The Big Idea

Playing the ends against the middle

Steven Abrahams | January 29, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

Most of the highest quality risk assets in fixed income have reached spread levels with limited room to tighten further. Large parts of agency MBS, agency CMBS and the highest quality corporate and structured credit markets fall in that category. Some investors appropriately are weighing whether risk-adjusted returns on these assets still top expectations for Treasury debt. Others are weighing riskier assets. A buyers’ strike is brewing in the middle, with marginal capital likely to flow to both Treasury debt and riskier assets.

The spreads

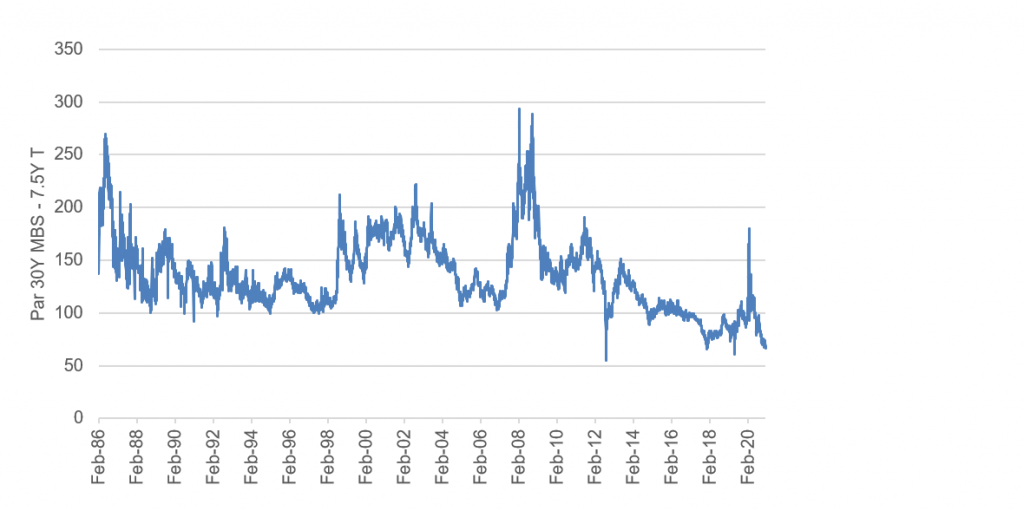

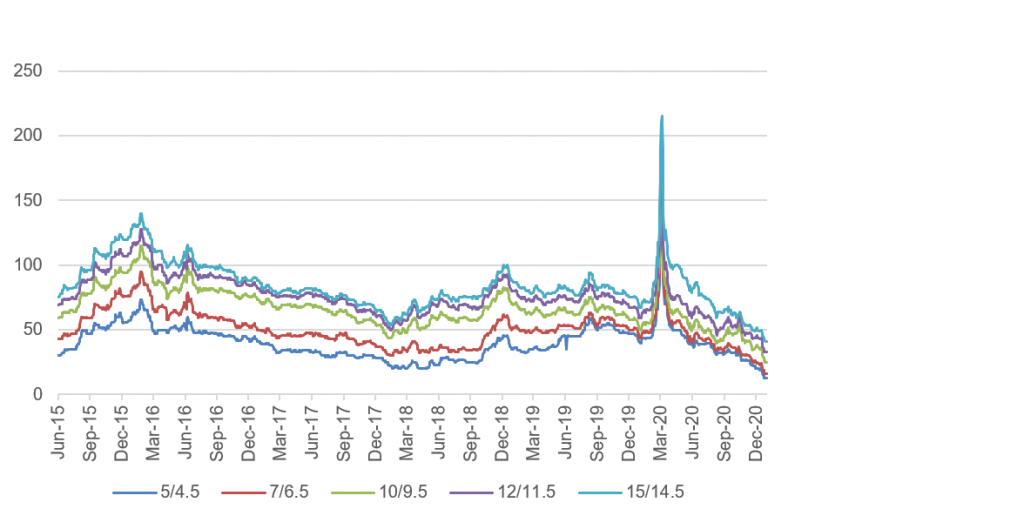

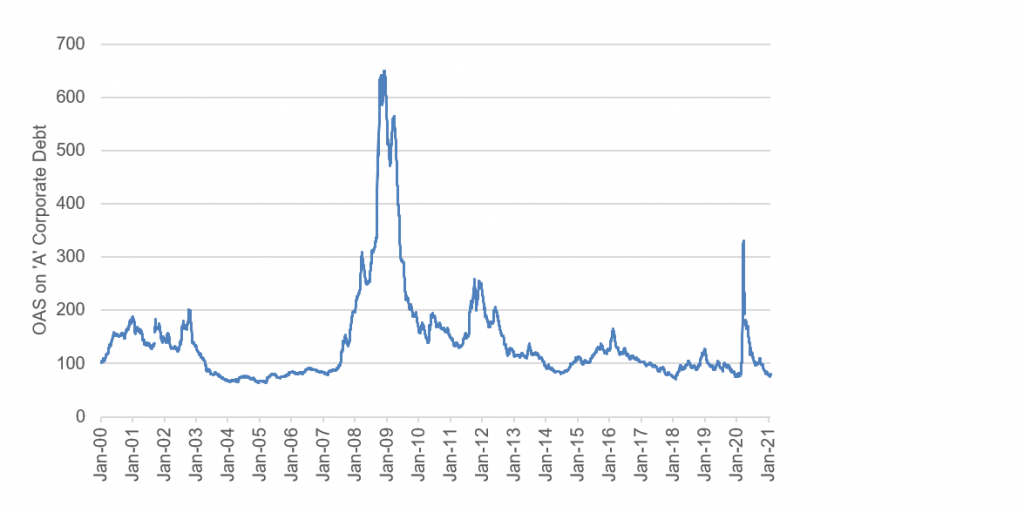

Almost every asset the Fed has targeted in QE now stands at or near historically tight levels. Nominal spreads to the Treasury curve on par 30-year agency MBS stand with basis points of the tightest levels in the market’s 35-year history (Exhibit 1A). Agency CMBS also shows spreads at the tightest levels in at least five years and anecdotally at the tightest levels since before the 2008 financial crisis (Exhibit 1B). Spreads on ‘‘A’ and other highly rated corporate debt have approached or exceeded the tightest levels in 20 years (Exhibit 1C).

Exhibit 1A: Par 30-year agency MBS spreads are near 35-year tights

Source: Bloomberg, Amherst Pierpont Securities

Exhibit 1B: Agency CMBS spreads have reached new tights

Source: Bloomberg, Amherst Pierpont Securities

Exhibit 1C: Spreads on ‘A’ corporate debt have reached 20-year tights

