The Big Idea

Peeling the inflation onion

Stephen Stanley | March 5, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

The Fed has laid out an approach to inflation that sees it in a few layers. First comes the imminent fluctuations in year-over-year inflation caused by gyrations in prices during the early months of pandemic. Then comes any temporary burst that accompanies initial full reopening of the economy. And finally, longer-run underlying inflation is laid bare. Chair Powell has stated clearly that the Fed plans to look through the first two layers and focus on the longer term, but financial market participants may not prove quite as patient.

First layer of the onion: basis effects

Chair Powell’s formulation feels a lot like peeling an onion. The first and most superficial layer of the inflation picture will be the basis effects that will produce a sharp acceleration in year-over-year inflation in March and April, as the highly unusual declines in inflation in the early days of the pandemic fall out of the 12-month calculation. In March and April 2020, the headline PCE deflator declined by 0.3% and 0.5% respectively. The core component slid by 0.1% in March and by 0.4% in April. If we plug in even modest 0.1% rises in for March and April 2021, the year-over-year advances will accelerate by about 100 bp for the headline gauge and 70 bp for the core, which would take headline inflation over 2.5% and core inflation above 2% on a year-over-year basis.

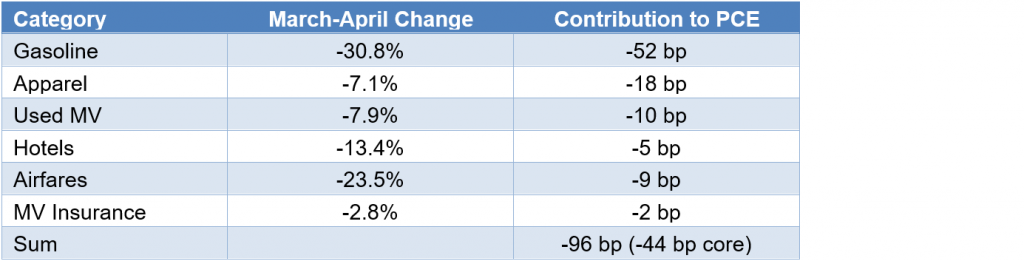

It is worth noting that price six categories alone accounted for close to a full percentage point drop in headline inflation last March-April and for almost half a percentage point for the core (Exhibit 1).

Exhibit 1: March-April Drop in PCE Deflator Prices

Source: BEA.

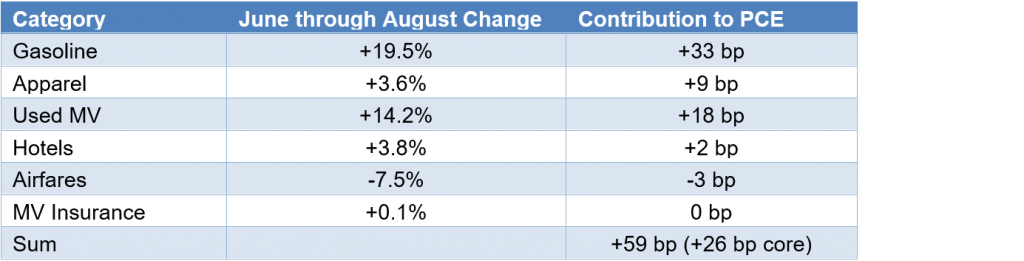

A big part of the reason the Fed can afford to ignore what would ordinarily be a disconcerting acceleration in year-over-year inflation is that much of it will quickly reverse. Inflation bounced back in June, July and August, with increases in the PCE deflator of 0.5%, 0.3% and 0.3%, while the core index posted three consecutive 0.3% rises.

The same six price categories that helped drive the March-April price declines then offset more than half of the earlier drop from June through August (Exhibit 2). Year-over-year advances consequently are likely to peak in April and then come back down over into the summer, though I would not be surprised to see the figures remain above 2% for both total and core inflation throughout the period.

Exhibit 2: June-July-August Rebound in PCE Deflator Prices

Source: BEA.

In any case, Fed officials have made clear that they are unlikely to react to these swings in the year-over-year readings over the next several months. Financial market participants may not be so sanguine, but investors seem likely to take their cues, at least to an extent, from the Fed.

Second layer of the onion: reopening pop

Given the immense stash of liquid assets held by households, when people are vaccinated and feel safe and the economy reopens, there is likely to be an initial rush of demand for a variety of goods and services inaccessible or undesirable to most during the pandemic. Airline and hotel bookings could explode, restaurants will likely be bursting at the seams with diners. And amusement parks, sporting events and a variety of other spectator venues will be in high demand. There is a decent chance that prices will rise, at least for a time, for many of these services, as firms try to manage a supply-demand imbalance.

