Uncategorized

Prepayments peak, servicers consolidate in 2021

admin | November 20, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Just as 2020 delivered prepayment surprises that hurt MBS investors, 2021 looks likely to offer kinder treatment. MBS prepayment speeds peaked this year at levels last seen before the 2008 financial crisis. But the peak is or soon should be passed, and some of the most negatively convex MBS should get the biggest lift. Servicers also should consolidate, raising risk in pools serviced by smaller non-banks and adding value to pools serviced by banks. As for other regulatory change with impact on valuation, very little looks likely to unfold.

Prepayment speeds have likely peaked, so go up-in-coupon

Even if Treasury rates and MBS spreads stand still next year, the mortgage rates available to borrowers look likely to plateau and allow the start of prepayment burnout. Higher rates could help, of course, but a bottom in primary rates alone sets the stage. With the MBS market priced to the fast speeds of 2020, a slower pace should lift returns in premium pass-throughs and MBS derivatives.

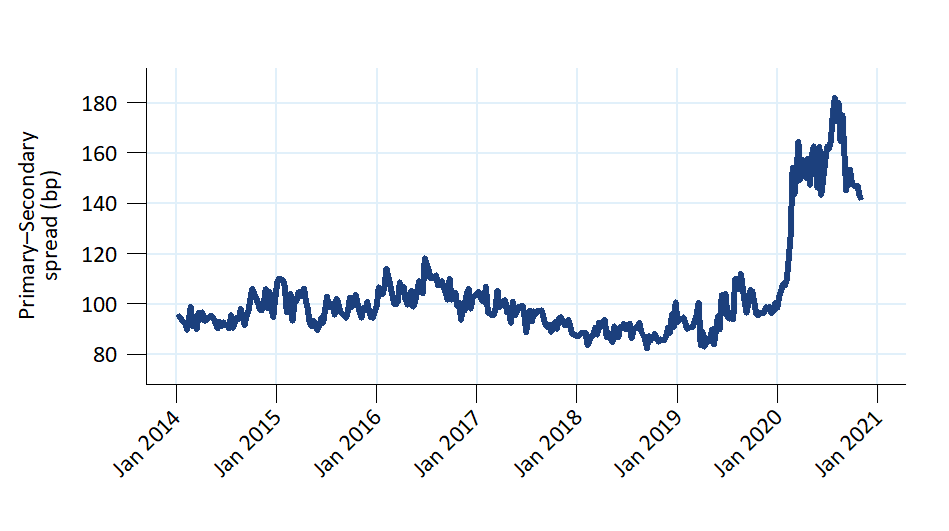

Relatively fixed origination capacity kept mortgage rates from falling as much as other rates markets early in the pandemic, causing the spread between the primary mortgage rate offered to a borrower and the secondary mortgage rate demanded by investors to widen significantly (Exhibit 1). The primary-secondary spread is often estimated using a survey, like Freddie Mac’s Primary Mortgage Market Survey rate (PMMS), and comparing it to the rate for a par-priced MBS, or the mortgage current coupon. That spread jumped as high as 182 bp in August 2020 before falling to 141 bp as of mid-November, which is about 45 bp above the average from 2017 through 2019.

Exhibit 1: Primary/secondary spreads widened during the pandemic

Source: Yield Book, Amherst Pierpont Securities.

The primary-secondary spread is not likely to fall much further. Starting December 1, both Fannie Mae and Freddie Mac will charge a 50 bp upfront refinance fee. Originators will likely pass this along to borrowers, which should raise the minimum primary-secondary spread by roughly 10 bp to 15 bp. This implies that primary-secondary spreads could only decline by at most 30 bp to 35 bp before normalizing. But wait, there’s more.

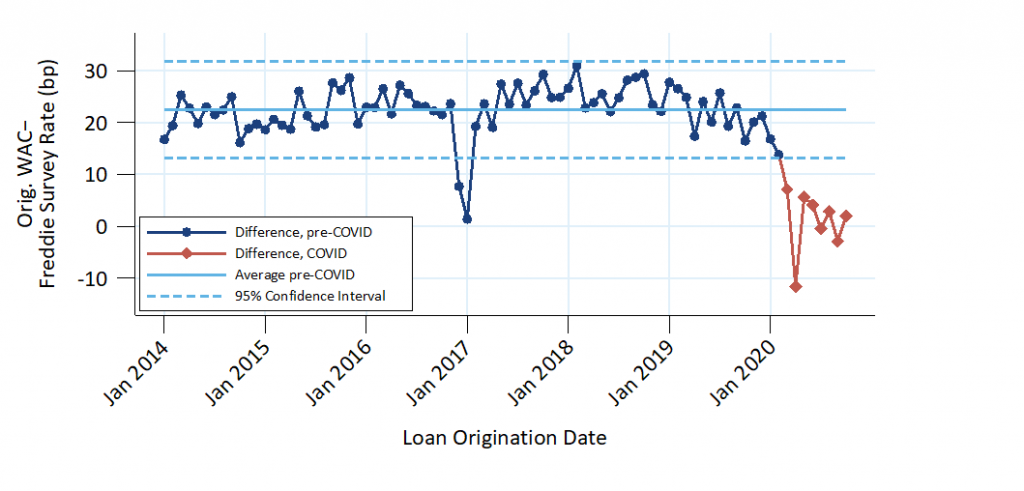

It turns out that much of the remaining spread is a mirage, since the PMMS rate has been artificially high throughout the pandemic by roughly 20 bp to 25 bp (Exhibit 2). This is seen by comparing the survey rate to the average rate on new originations each month. Since 2014, the survey rate has been 20 bp to 25 bp lower than the average rate received by a borrower, but since the pandemic this difference has fallen to nearly 0 bp. In other words, the origination rate currently is only around 10 bp to 15 bp wider than minimum. The primary-secondary spread has been tightening by roughly 10 bp a month since August; if that pace continues, then all the excess could vanish by the end of the year.