Source: ICE BofA AA Option-Adjusted Spread Index from FRB St Louis, Amherst Pierpont Securities

The drivers

Although QE since March has led to a nearly $400 billion net reduction in Treasury notes and bonds and has absorbed $718 billion in MBS—or more than 10% of the outstanding market—QE alone is not responsible for the broad tightening. QE undoubtedly has contributed by reducing the net supply of safer assets and forcing many portfolios into higher risks. But the federal government’s nearly $3 trillion in calendar 2020 fiscal stimulus has also put a safety net under many corporate and household balance sheets, consistent with tighter spreads. The announcement of Covid-19 vaccines in November, distribution problems notwithstanding, has also raises prospects of economic rebound consistent with tighter spreads. Spreads should be tight, arguably at historic levels.

Tight assets can get tighter, and there are powerful forces still pulling in that direction. Although the Fed has started a conversation about tapering its purchases, nothing looks imminent. The Fed should remain a force. Beyond the Fed, banks have proven a powerful bid for safer assets, too. Banks in the last year have added nearly $320 billion in Treasury balances and $500 billion in agency MBS balances. Because of regulations on liquidity and risk and the effect of assets on the capital required by annual stress testing, banks have limited ability to diversify outside of these safe assets. As QE and fiscal stimulus continue to flood bank balance sheets with cash, banks will need to keep buying.

