The Big Idea

Hedging taper risk

Steven Abrahams | January 15, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

If Fed speeches and interviews are a continuation of policy debate by other means, then the topic of tapering asset purchases has heated up in the last month. The Fed has tied the course of QE to “substantial further progress” on inflation and unemployment, but the Fed may have less control over the timing than it did after the 2008 crisis. Since so many investors own assets with valuations shaped by QE, hedging taper risk may be one of the big decisions of this year.

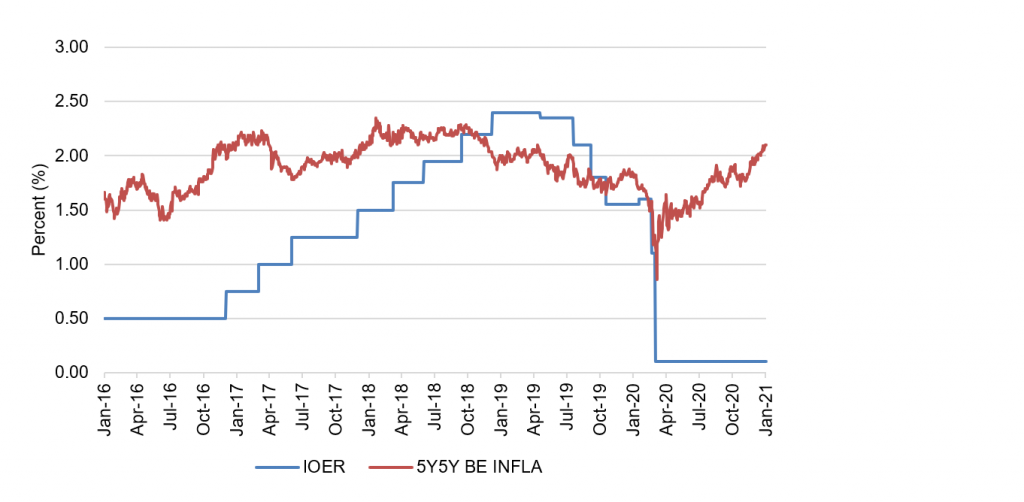

Inflation expectations have already breached 2%

A key Fed goal since its policy shift at Jackson Hole last year is to get average inflation to 2% over time and keep inflation expectations around 2%. Low Fed policy rates, QE and other Fed programs and actual and expected fiscal stimulus have lifted expected inflation sharply since last March. One of the Fed’s preferred measures, implied 5-year forward 5-year inflation, has moved above 2% since mid-December (Exhibit 1). The Fed historically has tended to tighten when this measure has moved above 2% and eased below 2%. The Fed after Jackson Hole may choose to let expectations run a little hot for a little longer than it might have in the past. The game of higher expectations is not over, but it is far along.

Exhibit 1: Inflation expectations have hits marks linked to past Fed tightening

Source: Bloomberg, Amherst Pierpont Securities

The Fed faces different challenges and active fiscal stimulus

Whether inflation will actually show up is another question. Inflation below 2% persisted despite rounds of QE running from 2008 through 2014. But current circumstances differ mainly because of the nature of the economic crisis and the role of fiscal policy. The 2008 crisis came out of the banking system, ultimately reducing its risk appetite and its ability to transmit Fed policy to the broader economy. The current crisis came from a pandemic shock to the economy, while the financial system is well capitalized and liquid. The high point of 2008 fiscal response was a $700 billion effort to support banks. Last year’s CARES Act added more than $2 trillion to the economy, recent legislation will add another $900 billion and the Biden administration is seeking $1.9 trillion more. Vaccination and fiscal stimulus take a large measure of control out of Fed hands. A rebound from pandemic could come with a surge in demand for clothing, travel, leisure, entertainment and other services with limited capacity to expand supply, a recipe for inflation that the Fed would need to address.