This dynamic already is playing out in other sectors of the economy. Home prices have been surging since the initial lockdowns ended last spring, as households have fled renting in cities for the more open spaces of single-family homes in smaller cities, suburbs and rural areas, creating a persistent shortage of homes for sale. Recent ISM reports indicate that manufacturers are experiencing a similar experience, as many are facing explosive demand but have had difficulty with their supply chains. In the February ISM report, there was increasing talk of firms passing along higher costs to their customers.

This experience may well extend to consumer goods and services later this year, especially if households seek to deploy the bulk of the stockpile of savings built up over the last year relatively quickly.

Chair Powell and Fed officials have similarly instructed that they intend to ignore this second layer of the inflation onion. Powell has correctly pointed out that a 1-time spike in prices is distinct from inflation, which entails prices rising persistently. In the Fed’s view, as long as longer-run inflation expectations are steady, a sustained pickup in inflation would be difficult if not impossible. Powell and a number of other Fed officials also believe that the structural forces that have helped to keep inflation low for the last few decades remain in place.

While the Fed seems likely to steadfastly stick to their guns, this strategy amounts to having faith that a pickup in inflation will not kick off a self-sustaining cycle of upward waves in prices and wages that begins to feed on itself. Financial market participants may or may not choose to share the Fed’s faith on that count. What will investors assume if core inflation rises above, say, 2.5% in late 2021 or early 2022.

The core of the onion: long-term inflation trends

The lynchpin of the inflation puzzle revolves around the primary driver of inflation in the long run. Sadly, it seems that economics does not have a strong, widely-held answer to this question. For decades, the Fed took a Keynesian approach and assumed that prices were determined primarily by the degree of slack in the labor market and the resulting determination of wages, a Phillips Curve formulation. Having jettisoned that approach—or at least abandoning it in one direction, when the unemployment rate is low—Fed officials have very little insight into the structural determinants of an acceleration in the underlying trend in inflation.

Fed models have come to rely heavily on inflation expectations, and Chair Powell and others appear to put great faith in the fact that inflation expectations are well-anchored. However, this has a circular logic element to it. Inflation did not initially tick up in the 1960s because inflation expectations rose. In fact, it was quite the opposite. The public, including financial market participants, was quite surprised, perhaps it would be fair to say shocked, to see inflation accelerate as much as it did. It is true that inflation then continued to accelerate in the late-1960s and 1970s specifically because more was expected. Workers then demanded higher wages, setting off a wage-price spiral. However, we have very little modern experience with how long consumers would maintain low and steady inflation expectations in the face of rising prices. It is one thing when inflation spikes because of an oil shock, which consumers have been trained to understand is usually temporary and brief. It would be quite another for consumers to sit quiet and maintain 2% long-term inflation expectations when they are seeing faster increases in prices for a variety of goods and services. For how long would consumers accept that loss of purchasing power without demanding higher wages?

So, what other models are there for inflation? Is inflation a monetary phenomenon, as Milton Friedman declared? If so, then the shift in the Fed’s monetary policy strategy probably should have an impact on inflation expectations. At first, the Fed would see that as a good thing, because policymakers have been more worried about inflation expectations falling below 2% than rising too high. Several Fed officials have noted approvingly the recent rise in TIPS breakevens. However, that can easily turn against the Fed if financial markets and the public more generally comes to believe that the Fed is accepting a substantial pickup in prices that the public thinks may be persistent, even if the Fed does not.

How does fiscal policy play in? In the short run, by supplying households with so much extra cash, the federal government will have contributed heavily to the prospect of the second layer of inflation described above. If the federal government fails to address massive structural budget deficits, will financial markets and the public begin to worry that the policy mix is too easy? Will investors come to believe that the Fed will be unable to do what it needs to do on the monetary side because raising interest rates would create an unsustainable fiscal burden? In that case, we would be back to the late 1940s, a time when the economy overheated and inflation surged while the Fed stayed at the pre-modern equivalent of the zero bound.

And what impact will the aftereffects of the pandemic have on those downward structural forces that Chairman Powell is so confident remain in place? Can we really rely on globalization to continue to push down inflation, with trade tensions with China still high and the pandemic convincing many businesses to try to bring their supply chains home?

I have posed a number of questions that I do not have good answers for. I have a very open mind about how things could play out with regard to inflation over the next few years. I know that the Fed can control inflation, but I am very unsure as to whether the current FOMC would see a pickup in underlying inflation, if it occurred, in time to nip it in the bud or whether they would have the nerve to take the hard and unpopular decisions that would be required in such a scenario. One thing that I do sense is that the Fed is likely to prove far more patient than financial market participants if inflation does move substantially above 2% and it is unclear for how long it will stay high. Things may play out exactly as Chairman Powell laid out, but alternatively, things may pan out quite differently, in which case, financial markets would probably be in for a wild ride.