By the Numbers

New twists in private CRT

This material is a Marketing Communication and does not constitute Independent Investment Research.

The market for private credit risk transfer may be getting some new players. A pair of banks in recent weeks—including one with a ‘BB+’ rating—have issued private CRT deals, and several factors point toward more issuance from banks looking to offload risk from retained mortgage portfolios or warehouse lending facilities.

Banks hoping to issue CRT have run into snags in the past. Transactions have to pass muster with bank regulators, and the transactions are not as straightforward as securitization—simply transferring loans off the balance sheet and issuing liabilities backed by the cash flow of the loans. CRT does not actually use the cash flow from the loans to pay principal and interest on deal liabilities, so the CRT issuer bears that obligation. That makes CRT a hybrid of both mortgage and unsecured corporate credit risk. To date, corporate credit has been a high hurdle for smaller banks hoping to issue private CRT. The cost of transferring credit should be higher for smaller, lower-rated issuers, diluting the potential benefits associated with transferring the mortgage credit risk.

While banks like JPMorgan continue to issue CRT, a transaction announced this week by Texas Capital Bancshares, a Dallas-based bank with just over $37 billion in total assets, likely came as a surprise to many market participants. The bank issued a $275 million Credit Linked Note referencing $2.2 billion of notional loan exposure held by the bank, according to a press release. The issuance allows “the Company to expand the Warehouse Lending program and better serve clients in all market environments.” The transaction is a private placement, so details on the deal are sparse. The deal appears to be a milestone in that it is the first CRT issued by a smaller, lower-rated bank as the company’s outstanding unsecured corporate issuance carries a BB+ rating.

Calculating the cost and benefits of CRT

An analysis of JPMorgan’s recently issued JPMorgan Wealth Management 2021-CL1 transaction suggests that the costs associated with transferring credit risk on relatively pristine collateral by a highly-rated issuer is relatively low and should create incentives for other issuers to follow suit. The deal references loans originated by JPMorgan Chase Bank through their Wealth Management Mortgage channel and retained by the bank. Principal payments are allocated to the notes based the performance of the reference pool of mortgages while the interest payments to the notes are unrelated to pool performance—absent the potential impact of loan modifications that could reduce note coupons. The deal is fully unsecured, meaning that neither the principal or interest associated with the loans nor the principal generated from the sale of the notes will be allocated to pay principal or interest on the notes. As a result, the rating on the notes is capped at JPMorgan’s senior unsecured debt rating of Aa2 by Moody’s.

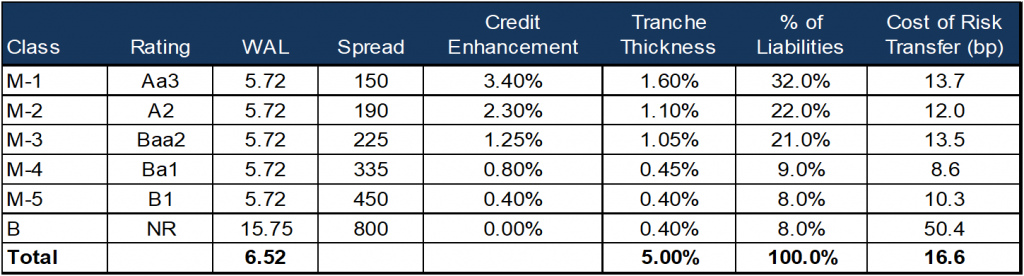

Despite being a hybrid of mortgage and unsecured corporate risk the cost to transfer the first 5.0% of pool losses as well as modification losses associated with the reference loans appears to be just over 16 bp based on the structure and estimated spreads on risk placed. (Exhibit 1)

Exhibit 1: Calculating the cost of private CRT JPMWM 2021-CL1

Source: Moody’s, Bloomberg LP, APS

Assuming a 50% risk-weighting and with JPMorgan’s current Tier 1 leverage ratio of 15%, the bank would have to hold 7.5% of regulatory capital against the position. At a current return on capital of 11.3%, the bank would have to pay out 85 bp of dividend yield on the capital held against the position instead of a cost of just over 16 bp to free up that capital, potentially making CRT a viable option for a larger swath of their loan portfolio assuming no residual economic or regulatory capital held against the position.

Why now might be the time for more private CRT

Away from the relatively low cost of risk transfer there may be a few other reasons why bank issuance of CRT may increase in the not too distant future. The most meaningful potential driver of private CRT issuance is the sheer amount of monetary and fiscal stimulus that has been implemented in the wake of the pandemic as trillions of dollars have been fed into the system in an effort to keep the economy afloat. This cash has in large part made its way onto bank balance sheets in the form of deposit liabilities. And as deposits grow, banks need more assets to pair against those liabilities. As assets grow, banks’ leverage will increase. Assuming some amount of banks asset growth will come in the form of retained mortgage loans, CRT appears to be an elegant solution for banks to both transfer mortgage credit risk and free up associated risk-based and economic capital.

The potential systemic need for regulatory capital relief may facilitate the second factor that could help push more private issuance, namely more support for these transactions by bank regulators. The path to regulatory approval for bank issued CRT has been a bumpy one. JPMorgan tried twice in 2016 only to have the transactions subsequently deemed insufficient to achieve regulatory capital relief by the OCC. However, since 2019, JPMorgan has issued a steady, albeit small, amount of private CRT to the market. This steady stream of issuance suggests that the deals have likely achieved the bank’s desired capital management metrics.

Additionally, with Fannie Mae still on the sidelines, it likely paves the way for the potential investor demand for their CAS transactions to be met by supply from private issuers. Obviously, private CRT is not completely fungible with GSE issuance given the incremental counterparty credit risk in private deals and the likely differences in collateral attributes referenced in the private pools. However, it seems likely that some amount of cash that was previously allocated to Fannie Mae’s new issue CRT could cross over to the private market.

But what about the little guys…

Counterparty credit risk appears to be the biggest potential impediment to smaller banks being able to tap the market, at least until recently. While it’s unclear what structural mechanisms the Texas Capital deal may or may not have employed to get over this hurdle there are certainly a couple of structural innovations that may help mitigate a good amount of the counterparty credit risk. First as to principal, unlike the JPMorgan deals, a lower-rated issuer could fund the principal due to the notes with the proceeds from the sale of them, commonly referred to as a fully funded Credit Linked Note. In a funded CLN, the par principal from the sale is reinvested into permissible investments that will generate the coupon associated with the benchmark index that the note coupons are tied to.

However, even in this structure, investors rely on the issuer to be able to pay the spread on the notes over and above the benchmark index. In the JPM structure, the funds to pay those spreads are disbursed by the bank on a monthly basis. In the case of a smaller issuer with a lower credit rating, issuers could potentially pre-fund a reserve account where they would deposit cash to cover some portion of the expected interest payments in an effort to offset some amount of the counterparty risk. Other solutions for lower rated counterparties could be partially hedging the counterparty risk with credit default swaps or attaching a financial guarantor to the interest payments. While the conventional wisdom to date is that private CRT issuance would be limited to only the largest institutions there may ultimately be ways for others to tap the market.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.