The Big Idea

Real investors take more risk

Steven Abrahams | February 5, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Investors in the safest corners of US fixed income are quietly taking risk with the buying power of their investments. Almost all Treasury debt and big parts of MBS, CMBS and corporate markets trade at yields that fail to cover market expectations for inflation. Current markets imply the risk of losing buying power is at its highest in decades. Investors looking for real and not nominal return will likely need to take other risk and lots of it.

The market expects Treasury debt investors to lose buying power after inflation

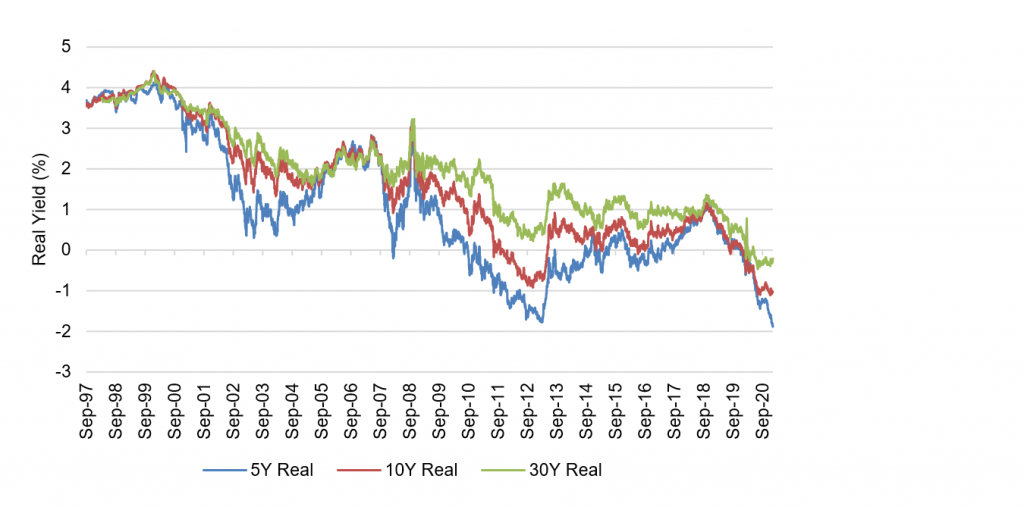

The market in Treasury Inflation Protected Securities implies rates of return likely after inflation in today’s Treasury notes and bonds. The 5-year TIPS, for example, imply a real rate on 5-year notes of -1.87%, the lowest since the Treasury started issuing TIPS in 1997 (Exhibit 1). Investors in 5-year notes will lose buying power at a compounded annual rate of 1.87%, the TIPS market says, and $1 invested now will buy $0.91 in today’s goods and services at maturity. Other TIPS markets also imply record low rates of real return. Markets in 10-year TIPS imply inflation will outstrip nominal 10-year yields for a -1.03% real return, and 30-year TIPS imply a -0.21% real return.

Exhibit 1: Implied rates on Treasury debt after inflation have reached record lows

Source: Bloomberg, Amherst Pierpont Securities

These implied negative returns come from investors with real money riding on inflation. An investor in 5-year TIPS today pays nearly $110 to own an instrument with a 0.125% coupon. If that investor just collected coupon and amortized the premium price down to par at maturity, the investment would yield -1.87%. But the principal balance on TIPS rises with inflation. TIPS investors presumably believe the principal balance over the next five years will rise to $110 and beyond to produce a positive real return—one where money invested today will buy the same set of goods and services in the future. To be indifferent to investing in a 5-year Treasury note at par yielding 0.46%, that breakeven rate of inflation would need to be 2.34%. If the TIPS pays coupon and its balance hits $111.58, the investor will just cover inflation. The 5-year note investor, however, will lose a compounded 1.87% in buying power a year—the difference between 2.34% inflation and the note coupon.

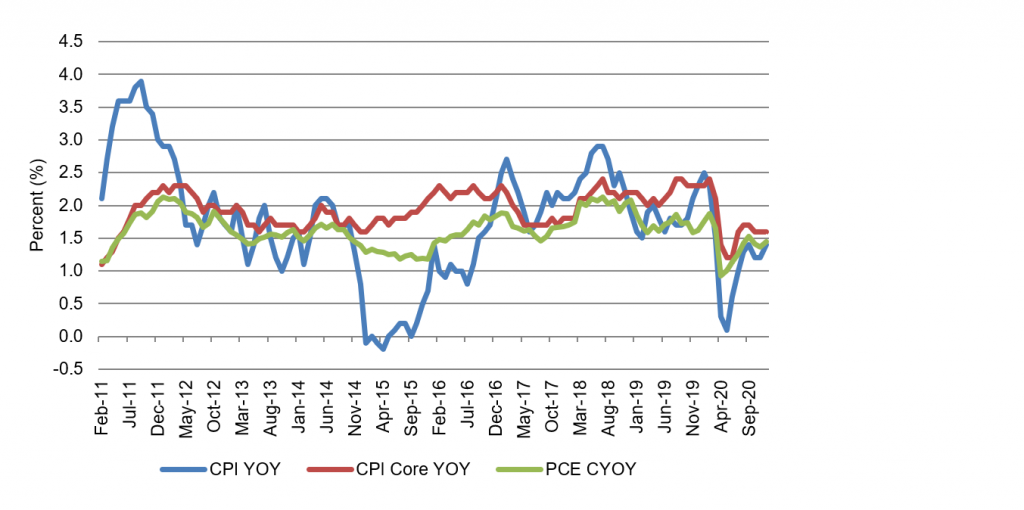

It is not just markets suggesting inflation could outstrip current nominal Treasury yields. CPI, core CPI and PCE printed year-over-year in December around 1.5% (Exhibit 2). And the most recent Philly Fed survey of professional forecasters showed a consensus 5-year PCE forecast of 1.79% and CPI forecast of 2.00%.

