The Long and Short

A faster than expected recovery favors basic industry

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

The sector weighting recommendation on basic industry (materials) changes in February to overweight from underweight. This reflects expectations for a more rapid global economic recovery than the market is currently anticipating. Excess and total returns were flat to negative for the month of January for the broad investment grade corporate bond index. A review shows REITs and finance companies were the top performing credit sectors, while energy appears to have been impacted by ratings agency announcements.

A summary of how APS expects sectors within the investment grade index to perform for the next several months on an excess return basis (total return net of commensurate UST return) are presented in Exhibits 1 and 2. These weightings serve as a proxy for how we recommend that portfolio managers should position their holdings relative to the broad IG corporate bond market.

Exhibit 1: APS Sector Recommendations for February 2021

Source: Amherst Pierpont, Bloomberg/Barclays US Corp Index

Exhibit 2: APS Sector Recommendations for February 2021

Source: Amherst Pierpont, Bloomberg/Barclays US Corp Index

Spreads closed the month little changed in aggregate (Index OAS +1 bp), despite the fact that the market appeared to remain in a “risk-on” posture for credit. The IG Corporate Bond Index generated -0.06% excess return for the month, while total return was -1.28% with the sell-off in US Treasuries.

REITs (0.45% excess return) and finance companies (0.29%) generated the top credit returns in the Index amidst a flat month, as the appetite for low BBB credit persisted. Rounding out the top 5 sector performances for January were utilities (0.25%), natural gas (0.24%) and basic industry (0.22%), demonstrating a very mixed approach to credit risk. For the first time in several months, energy (0.01%) failed to land among the top sectors within the index, as the energy trade appeared to take breather; although much of that flat performance can be attributed to the reaction to S&P’s decision to put several of the energy majors on watch negative late in the month. Citing energy transition, price volatility and pressures on profitability, the rating agency placed nine oil and gas companies on review for downgrade, which it expects to resolve in the next several weeks, while also affirming the ratings and revising the outlooks on two companies to negative from stable (BP and Suncor). The five worst performances in January included communications (-0.38%), technology (-0.34%), banking (-0.21%), consumer cyclical (-0.08%) and capital goods (-0.05%), as investors appeared to continue to seek out higher-yielding opportunities even as aggregate spreads bumped along the bottom throughout the month.

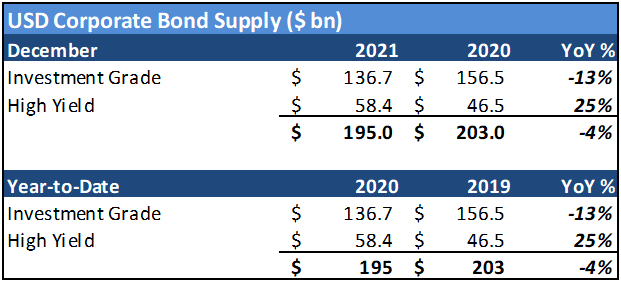

The IG new issue calendar handily beat expectations for the month, but failed to outpace January 2020. Total volume was $137 billion versus $157 billion in the prior year. Debt launches in the month were bolstered by a jumbo deal of $10 billion from 7-Eleven (SVELEV: Baa2/AA-*-) and a particularly active month from the bank/finance sectors – first by yankee issuance and later by the big US money center banks exiting their earnings blackout periods. Overall corporate debt placement year-over-year was flatter when taking into consideration the big gains over the prior year in High Yield and the EM, with HY new issue volume of $58 billion (+25%) and a record month for emerging markets.

Exhibit 3. Supply Recap – January IG volume fails to outpace 2020 despite a highly active month for bank/finance and the jumbo 7-Eleven launch

Source: Bloomberg LP

Exhibit 4. REITs and FinCos among the top performances in January

Source: Bloomberg Barclays US Corp Index

Exhibit 5. “Down-in-credit” strategies persisted despite spreads closing flat for the month

Source: Bloomberg Barclays US Corp Index

Exhibit 6. The 5-7 year bucket saw the best credit returns last month

Source: Bloomberg Barclays US Corp Index

Exhibit 7. Airlines, REITs, Hospitals and Natural Gas produced outsized gains in January

Source: Bloomberg Barclays US Corp Index

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.