The things that can go wrong

But the market in the highest quality assets leaves little room for error, and there is possible error out there in each factor driving spreads:

- The risk of taper. The market is tightly wound around QE both through the Fed’s direct purchases and the purchases made by banks. If the economy recovers as sharply as our Chief Economist Stephen Stanley expects, there is a strong case for Fed tapering in early 2022. And the Fed would need to send a signal in late 2021. Former New York Fed President Bill Dudley has recently argued that the Fed will trigger a new version of the 2013 taper tantrum, which featured a sharp widening in risk spreads.

- The risk of fiscal shortfall. The market looks priced for somewhere between $1 trillion and $1.25 trillion of the Biden administration’s $1.9 trillion stimulus proposal, but there is some risk of shortfall. If Biden decides to encourage a bipartisan bill, the numbers could come in below market pricing. This could also happen if centrist Democrats want to limit spending. Biden might also choose to split the bill into two pieces—one including the most popular parts of this program that he could pass with bipartisan support and a second that he could pass through reconciliation—and the second piece could get stranded if centrist Democrats object.

- Complications of pandemic. More vaccine supply and improved distribution looks likely to get the US to herd immunity by mid-2021 or late 2021 in the worst case. But mutations in the coronavirus could complicate the process. New variants of Covid-19 could keep public social distancing policies in place or continue to inhibit consumers’ willingness to engage in certain economic activity. Even though scientists have proven their ability to rapidly develop vaccines tailored to new viruses, steady evolution in the coronavirus could cap economic rebound below levels now priced into the market.

Any of these would likely fall heavily across most asset in fixed income, but the ones now trading at historically tight spreads offer limited compensation.

A quality barbell

For capital constrained to stay in safer investments, the thin spreads on some assets targeted by QE already argue for giving up the marginal yield for the liquidity of Treasury debt. At least a handful of banks already are looking at this. Liquidity, after all, is an option to get back into the market at better levels. For capital free to take higher risks, the yields in weaker or less liquid credits offer better compensation. The net effect should be to see marginal capital now flow into both the riskless and riskier assets—a credit and liquidity barbell. The ends play against the middle with good odds of winning.

* * *

The view in rates

Higher and steeper. The Treasury yield curve has finished its most recent session with 2s10s at 95 bp, flatter from last week by only 1 bp, and 5s30s at 141 bp, also only 1 bp flatter. Inflation expectations have remained relatively steady at 210 bp, not far from the high point for the last 12 months. Volatility should remain steady.

In financing markets, the heavy supply of cash is reducing repo rates. GC repo for Treasury debt and agency MBS has run below IOER for several weeks. Cash from banks is bringing repo that normally trades above IOER down to IOER. Cash from money market funds is left to chase other opportunities, and, as the supply of Treasury bills has dropped—a favorite money market fund investment—more cash has poured into repo. Repo rates have consequently dropped.

The view in spreads

Spreads should continue to tighten slightly despite being near or at historic tights in many assets. QE absorbs MBS, the relatively riskless spread asset, at least regarding credit. Fiscal stimulus, pandemic recovery and Fed policy should also keep spreads steadily tighter through 2021. Weaker credits should outperform stronger credits, with high yield topping investment grade debt and both topping safe assets such as agency MBS and Treasury debt. Consumer credit should outperform corporate credit.

The view in credit

Consumers in aggregate are coming out of 2020 with a $5 trillion gain in net worth. Aggregate savings are up, home values are up and investment portfolios are up. Consumers have not added much debt. Although there is an underlying distribution of haves and have nots, the aggregate consumer balance sheet is strong. Corporate balance sheets have taken on substantial amounts of debt and will need earnings to rebound for either debt-to-EBITDA or EBITDA-to-interest-expense to drop back to better levels. Credit in the next few months could see some volatility as Covid begins forcing shutdown of some economic activity and distribution of vaccines potentially hits some logistical potholes. But distribution and vaccine uptake through next year should put a floor on fundamental risk with businesses and households most affected by pandemic—personal services, restaurants, leisure and entertainment, travel and hotels—bouncing back the most.