The Big Idea

A heavy lift to higher longer rates

Steven Abrahams | May 21, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

The market has seen real inflation in the last few months and rising expectations of more to come, but actual interest rates have moved up surprisingly little. The reason: an implied massive surplus of investable cash ahead. That almost certainly means pushing up interest rates will become a heavier lift than a casual observer might expect. Low rates have a long way to go, along with their implications for asset-liability managers, the yield curve, corporate balance sheets and the appetite for yield.

A puzzle in rates

The puzzle is straightforward: longer interest rates have returned to where they stood before Covid, expectations of inflation have danced much higher but expectations for real rates—the rate where supply and demand for money clears after covering inflation—have completely offset the inflation bump. Look at 10-year Treasury rates since the beginning of 2020 (Exhibit 1). Today’s nominal 10-year rate in the 1.60%s has returned to pre-Covid levels and implied 10-year inflation has jumped from 168 bp to 249 bp. But real rates have dropped from 0 bp to negative 82 bp, offsetting the inflation rise.

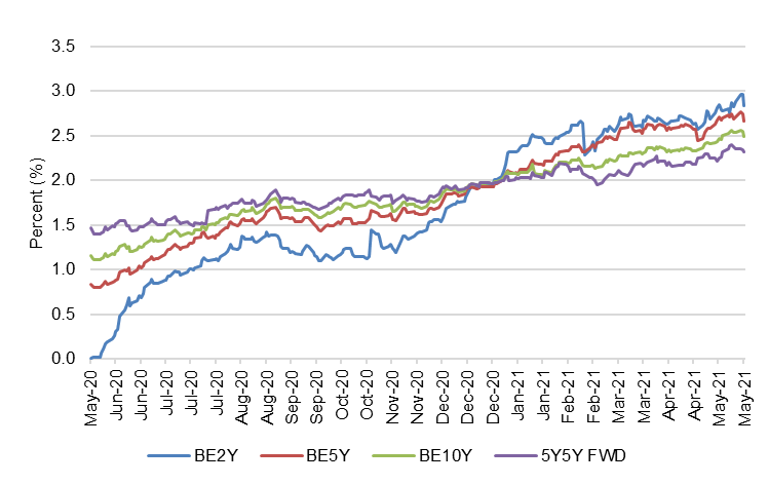

Exhibit 1: Return to pre-Covid rates, higher implied inflation, lower real rates

Source: Bloomberg, Amherst Pierpont Securities

Make no mistake, the market gets the inflation story. The Fed has sketched a clear path of inflation running high this year from basis effects and reopening before drifting back towards a 2% target. Inflation implied by the yield spread between Treasury notes and TIPS has hit the highest levels in years. Average inflation over the next two years is expected to be 280 bp. Over the next five years, it is expected to be 262 bp and over the next 10 years, 232 bp. Investors get the message. Higher now, lower later.

Exhibit 2: Breakeven inflation prices in higher inflation now, lower later

Source: Bloomberg, Amherst Pierpont Securities

It’s all about the cost of money after inflation

The problem for the intuition that higher inflation leads lockstep to higher rates is market expectations of a massive supply of savings and investment and tepid demand to borrow. Lots of supply, limited demand. That depresses the cost of money. That is the message in low and even negative real rates. And there are good grounds for this expectation:

- Massive liquidity. The Fed and global central banks have poured liquidity into the financial system on a completely new scale during Covid and arguably conditioned the system to expect high levels of liquidity in the future. Bank regulators seem inclined to support a system with high levels of reserves, and that was true even before Covid following the September 2019 stresses in repo markets. It will likely take years to draw down reserves. Preferences for higher bank reserves come on top of the case made by former Fed Chair Bernanke for a global savings glut, with central banks outside the US holding high balances of currency reserves. The glut may have moderated, but it has not gone away. Consumers have saved more in the last year, but it is too early to make the case that will persist.

- Potential low growth and low investment demand. It is hard to separate expected growth from investment demand; growth can draw out investment demand and investment demand can drive growth. But we have seen both run below historic averages leading up to Covid. US labor force growth has been low and slipped further during Covid, and productivity has run low, too. Over the next few years, productivity growth may even run below the roughly 1% average of the last decade as many low-productivity jobs in retail and travel return. Labor force and productivity are the gears of GDP, and both have turned slowly. Levels of capital investment have generally dropped. We may see a rebound in capital investment as economies reopen, but it is unclear investment will go beyond niches left open by Covid.

- Demand for safe assets. If lots of investable cash and limited demand to borrow were not enough to keep rates low, demand for safe assets arguably has gone up. Some analysts frame this as a response to rising global concern about various macroeconomic risks, but it is much simpler to point to regulatory requirements for banking system liquidity. Much of the cash pumped into the economy by central bank policy ends up on bank balance sheets, and banks have regulatory liquidity incentives to invest a sizable share of this inflow in excess reserves, Treasury debt and other safe assets. Within the last year especially, banks have done exactly that.

