Uncategorized

High yield returns available in 2013 vintage aircraft EETCs

admin | November 13, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Non-US 2013 vintage aircraft EETCs are currently offering high 5% range yields as they approach the final years in their respective sinking fund maturity structures. Two highlights are British Airways (IAGLN) and Air Canada (ACACN) 2013-1 Class A certificates. While aircraft secondary values, particularly widebody, have taken a considerable hit with the drop-off in air travel due to global Covid concerns, these bonds still remain well over-collateralized and benefit from liquidity facilities covering 18 months of interest payments. The recent vaccine developments and prospects for an accelerated recovery in air travel have caused a pop in pricing, but the pass-thru certificates still offer excellent value given the underlying strength of the airlines and their relative systemic importance to air travel in their respective countries.

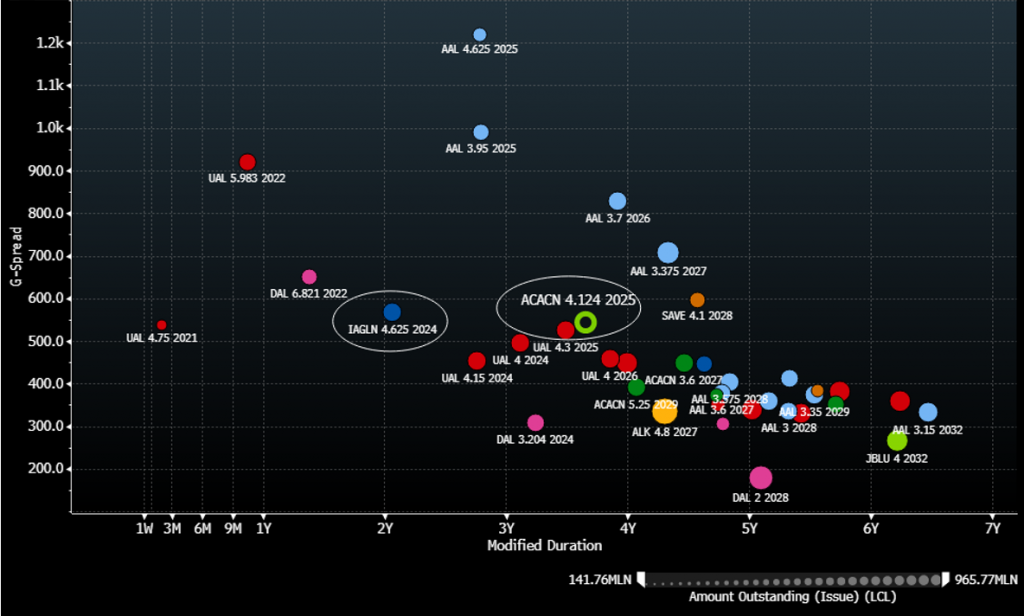

Graph 1. IAGLN 2013-1 and ACACN 2013-1 vs IG first lien EETCs

Source: Amherst Pierpont Securities, Bloomberg/TRACE – G-spread Indications Only

Recommendation

IAGLN 4.625% 6/20/24 @ $97.5; G+569; 5.87%

Issuer: British Airways 2013-1 Class A Pass Through Trust

CUSIP: 11042AAA2

First Lien, Sinking Fund, 144A

Amount outstanding: $472.6 million

Amount issued: $721.6mm

Rating: Baa2/A/A+

- This structure is a first lien enhanced equipment trust (EETC). They are designed as pass through trusts, which are tax efficient and bankruptcy remote to help facilitate the passing of collateral in event of default. The enhanced feature of an ETC means that it is separated into multiple classes. In this case, the Class B pass through certificates already matured earlier this year. The 2013-1 deal was a first for British Airways when issued in 2013, and the structure has since been replicated twice in 2018 and 2019. The rated pass through certificates are issued by the two pass through trusts. The assets in the trust consist of equipment notes, issued by a special purpose entity. The proceeds of the notes were used to purchase mortgage bonds for the purchase of the aircraft, the payments of which are funded with the lease payments from British Airways (BA) for the term of the transaction. The structure was formed under the protocols of the “Cape Town Convention.”

- The Class A certificates include an 18-month liquidity facility provided by Landesbank Hessen-Thuuringen (Aa3/A/AA-), which provides 6 quarterly interest payments or 18 months of debt service.

- The Class A certificates were extremely over-collateralized at inception with an initial loan-to-value (LTV) ratio of 55% (according to the prospectus). Max LTV was expected to be 68% given the amortization schedule. While we do not have current appraisal on the aircraft, the rating agencies provide updates to keep investors informed, in some cases annually, as is the case with Fitch. In their most recent update (2019), Fitch applied a stress level haircut of 25% on the aircraft and calculated a max LTV of 78%.

