The Big Idea

Managing the yield curve

This material is a Marketing Communication and does not constitute Independent Investment Research.

The Fed might look like it has done Treasury and the federal government a great favor by purchasing massive amounts of Treasury securities and helping finance the rise in the budget deficit required by the pandemic. But on closer examination, the Treasury’s borrowing and the Fed’s buying have been like the proverbial ships passing in the night. The Treasury has focused its borrowing in the bill sector while the Fed stopped buying bills after the pandemic began and bought an unprecedented amount of coupon securities across the yield curve. Treasury bill supply consequently exploded in 2020 while the outstanding float of Treasury coupon securities excluding Fed holdings actually dropped substantially.

Treasury debt issuance

The pandemic created urgent federal borrowing needs not seen since World War II. Not only did the budget deficit increase, but the government shoveled massive amounts of money out the door, with rebate checks and unemployment benefits authorized in the CARES Act quickly distributed beginning in April. The federal government also shelled out billions for health care, testing and vaccine research as well as funds forother relief programs like PPP. And Treasury delayed the April 15 deadline for individual and corporate income taxes to July 15.

The federal budget deficit went from running at an already-hefty $1 trillion annual pace before the pandemic to an eye-popping $2 trillion in the second quarter of 2020 alone. Coupled with Treasury debt managers’ desire to beef up the cash balance to cover the possibility of a further unexpected bulge in expenses, federal borrowing in the spring of 2020 topped $2.7 trillion.

Due in part to its longstanding policy of fostering regular and predictable issuance as well as the realities of the market, Treasury debt managers were not in a position to raise massive amounts of new money from its coupon offerings in a matter of weeks. Out of necessity, they turned to the bill sector. In particular, debt managers issued close to $2 trillion in cash management bills in a matter of a few months.

At that time, Treasury debt managers also began raising the monthly coupon auction sizes by unprecedently large increments. These hikes are an effort over time to “term out” the issuance, but it takes a while for the monthly increases to compound and add up to a meaningful amount in the context of $3 trillion annual budget deficits.

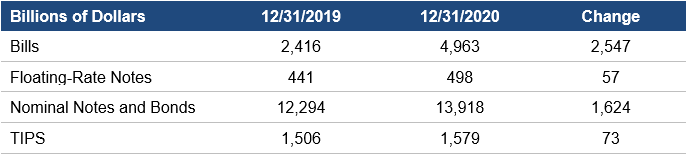

Both Treasury bill and coupon issuance rose sharply through 2020, but bills accounted for a larger proportion of the increase and rose by much more in percentage terms (Exhibit 1).

Exhibit 1: Outstanding Treasury debt held by the public, including Fed holdings

Source: Treasury Dept.

Federal Reserve Holdings

Prior to the pandemic, the Federal Reserve had two programs going simultaneously to buy Treasury securities. First, the Fed was rolling over its MBS runoff into Treasuries, which required a modest amount of purchases each month, spread evenly across the yield curve from bills all the way to bonds. Second, after seeing the shrinkage in its balance sheet through the summer of 2019 create a scarcity of reserves and dislocations in the repo market, the Fed began to buy T-bills to increase the level of reserves in the financial system. Pre-pandemic, the Fed was actually increasing its bill holdings by more than it was building its coupon position.

When the pandemic led to severe financial market upheaval, two key developments in March altered the Fed’s approach. First, the Fed stopped buying bills because of a flight to quality and liquidity, which lead to an immense increase in the market demand for bills. The Fed did not want to create or exacerbate a shortage of bills. Second, a sharp reduction in liquidity for off-the-run Treasuries created wild swings in coupon prices, and the Fed responded by becoming the buyer of last resort, embarking on a massive buying campaign of off-the-run Treasury coupons split evenly across the yield curve according to the outstanding debt in each sector.

As financial markets returned to normal, the Fed gradually reduced the pace of its coupon purchases but continued to buy at a substantial pace, eventually shifting the stated rationale of the program away from market functioning and toward monetary policy accommodation. By year-end, the Fed was buying $80 billion in Treasury coupons a month and was still maintaining steady bill holdings.

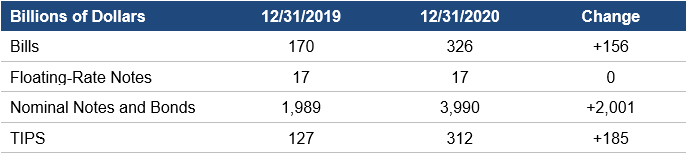

The Fed through 2020 bought roughly $2 trillion in nominal coupons and a substantial amount of TIPS but barely increased bills holdings for the year, and not at all after March (Exhibit 2).

Exhibit 2: Fed SOMA Treasury debt holdings

Source: Treasury Dept.

Net supply: combining the two

Combining Treasury issuance and Fed holdings, the 2020 increase in outstanding supply of Treasury bills was massive. Even accounting for the Fed’s SOMA account, outstanding supply more than doubled, rising by nearly $2.5 trillion, and the Fed only absorbed a small portion of that.

In contrast, net of the Fed, outstanding Treasury coupon supply actually declined in 2020 by almost $400 billion, while outstanding TIPS float sank by over $100 billion, or almost 10%.

Whether it was intended or not, the impact of the separate decisions by Treasury and the Fed have created massive swings in the relative supply of short paper versus longer-term paper and presumably has had an impact on the shape of the yield curve.

Although radical changes in the behavior of either the Treasury or the Fed look unlikely in the near term, once the pandemic is over, presumably Treasury borrowing needs will diminish, which will lead to an unwinding in a good portion of the spike in bill issuance, while the FOMC will eventually begin to taper the pace of its coupon purchases, unwinding in both cases the trends established in 2020, though the pace on the way out will likely be far more gradual than the abrupt changes seen in the spring of 2020.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.