- Demographics. This largely complements other factors. The retirement of the Baby Boom generation has slowly reduced labor force participation [since 2008] along with the average level of experience, contributing to slower growth and lower productivity. Retirement typically raises savings and encourages safe assets for preservation of capital.

The Fed has two implied targets

The Fed has pegged its median long-term fed funds rate at 2.5%, not far above the current yield on the 30-year bond. The Fed basically is saying it expects 2% inflation and a 0.50% real rate. Current negative real rates make sense; they should run below the Fed’s implied 0.50% real rate target to get the economy back on its feet. But it is a long way and a heavy lift to get real rates from negative 82 bp to positive 50 bp, and it depends less on boosting inflation expectations than it does on realigning expectations for the supply and demand for money.

The investment implications of lower rates

Asset-liability managers sensitive to the level of longer rates have revised their expectations down sharply over the last year. Life insurers MetLife and CNA, for example, have lowered their US 10-year rate assumptions over the last year by 100 bp to 2.75%. Life insurers Brighthouse and Principal lowered their US 10-year rate assumption by 75 bp to 3.00% and 3.25%, respectively. And Lincoln National and Prudential both dropped their assumption by 50 bp to 3.00% and 3.25%, respectively. That helps insurers price new business, although assumptions above 3.0% look unrealistic. Older books of liabilities priced at higher rates will likely force their managers to take more risk.

If equilibrium comes around 2.50%, then yields at the long end of the curve have limited room to move higher and the likelihood of flattening increases. The 5s30s curve has struggled to steepen beyond its late February peak of 160 bp and looks more likely to flatten. The 2s10s curve could steepen as the Fed begins to taper but before it hikes, but hiking looks likely to bring a replay of the mid-2000s flattening.

Selling caps can make sense, too, whether outright or embedded in CMO floaters or other securities. The only caveat to this strategy is that the 2s10s curve may steepen before it eventually flattens; the steepening could temporarily put caps in-the-money forward.

A slow path to higher rates and a low terminal rate has clear implications for corporate credit: borrowing will remain inexpensive, so interest expense on corporate balance sheets should remain low. Traditional measures of corporate leverage such as debt-to-EBITDA are high, but EBITDA-to-interest-expense is at healthy levels compared to most points in the last 50 years. Even low growth can be a good scenario for credit as long as it come with low rates. And that looks like what we are in for as far as the yield curve can see.

Finally, the appetite for yield should have legs, too. Low risk-free rates should push portfolios that need income into higher tiers of risk. Not only should massive liquidity keep risk-free rates low, it should lower risk premiums, too. The distribution of future spreads on risk assets look tilted toward the tight end.

* * *

The view in rates

Rates at the very front end of the yield curve continue to sink. Overnight Treasury repo has gone negative in recent sessions, and 3-month LIBOR has dipped even further to a new record 15 bp. SOFR is still pinned at 1 bp but looks vulnerable unless the Fed lifts the rate on its reverse repo facility from the current 0 bp. Cash continues to swamp the money markets and lap at the sides of the tub.

The 10-year note has finished the most recent session at 1.62%, basically unchanged from a week before. It is the battle royal between inflation expectations and real rates.

The Treasury yield curve has finished its most recent session with 2s10s at 147 bp, effectively unchanged week-over-week. The 5s30s curve has finished at 150 bp, flatter by 3 bp.

The view in spreads

The latest Fed minutes raised the specter of tapering, and comments after their release by Philly Fed President Harker amplified the discussion. MBS spreads nevertheless should stay tight and the dollar roll in MBS special as long as Fed and bank net buying continues to soak up almost all net MBS supply. The nominal spread between par 30-year MBS and the interpolated 7.5-year Treasury yield closed recently at 63 bp, just 4 bp off the tightest level in MBS market history.

In credit, support from insurers and money managers should keep spreads tightening. Investment grade spreads have generally outstripped high yield on the back of bids from insurers and money managers, but high yield should get its due. Weaker credits should outperform stronger credits, with high yield topping investment grade debt and both topping safe assets such as agency MBS and Treasury debt. The consumer balance sheets has come out of 2020 stronger than ever—at least on average—and consumer credit should outperform corporate credit.

The big risk to spreads should come when the Fed starts making noise about approaching its targets for employment and inflation and tapering asset purchases. Keep those antennae tuned.

The view in credit

By the end of 2021, US GDP could be above levels projected before Covid for late 2021. That would represent one of the fastest and strongest rebounds from recession in US history. Consumers should continue to build strength. Aggregate savings are up, home values are up and investment portfolios are up. Consumers have not added much debt. Corporate balance sheets have taken on more leverage, although mitigated by strong cash balances and low interest costs. EBITDA-to-interest-expense is at healthy levels. Strong economic growth in 2021 and 2022 should lift most EBITDA and continue easing credit concerns. Eventually, rising interest expense should compete with EBITDA growth. But not for a long time.