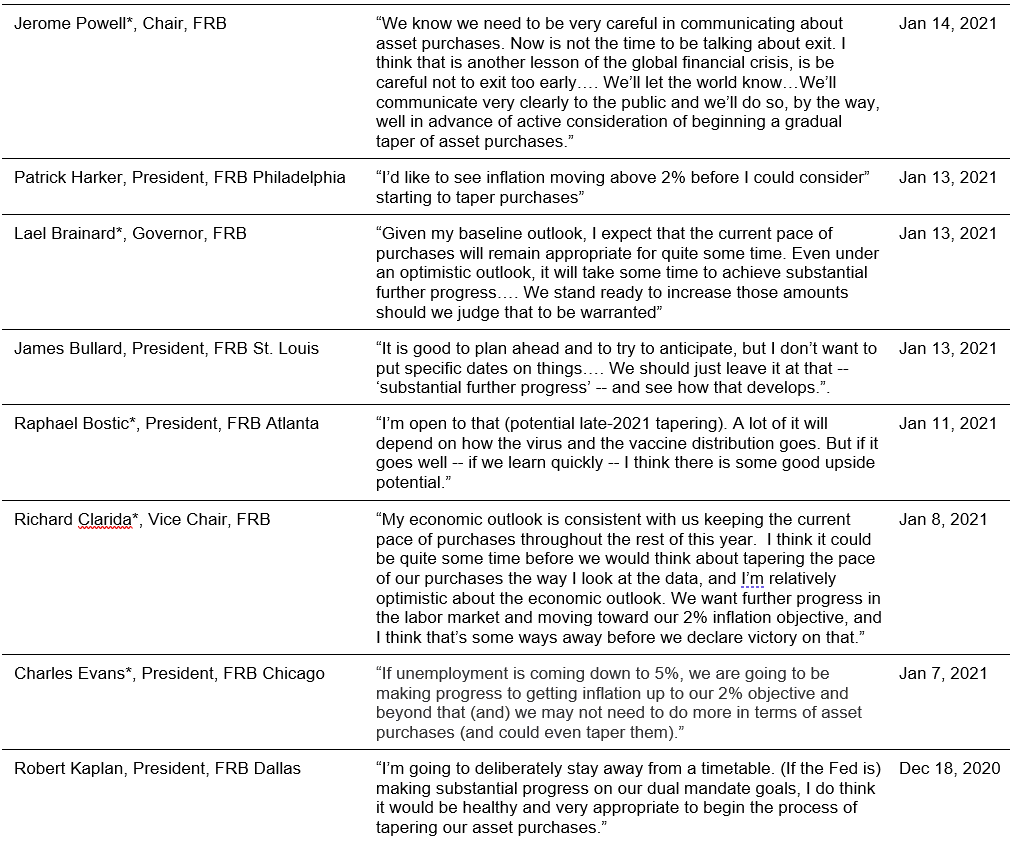

A Fed debate

Eight Fed governors or bank presidents have weighed in since mid-December on the topic of tapering, including five of the 11 members of the FOMC eligible to vote in 2021 (Exhibit 2). All have avoided timelines and largely focused on linking tapering to progress on inflation and employment. Powell has talked down the possibility of tapering, and the market has reversed some of its move to higher rates. But the broad public remarks are a clear sign of active discussion at the board and among the banks and system staff likely about what “substantial further progress” will mean in practice.

Exhibit 2: Recent Fed remarks on tapering signal active debate

Note: *Voting member of the FOMC in 2021.