Exhibit 2: Realized inflation even recently has outstripped current Treasury yields

Source: Bloomberg, Amherst Pierpont Securities

Other investors could lose buying power, too

Other fixed income investors also stand to lose buying power if TIPS investors are right. The market in 15-year pass-throughs, for example, offers a nominal par rate 48 bp over the nominal 5-year Treasury yield, well below the 187 bp of spread above the Treasury curve needed to cover implied inflation. The market in 30-year pass-throughs offers a par yield 65 bp higher than the interpolated 7.5-year Treasury, also too little to cover implied inflation. After adjusting for prepayment options, agency MBS spreads approach or drop below the nominal Treasury curve and further below implied inflation. The Bloomberg Barclays Capital US CMBS 2.0 ‘AAA’ 8.5-year OAS comes in at 76 bp, also too little. The latest 10-year agency CMBS deal priced at a spread of 27 bp over the nominal 10-year Treasury note, well below the 103 bp need over the curve to cover implied inflation. Corporate ‘AA’ 10-year debt trades 53 bp over the 10-year Treasury and ‘A’ at 70 bp over, both too little to breakeven to implied inflation.

Record low real yields may reflect a powerful bid for safety and liquidity

The risk of losing buying power in the safest fixed income assets reflects the appearance of historically low yields at just the moment the Fed and other central banks are working aggressively to encourage higher inflation. Covid vaccines and fiscal stimulus have also added to inflation concerns. Still, nominal rates have stayed low, implying that investors in many assets put a tremendous value on safety and liquidity. Investors seem focused on getting nominal dollars back even at the risk of losing real dollars along the way.

A pending challenge for all portfolios—their real liabilities

All investment portfolios have at least some real liabilities, and some have more than most. Endowments that pay for facilities, faculty, staff and tuition rely on real return. Insurers that cover damage to homes, businesses and property need real returns. But all portfolios have some responsibility for the real operating expenses either of the portfolio itself or the larger organization—the bank, the investment manager, the pension or insurer—that sponsors the portfolio.

If global central bank policy and demand for safe assets keeps yields below expected inflation, investors will have to take risks to cover the loss of buying power. Duration, credit, liquidity, volatility and other risks all offer incremental return premiums. Longer ‘BBB’ corporate and structured credit cover inflation costs. A wide range of private debt covers inflation costs.

Of course, markets and forecasters can be wrong. Inflation implied by TIPS or published by professional forecasters may turn out to be way off the mark. Inflation could be benign. But the tremendous amount of cash sitting in the world’s safest assets has limited room for error. Inflation risk is there, and investors should diversify where possible into other exposures that should help keep real returns at acceptable levels.

* * *

The view in rates

Higher, at least in the long end of the yield curve, and steeper. The Biden administration’s $1.9 trillion stimulus package increasingly looks likely to pass through budget reconciliation, and the surge of cash and federal spending would likely push growth and concern about inflation higher. The Treasury yield curve has finished its most recent session with 2s10s at 106 bp, the highest in nearly four years, and 5s30s at 151 bp, the highest in at least five years. Inflation expectations measured by the spread between 10-year notes and TIPS have moved up 10 bp in the last week at 220 bp, the highest since late 2018. Volatility should remain steady.

A heavy supply of cash is reducing repo rates, Treasury bill yields and LIBOR. Yields on 2-year notes have slipped lower lately despite higher rates in longer maturities.

The view in spreads

Spreads should continue to tighten slightly despite being near or at historic tights in many assets. QE absorbs MBS, the relatively riskless spread asset, at least regarding credit. Fiscal stimulus, pandemic recovery and Fed policy should also keep spreads steadily tighter through 2021. Weaker credits should outperform stronger credits, with high yield topping investment grade debt and both topping safe assets such as agency MBS and Treasury debt. Consumer credit should outperform corporate credit.

The view in credit

Consumers in aggregate are coming out of 2020 with a $5 trillion gain in net worth. Aggregate savings are up, home values are up and investment portfolios are up. Consumers have not added much debt. Although there is an underlying distribution of haves and have nots, the aggregate consumer balance sheet is strong. Corporate balance sheets have taken on substantial amounts of debt and will need earnings to rebound for either debt-to-EBITDA or EBITDA-to-interest-expense to drop back to better levels. Credit in the next few months could see some volatility as Covid begins forcing shutdown of some economic activity and distribution of vaccines potentially hits some logistical potholes. But distribution and vaccine uptake through next year should put a floor on fundamental risk with businesses and households most affected by pandemic—personal services, restaurants, leisure and entertainment, travel and hotels—bouncing back the most.