The Long and Short

Kohl’s Inc. has further spread upside as leverage declines

This material is a Marketing Communication and does not constitute Independent Investment Research.

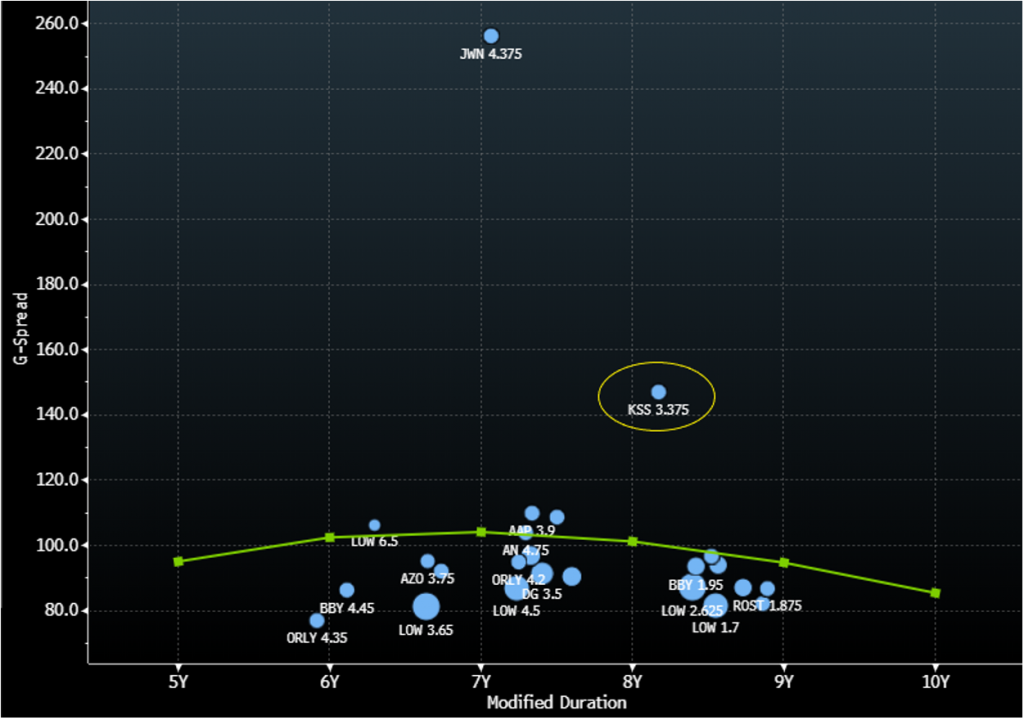

After posting first quarter results that exceeded expectations and repaying approximately $540 million of debt, Kohl’s Inc. (KSS) is moving much closer to hitting its leverage target of 3.0x. While not the widest trading credit in the investment grade retail space – as Nordstrom (JWN) has captured that spot – it has the greatest potential to trade closer to pre-pandemic spreads by year-end 2021, with the company’s 10-year bonds offering significant upside for investors.

Focus on debt reduction has brought KSS’ total debt (excluding leases) to its lowest level in over 10 years. Leverage should improve as EBITDA returns closer to $2.0 billion on an annual basis. The company’s 3.375% 2031 bonds offer the best potential value: they are currently trading at +143 bp (+146 bp g-spread – 3.05% yield) and have recently traded as tight at +135 bp. These spreads could tighten to the +120 bp area if results continue to outpace expectations and the company’s leverage target is achieved before year-end.

Exhibit 1. 10-year BBB Retail Curve

Source: Bloomberg TRACE; Amherst Pierpont Securities

Long History of Prudent Capital Management

KSS has long maintained a conservative balance sheet as management values its IG credit ratings, and the pandemic was no exception. In fact, we note that KSS has maintained an IG rating for over two decades. While the pandemic hit all retail peers exceptionally hard, KSS quickly shifted focus to debt reduction in an effort to help limit the deterioration of its credit metrics. We note that KSS ended the most recent quarter with total debt (excluding leases) of $1.9 billion, which is down from $3.5 billion in the year-ago period. Adjusted leverage now stands at 4.2x and should get to the 3.0x area by year end, as EBITDA returns to more normalized levels. Additionally, while supply chain disruptions have plagued the retail sector, KSS navigated the headwinds quite well and moved to bring inventory levels closer to the buying environment. As such, inventory is down 25% year-over-year. Management plans to monitor inventory levels quite closely to better match buying patterns and reduce its level of clearance promotional strategies, which should help support margins. KSS believes that its prudent to not build inventory levels too quickly but has increased the frequency of store deliveries to make sure that it is prioritizing inventory levels in growth areas (namely the women’s business line).

Liquidity Remains Strong

Even as the pandemic winds down, there is likely to be some disruptions along the way. That said, we believe KSS remains in a strong liquidity position to fuel its growth strategy and manage any further headwinds. KSS ended the quarter with cash on hand of $1.6 billion and also maintains an untapped $1.5 billion revolver. The cash position is supported by solid free cash flow generation, which totaled $1.3 billion on an LTM basis. KSS is returning to shareholder rewards, but we note that they are expected to remain within the confines of free cash flow. The board recently approved a $0.25 common dividend, after suspending the dividend for nearly a year. The new dividend is approximately one third of what the company was paying pre-pandemic. KSS also plans to repurchase between $200 million-$300 million of shares in 2021. We note that KSS spent $46 million on buybacks in 1Q and we expect that pace to continue per quarter. That said, shareholder rewards will likely total between $350 million-$450 million for the year. We estimate that KSS will generate at least $500 million of free cash flow in fiscal 2021, with potential for upside to that number should results continue to exceed expectations.

Exhibit 2. KSS Key Balance Sheet & Cash Flow Items 1Q21

Source: KSS Company Presentation

New Year New Outlook

Given the strong start to the fiscal year, management raised full year guidance. Management chose to approach its updated outlook prudently given the uncertainty to how the recovery unfolds. That said, there is potential for further upside should the pace of recovery continue. Net sales are now expected to grow in the mid-high teens area, up from previous guidance of mid-teens. The operating margin is now expected to be in the 5.7%-6.1% range, which is up from original expectations of 4.5%-5.0%. Lastly, EPS was raised from the $2.45-$2.95 range to a range of $3.80-$4.20. The guidance now assumes interest expense of $270 million which is lower than previous expectations given the recent debt reduction. While management has been managing costs conservatively, they expect SG&A expense in 2Q to be higher than the rate witnessed in 1Q as the company invests in its partnership launch with Sephora (expected this fall).

Managing Activist Investors

As if the pandemic was not hard enough, KSS management felt the heat of a group of four activist investors (Macellum Advisors, Legion Partners Holdings, Ancora Advisors and 4010 Capital) earlier this year. The group, which took a 9.5% equity stake, proposed nine directors to be elected to KSS’ board after citing equity underperformance which they believe is the result of operating mishaps. The activist investor group believes that KSS can benefit from improvements in merchandise mix (branded versus private label), as well as better inventory management and a focus on e-commerce fulfillment. Furthermore, the activist group is in support of KSS liquidating real estate holdings via sale lease-back transactions. KSS management was able to appease the activist group with a settlement agreement that included two seats on the board and an additional independent board member that both parties agree upon. While KSS kept its share buyback expectation in the $200 million-$300 million range for the year, it did increase its repurchase authorization to $2.0 billion. We note that as of 4/9/21, KSS had $697 million of authorization remaining under its existing program. Given management’s commitment to IG ratings, we do not expect share repurchases to increase until management achieves is leverage target.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.