- The collateral consists of 14 tier 1 aircraft, all purchased new for delivery in 2013 and 2014. The bulk of the value is held in the 6 Boeing 787-8s – known more commonly as the Dreamliner series. These are long-haul, widebody, twin engine aircraft that became the standard bearer for the industry upon their introduction several years earlier. In 2013, each aircraft had a new appraised value of around $120 million apiece. Also included are two Boeing 777-300ER or extended range aircraft. The 777s are also widebody and the largest class of twin jets that Boeing produces. These were launched as replacement for older, 747s, 767s and DC10 models for extended range flight. They are attractive because they are cheaper to operate than the competing Airbus A380s. These 2 aircraft were each valued at about $167mm at delivery. Lastly, are the 6 Airbus A320-200s. These are shorter-range, narrowbody aircraft, and still among the most popular variants on the A320 model. The secondary market for narrowbody aircraft remains much more viable, particularly in the challenging operating environment. These 6 aircraft were delivered at a price of roughly $43 million apiece.

- BA (Ba2/BB/BB) is a core component of the larger parent International Consolidated Airlines Group (IAG: B1/BB), and would therefore likely benefit from downstreaming of cash flows in a stressed event for the UK air carrier. BA is also viewed as being systemic to the UK airline industry with a large percentage of total traffic, and would therefore appear more likely to undergo a restructuring than a liquidation in the event of default.

- Moody’s recently downgrade BA to Ba2 to Baa1 on 9/07/20, resulting in a downgrade of the 2013-1 pass through certificates to Baa2 from Baa1. The ratings on the pass-thru certificates by S&P and Fitch were unaffected by the recent moves to BB from BBB- in May of 2020 by S&P and move to BB from BB+ last month by Fitch.

Recommendation

ACACN 4.125% 5/15/25 @ $94.5; G+545; 5.75%

Issuer: Air Canada 2013-1 Class A Pass Through Trust

CUSIP: 009089AA1

First Lien, Sinking Fund, 144A

Amount outstanding: $292.8 million

Amount issued: $424.4 million

Rating: Baa3/BBB-/A-

- This structure is also a first lien enhanced equipment trust (EETC). They are designed as pass through trusts, which are tax efficient and bankruptcy remote to help facilitate the passing of collateral in event of default. The enhanced feature of an ETC means that it is separated into multiple classes. In this case, the Class A remain senior to the Class B pass through certificates, which mature in the first half of next year, while the C class was fully retired in 2018. The assets in the trust consist of equipment notes, issued by a special purpose entity. The proceeds of the notes were used to purchase mortgage bonds for the purchase of the aircraft, the payments of which are funded with the lease payments from Air Canada (ACACN) for the term of the transaction. The structure was formed under the protocols of the “Cape Town Convention.”

- The Class A certificates include an 18-month liquidity facility provided by Natixis SA (A1/A+), which provides 3 semi-annual payments or 18 months of debt service.

- The Class A certificates were extremely over-collateralized at inception with an initial loan-to-value (LTV) ratio of less than 49% (according to the prospectus). While we do not have current appraisal on the aircraft, the rating agencies provide updates to keep investors informed, in some cases annually. In their most recent rating action downgrading the 2013-1 Class A certificates from A to A- in July of this year, Fitch assigned a max LTV in the mid-80% range for the collateral.

- The collateral consists of 5 tier 1 aircraft, all purchased new for delivery in 2013 and 2014. All five aircraft are Boeing 777-300ER or extended range aircraft. The 777s are widebody, long-range jets and the largest class of twin jets that Boeing produces. These were launched as replacement for older, 747s, 767s and DC10 models for extended range flight. They are considered attractive because they are cheaper to operate than the competing Airbus A380s. These aircraft were each valued at about $173mm at delivery.

- Air Canada is the country’s largest domestic, US transborder and international airline, and among the five operators in North America. As of year-end, ACACN operated a fleet of 188 aircraft, plus an additional 64 through Air Canada Rouge, and 151 via capacity purchase agreements operating under Air Canada Express through regional partners.

We believe the rating agencies have been very proactive and conservative in their rating actions on this particular structure. S&P recently downgraded ACACN parent to B+ from BB- on 8/24/20 and assigned a Negative Outlook. The 2013-1 pass through certificates were downgraded to BBB+ at that time, and then taken two more notches to BBB- last month, with S&P citing the longer-term deterioration on international travel. Fitch lowered their ratings on the pass through certificates to A- from A in July, following a downgrade of Air Canada to BB- from BB in the prior month. Moody’s lowered the rating on the 2013-1As to Baa2 from A3 in early May and then later took them down another notch that same month when they lowered the ACACN parent rating to Ba2 from Ba1.