Exhibit 2: Primary rate surveys overstate the primary/secondary spread

Source: Fannie Mae, Freddie Mac, Yield Book, Amherst Pierpont Securities.

This means that, unless rates drop even lower, the primary rate will shortly plateau, and MBS prepayment speeds are very close to the peak. Primary mortgage rates would increase if interest rates shift higher since the primary-secondary spread does not have much room to tighten. My colleague, Steven Abrahams, makes the case that interest rates next year are likely to move even higher than predicted by the forward curve, and prepayment speeds would fall as a result.

A bend toward slower speeds would likely benefit the more negatively convex premium pass-throughs now getting hit hardest by prepayments, including TBA FNCL 3.0% and higher coupons. Jumbo pass-throughs should get a lift, too. MBS derivatives backed by negatively convex pools also should perform well. Weaker performers would include specified pools that offer prepayment protection just as speeds fade.

Contraction and consolidation raise risk in non-bank servicers

MBS servicers already have an important impact on valuation, but servicer looks likely to matter even more next year. Originators, who usually also service the loans, will have to grapple with less business as refinancing volumes likely slow in 2021. The first step will be job cuts, reversing the job growth over the last few months. But a significant drop in origination volume could drive consolidation as smaller and less efficient originators are no longer able to compete effectively. Many will be acquired or go out of business. Similar consolidation occurred after the 2008 financial crisis, when a large share of mortgage origination was done by a handful of large banks. Subsequent regulatory changes opened the window for the growth of non-bank originators and reduced the role of the banks. This time it is likely that the origination business will concentrate at the large non-bank originators.

Consolidation and transition of servicing to a new platform often adds volatility to prepayments, particularly if the acquirer tends to buyout or refinance loans aggressively. Holding pools serviced by banks avoids this risk. Alternatively, holding pools serviced by the larger non-bank servicers mitigates this risk since the larger non-bank names are likely to be the acquirer and not the acquiree.

Covid-19 changes create more negative convexity in the long run

Although this may not play out materially in 2021, more efficient originations stand to add negative convexity to MBS in the long run. This should slowly accrue to the benefit of specified pools.

One consequence of the Covid-19 pandemic is that Fannie Mae and Freddie Mac permitted more appraisals without requiring an interior inspection. This may have a lasting effect on the origination of purchase loans, which lenders can appraise without an on-site inspection using the so-called “desktop appraisal.” If loans originated with desktop appraisals have similar credit performance as loans with full appraisals, it could prove difficult for the GSEs to roll back this change. That means originating purchase loans could be somewhat easier than before, adding a little boost to turnover-driven prepayment speeds. This could keep lower coupon MBS prepaying a little faster than before. It could also prove difficult to roll back appraisal flexibilities from refinance transactions—although desktop appraisals are not currently permitted, the use of appraisal waivers has grown rapidly, and originators can opt to use an exterior-only appraisal. This means that MBS are likely to prepay quickly in any future refinance environment.

Few other regulatory risks to MBS

The Covid-19 pandemic makes it less likely that the incoming administration would immediately lower FHA mortgage insurance premiums (MIPs). Lower MIPs would cause FHA loans to prepay faster, hurting the value of Ginnie Mae MBS. However, the FHA could pay as much as $11 billion dollars to satisfy partial claims on the current delinquent FHA loans, and that number will be even higher since some loans will proceed to foreclosure. That would use roughly 16% of the FHA’s capital reserves. Until the pandemic is clearly under control, it seems more likely that the FHA would leave premiums at their current levels. It is also worth remembering that the insurance fund had similar capital reserves prior to the 2008 financial crisis yet ultimately needed a cash infusion, which implies that lower premiums are insufficient to protect against extreme economic shocks. Keeping premiums at 85 bp instead of lowering to 55 bp at the start of 2017 likely added roughly $4 billion to the insurance fund.

Similarly, it seems unlikely that the GSEs will make dramatic changes to how they price mortgages. Affordable housing goals may be more important to the incoming administration than the outgoing administration, but that does not necessarily indicate there will be large changes that could affect prepayments even if the administration is able to replace current Federal Housing Finance Agency Director Mark Calabria early. The five years under Mel Watt did not bring major changes to pricing compared to his more conservative predecessor. It does reduce the likelihood that the GSEs will be recapitalized and released from government conservatorship, but the smooth functioning of the MBS market is extremely important and unlikely to be disrupted.

The qualified mortgage “patch” that allows the GSEs to guarantee high-DTI loans is set to expire in January 2021. However, it is highly unlikely that the government will let this happen since it would leave many borrowers without easy access to mortgage credit. The patch will be extended or replaced with a rule that permits the GSEs to continue guaranteeing most of those loans.