentration of single-family rentals between the two companies shows some modest differences, but overall reflects the heavy footprint of properties in the Sun Belt (Florida, Texas, Arizona and Nevada), the US Southeast and the Western US. American Homes for Rent does have 16% of their rentals in the Midwest US and 5.5% in Nashville – two areas where Invitation Homes is either exiting entirely or has a very minor presence. Otherwise, the major difference between the two is that American Homes 4 Rent favors the Southeast (25% of properties) while Invitation Homes has their heaviest concentration in the Western US (40%).

Unlike Invitation Homes, American Homes 4 Rent has also been actively developing built-for-rent properties in order to grow their single-family portfolio. During the first quarter of 2021 the company added 580 homes to their portfolio. These included 299 homes developed through their internal new construction program and 281 homes which they bought from third-party developers through their National Builder Program or through traditional acquisition. These additions were partially offset by 180 homes sold during the quarter. The company invested $180 million during the first quarter of 2021 primarily to build and acquire new properties. According to a report by Hoya Capital Real Estate, the company is planning to invest between $1.2 billion and $1.6 billion of total capital this year to add 3,500 homes to its wholly-owned and joint venture portfolios, including 1,900 to 2,200 homes through its internally operated new construction development program. By contrast, Invitation Homes plans to add about $1 billion in homes this year, about 85% of which are expected to be purchases of existing homes and 15% may be bought new from homebuilders.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.