Source: MNI, Reuters, Bloomberg, Amherst Pierpont Securities

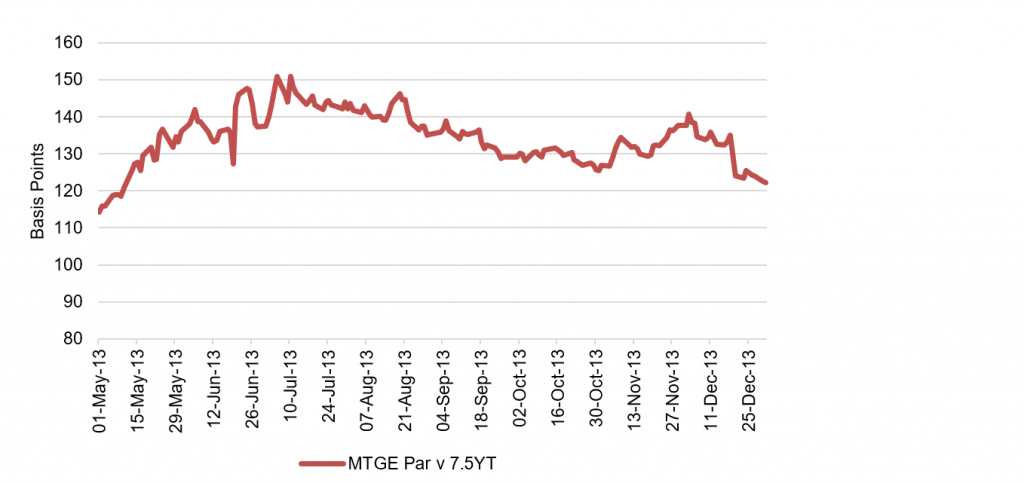

The impact of the first sign of tapering

When then-Fed Chair Ben Bernanke first indicated on May 22, 2013, that the Fed might pull back on QE, the impact came in both higher rates and wider spreads. Higher rates arguably reflected market belief that the Fed saw stronger growth than the market had expected. Wider spreads reflected concerns that a pull back in QE would reduce demand for risk. In any event, the impact was swift and significant. Within a month, US 10-year rates moved from 1.93% to 2.53% (Exhibit 3A). Nominal spreads on par 30-year agency MBS from 128 bp to 146 bp (Exhibit 3B). And implied volatility in 3-month options on 10-year swaps moved from 34% to 39%.

Exhibit 3A: The 2013 taper tantrum sent rates up quickly…

Exhibit 3B: And sent risk spreads wider

Source: Bloomberg, Amherst Pierpont Securities

Hedging the risk

Even if the Fed waits until 2022 to taper, the signaling will probably start this year. Liquidity across most parts of fixed income will likely drop, making it relatively expensive to sell and reduce exposure. Hedging now, well in advance of tapering, seems a better approach. The menu of possibilities includes a list of positions that could counter higher rates, wider spreads and higher volatility:

• Paying fixed on swaps or using Treasury futures to lower duration

• Shorting IG or HY CDX or possibly CMBX to monetize wider spreads

• Rolling a position in short-dated pay-fixed swaptions to gain from higher rates and higher volatility

• Rolling a position in calls on the VIX to capture higher volatility, or using call spreads to limit costs

• Rolling a position in puts on the S&P 500 or using put spreads to limit costs

Relatively low rates, tight spreads and low volatility make many of these hedges inexpensive, although giving up income in this market also is hard.

The risk of tapering does not change the greater likelihood that remaining QE, fiscal stimulus and pandemic rebound will push up longer rates and tighten spreads this year. Portfolios need to stay invested especially in the lower rated corporate and structured credits most likely to perform well. But the conversation about tapering has clearly started at the Fed and will likely end at some point this year with an announcement. Get ready for it now.

* * *

The view in rates

The incoming White House will ask Congress for $1.9 trillion in fiscal spending, and the story of rates for the next 100 days will likely play out on a political field. The market for now probably prices in another $1,400 in payments to eligible taxpayers, some extension of unemployment benefits, some funds to state and local governments and some infrastructure spending. That probably comes to an expected $1 trillion to $1.25 trillion. As expectations go above or below that range, rates should move accordingly. The Treasury yield curve has finished its most recent session with 2s10s at 95 bp and 5s30s at 138 bp, not far from the high marks over the last 12 months. The steepening largely reflects rising inflation expectations. The spread between 10-year notes and TIPS shows inflation expectations at 210 bp, the high point for the year, with real yields showing significant weakness and hovering at -102 bp. Implied interest rate volatility remains relatively low but has slowly trended higher since initially dropping after the early November US elections.

The view in spreads

Spreads should continue to tighten further despite being near or at historic tights. Tremendous net Treasury supply is creating a surplus of the riskless benchmark while QE absorbs MBS, the relatively riskless spread asset, at least regarding credit. Beyond the influence of net Treasury supply, fiscal stimulus, pandemic recovery and Fed policy should also keep spreads steadily tighter through 2021. Weaker credits should outperform stronger credits, with high yield topping investment grade debt and both topping safe assets such as agency MBS and Treasury debt. Consumer credit should outperform corporate credit.

The view in credit

Consumers in aggregate are coming out of 2020 with a $5 trillion gain in net worth. Aggregate savings are up, home values are up and investment portfolios are up. Consumers have not added much debt. Although there is an underlying distribution of haves and have nots, the aggregate consumer balance sheet is strong. Corporate balance sheets have taken on substantial amounts of debt and will need earnings to rebound for either debt-to-EBITDA or EBITDA-to-interest-expense to drop back to better levels. Credit in the next few months could see some volatility as Covid begins forcing shutdown of some economic activity and distribution of vaccines potentially hits some logistical potholes. But distribution and vaccine uptake through next year should put a floor on fundamental risk with businesses and households most affected by pandemic—personal services, restaurants, leisure and entertainment, travel and hotels—bouncing back the most.