Uncategorized

The sprint for substantial further progress

admin | April 9, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

The Fed has said it plans to keep securities purchases rolling until the economy has made “substantial further progress” toward maximum employment and 2% inflation. But officials have been purposefully vague about exactly what that means. The economy is reopening, and we are likely to see sharp upward movement in both employment and inflation over the next several months. At least on the labor side, we could see substantial further progress by August.

Starting Point

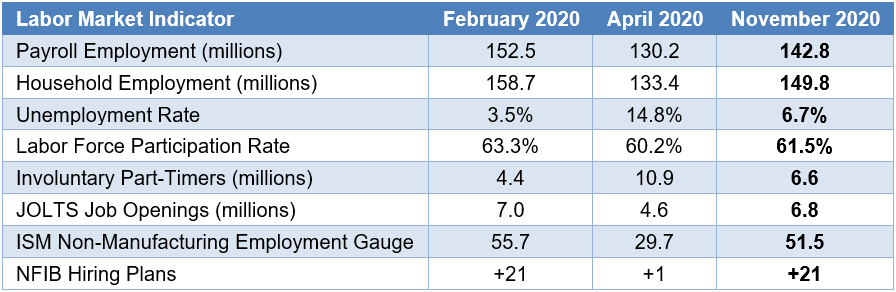

The FOMC rolled out the “substantial further progress” forward guidance language for its balance sheet strategy back in mid-December. The starting point for benchmarking further progress should be the November data. The labor market then had rebounded from the economy’s low point in April but stood short of the mark before the pandemic began (Exhibit 1).

Exhibit 1: Initial Progress

Source: BLS, ISM, NFIB.

The labor market still had made good progress by last November. In fact, most of the indicators were more than halfway back to their pre-pandemic levels. However, as Chair Powell and other Fed officials have made clear, the economy was still in a very deep hole, with payroll employment still 10 million shy of the February 2020 level and the unemployment rate several percentage points higher.

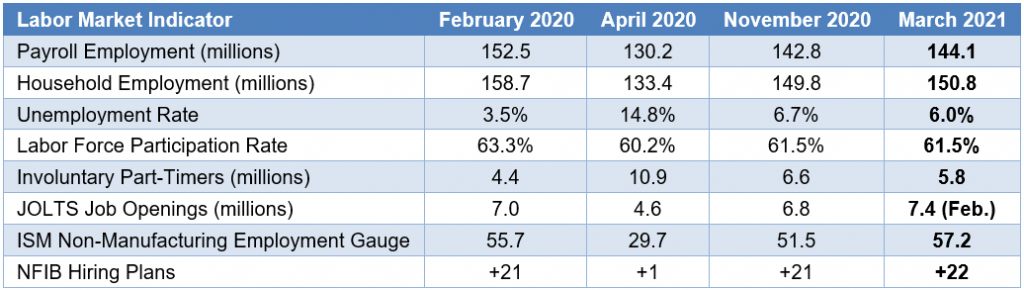

The economy made only limited progress through the winter as the pandemic ratcheted up sharply, forcing many states to reimpose restrictions on business activity. Over the past month or two, however, the labor market appears to have gained considerable ground (Exhibit 2). The improvement is likely to gather momentum in the spring, as vaccinations are allowing for the removal of business restrictions in a number of states already, with others likely to follow suit once cases and hospitalizations decline further.

Exhibit 2: Further Progress

Source: BLS, ISM, NFIB.

Progress since November

For each variable, we can assess the “progress” made since the FOMC’s initial forward guidance offering. For payroll and household employment, the gains have been limited. There was not much growth at all in the winter months, followed by a strong payroll advance in February and an explosive rise in March. As a result, payroll employment is now about 8.5 million short of the pre-pandemic level, while the household survey gauge of employment is 8 million short. The unemployment rate has dropped by another 0.7 percentage points but remains 2.5 percentage points above the February 2020 reading. Involuntary part-time workers have also continued to move back toward levels seen before the pandemic. The one variable that has not yet made up significant further ground is labor force participation, as the LFPR in March was unchanged from November.

The continued low level of labor force participation is creating a shortage of available workers as firms look to staff back up. The JOLTS measure of job openings has surged in recent months and, as of February, exceeded the readings just before the virus hit. Similarly, the ISM non-manufacturing employment index and the NFIB measure of small business hiring plans both are above their February 2020 levels. Even as employment levels are still depressed, from the perspective of prospective hirers, the labor market looks very tight, remarkably similar to what we were seeing prior to the pandemic, when the unemployment rate was sitting at 50-year lows. Another marker is online job postings. The job-search site Indeed reported that job listings as of April 2 were 16.4% above the level on February 1 of last year.

Potential workers look likely to flood back into the job market as soon as more people are vaccinated and feel safe returning to the workplace and as soon as schools fully reopen, freeing parents to work outside the home daily. The former should be accomplished within the next two months. The latter should also be mostly achieved by then, though for a handful of big-city school districts, a return to full in-person learning may have to wait until the beginning of the next school year. A third key development will be the expiration of supplemental unemployment benefits in early September. Currently, with an extra $300 per week in payments available, there are still millions of lower-wage workers who are financially better off collecting benefits than going back to their former jobs. This is undoubtedly exacerbating the shortage of available workers that firms are currently facing.

Defining “substantial”

Fed officials have been intentionally vague about what would constitute “substantial further progress.” Initially, narrowing close to half of the November 2020 employment shortfall relative to February 2020—around 5 million jobs—seemed like it might be enough. After listening to policymakers over the last three months, it might take even more progress to satisfy “substantial.” However, the March payroll jump, over one million including revisions, represents a mere down payment on what should be a massive hiring spree in the spring. Payrolls should advance by at least a million a month on average over the next three to four months. A run of that magnitude would bring the level of employment to a point where Fed officials would have an increasingly hard time denying “substantial further progress.” In fact, the the labor market will likely meet the FOMC’s standard for tapering by the summer—maybe August or at the latest September—though the inflation side of the equation will be a more complicated assessment and a discussion for another day.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.