Uncategorized

Outperforming Aircastle bonds still have room to run

admin | October 30, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

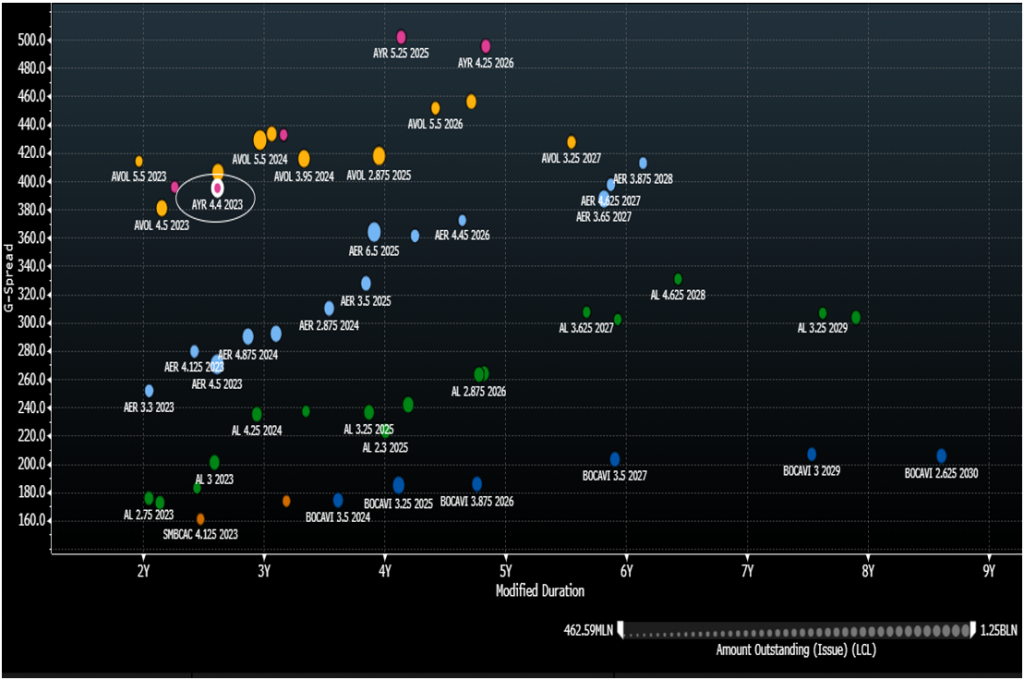

Investors comfortable playing in the riskier aircraft leasing credits in the front-end of the curve should consider Aircastle Ltd (AYR). AYR appears to have an adequate liquidity profile to meet near-term debt obligations, and the company was one of the top performing credits in the entire investment grade index throughout much of the latter part of the credit recovery over the summer months. Since the end of May, AYR has been a top 5 performing credit with a cumulative excess return of nearly 19%, and the single best performer on a spread basis, tightening by over 600 bp. The AYR 4.4% ‘23s tightened by over 700 bp during that time frame and still yield nearly 4.00%.

Recommendation: AYR 4.40% 9/25/23 @ +375 bp to 3-year; G+376 bp; 3.93%; $101.24

Similar issues: AYR 5½ 2/22 310-290 to the 2-year

Issuer: Aircastle Ltd (AYR)

CUSIP: 00928QAR2

Amount outstanding: $650 million

Rating: Baa3/BBB-/BBB

Global Issue

Exhibit 1: AYR vs IG Aircraft Lessor comps

Source: Bloomberg/TRACE Indications, Amherst Pierpont Securities

- AYR is unique among peers in that they strictly acquire mid-life aircraft, as opposed to financing new or newer equipment. They are focused on older aircraft and a customer base of more “upstart” global airlines. Average age of their aircraft portfolio is about 9 years, which compares with an industry leading level of about 4 at Air Lease and low 6s at names like AER. The company has been modernizing its fleet in recent quarters, bringing the average age down from about 9.5 a year ago. While this still places AYR among the riskier names in the Aircraft Leasing peer group, the upside of this characteristic is that the company has absolutely no exposure to the Boeing 737 Max.

- AYR has $7.2 billion in equipment held for lease with no existing order book. As of the most recent quarter, the fleet consists of 283 aircraft, the large majority of which are unencumbered. 90% of the aircraft are currently classified as narrowbody. AYR services 80 separate airline customers in 44 nations. Some of their larger lessees include IndiGo, Latam, Easy Jet, Air Canada & Iberia. The portfolio is well diversified geographically: 40% Asia/Pacific, 30% Europe, 25% in North and South America, and about 8-10% in the Middle East/Africa.

- AYR’s credit profile improved in recent months with the acquisition by minority stakeholder Marubeni in a joint venture with Mizuho, which was announced late last year and closed at the end of 1Q20. Japanese conglomerate Marubeni (rated Baa2/BBB), with an enterprise value over $30 billion, raised its ownership in AYR to 75% with a $1.1 billion investment. The new foreign ownership provides considerable implicit financial support that wasn’t there previously. Fitch upgraded the rating to BBB from BBB- on completion of the acquisition. At the time the acquisition was announced, there was some indication that the new owners might seek to completely refinance AYR’s outstanding debt obligations with a large-scale recapitalization, but that doesn’t seem to be the case. Instead they appear be doing more traditional tender/retire and re-issue as the market permits. AYR last tapped the public debt markets in August of this year with a $650 million 5-year debt launch, a portion of which was earmarked to be utilized to refinance or redeem upcoming debt maturities.

- Moody’s affirmed AYR’s senior Baa3 rating last month and assigned a stable outlook. The rating agency had placed most of the IG players in the industry on watch negative back in June of this year. Moody’s highlighted the company’s improved liquidity profile, which it believes makes the credit more resilient to a lengthy downturn in the global aviation sector. The rating agency also cited the Marubeni/Mizuho ownership described above. The affirmation of the rating helps alleviate near-term risk of a move to non-investment grade; AYR bonds do not include coupon step-up language.

Management reports that they have over $2 billion in available liquidity. AYR has $500 million in senior debt maturing in each 2021 and 2022, ahead of the $1.15 billion due in the bond’s maturity year of 2023. The Company has $319 million in cash on the balance sheet as of 2Q20, plus $1.08 billion in available capacity on its credit facilities through 2022. Cash flow from operations is typically over $500 million annually.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.