Uncategorized

Dodging default risk in Ginnie Mae project loans

admin | December 4, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Trends in delinquency rates in Ginnie Mae project loans during the pandemic have been similar to those seen in the aftermath of the 2008 financial crisis, though total delinquencies so far remain well below prior peaks. There are some pockets of risk: deals vulnerable to prepayment triggered by high levels of delinquencies or by delinquencies concentrated in construction loans. Senior housing also poses some risk.

Delinquency rates across all Ginnie Mae project loans are currently 1.48% (Exhibit 1). That is the percentage of delinquent unpaid principal balance (UPB), not the percentage of delinquent loans, though the two are very close. Over half of those delinquencies are in the 90+ day bucket. Ginnie Mae does not publicly disclose loans in forbearance but does mark loans in forbearance as delinquent. The vast majority of loans in the 90+ day delinquency bucket presumably have been in forbearance for between three and six months.

Exhibit 1: Historical Ginnie Mae project loan delinquency rates

Source: Ginnie Mae, Amherst Pierpont Securities

Repayment periods have started for most loans in forbearance, and as the loans gradually cure, many of the 90+ day delinquent loans will move to the 60-day and then the 30-day delinquent bucket and then eventually back into performing status. Others will transition into default. Although construction loans only comprise about 21% of outstanding project loans, they historically have tended to become delinquent and default at two times to three times the rate of other project loans. During the pandemic this trend is remaining intact, as construction loans have a delinquency rate of 2.75%, about 2.5 times the 1.10% delinquency rate of standard project loans (Exhibit 2), and currently account for 39% of all delinquent loans.

Exhibit 2: Ginnie Mae project loan delinquency rates

Note: Delinquency data as of November 2020. This includes all currently outstanding Ginnie Mae project loans, approximately $10 billion of which are not in REMICS. Prefix definitions are in the Appendix.

Source: Ginnie Mae, Amherst Pierpont Securities

Several of the project loan types are not currently in outstanding GNR REMICs, including CS, LS, RX and PL types. However, the overall delinquency rates by loan type in REMICS are similar. Investors looking to avoid concentration risk of involuntary prepayments should monitor the deals with notably high levels of overall delinquencies and delinquencies concentrated in construction loans (Exhibit 3).

Exhibit 3: Deals with concentrated default risk

Note: Data as of 12-3-2020. Source: Bloomberg, Amherst Pierpont Securities

Seniors housing remains a trouble spot

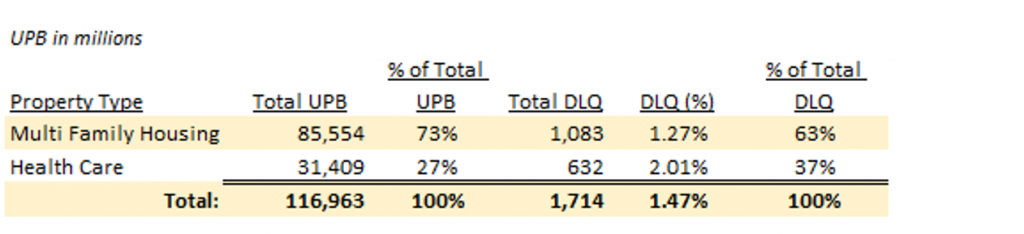

Senior housing facilities continue to have elevated delinquency rates: 2.0% of loan balances of health care facilities are in some stage of delinquency compared to 1.27% of multifamily properties (Exhibit 4). The health care facilities represent 37% of delinquent loan balances and 27% of GNR multifamily REMIC balances outstanding.

Exhibit 4: GNR multifamily REMIC delinquency rates by property type

Note: GNR multifamily REMIC loan balances total $121.5 billion as of 12/3/2020. Approximately $5 billion of that total does not list a property type. Data as of 11/16/2020 tape date.

Source: Bloomberg, Amherst Pierpont Securities

Investors looking to avoid concentrated default risk should also get proper compensation for deals overweight health care properties.

Appendix: Prefix codes for Ginnie Mae Project Loans

Note: There is no listed prefix code of RX that could be found in the documentation but it does appear in Ginnie Mae’s project loan database.

Source: Ginnie Mae

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.