Uncategorized

Positioning for inflation

admin | October 16, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

The Fed has struggled to get inflation above its target for most of the last decade, but a couple of things have put it back on investors’ agenda. QE, fiscal stimulus and the Fed’s new flexible average inflation targeting have raised inflation risk and driven up market pricing for it. But investing in a market with rising inflation expectations may be somewhat of a lost art. Fixed income assets that lose value with inflation are easy to spot. Assets that gain value are harder. But they are out there.

The state of inflation expectations

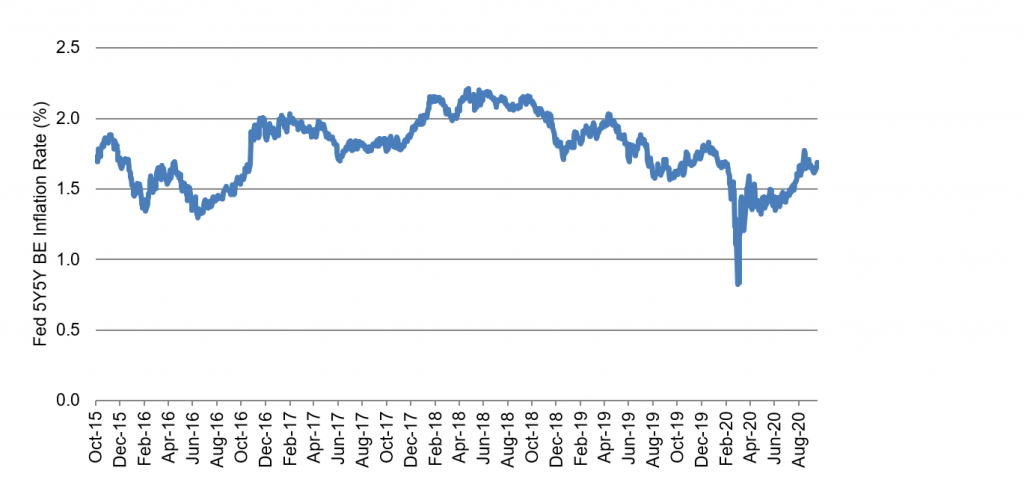

Expected future inflation has been on the rise lately. The 5-year forward 5-year implied inflation rate, a favorite of the Fed’s, fell toward 80 bp in mid-March before rebounding (Exhibit 1). It has climbed steadily since July, peaking at 177 bp immediately after the Fed outlined its new inflation policy at Jackson Hole. Expectations have moved higher lately on prospects of new pandemic stimulus either before or after the November 3 US elections and on the possibility of a Blue Wave and expanded federal spending in a new administration. Expectations nevertheless are slightly below the median of the last five years and still below the Fed’s target of 2.0%.

Exhibit 1: Expected inflation is moving up but is still below the Fed’s 2% target

Source: Bloomberg, Amherst Pierpont Securities

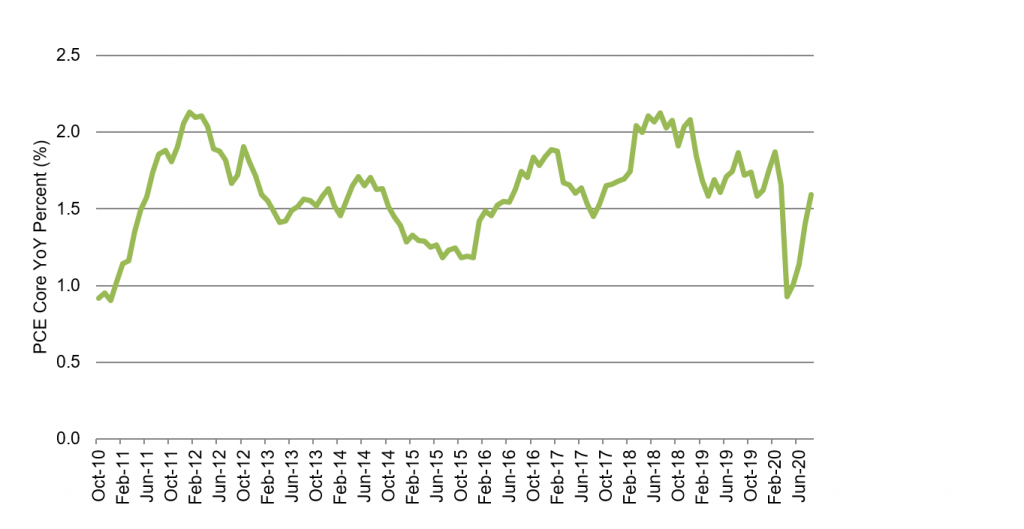

More than a decade with inflation below 2.0% despite the Fed’s best efforts have left their mark (Exhibit 2). Explanations for low inflation vary: globalization has made markets more competitive, technology has lowered production and input costs, the Internet has made price shopping easier. However, a few new factors are in play: QE, the Fed’s willingness under flexible average inflation targeting to let inflation run above 2.0% and the potential for fiscal expansion. They all raise inflation risk. This is especially true when development of one or several ways to contain Covid-19 could quickly revive the economy amidst very easy financial conditions.

Exhibit 2: A decade with core inflation largely below 2% weighs on expectations

Source: Bloomberg, Amherst Pierpont Securities

Correlations tell the story: winners and losers with inflation

Past shifts in asset value as inflation expectations change should help identify the expected inflation winners and losers. Correlations between changes in inflation expectations and returns in different assets identifies at least three distinct groups:

- Generally safe assets with cash flows that lose value with rising inflation and gain value with falling inflation

- Riskier assets from issuers that can more easily pay off nominal debt as inflation rises and might find it harder to pay off debt as inflation falls, and

- Assets backed by property or commodities that gain value with rising inflation and potentially lose value with falling inflation

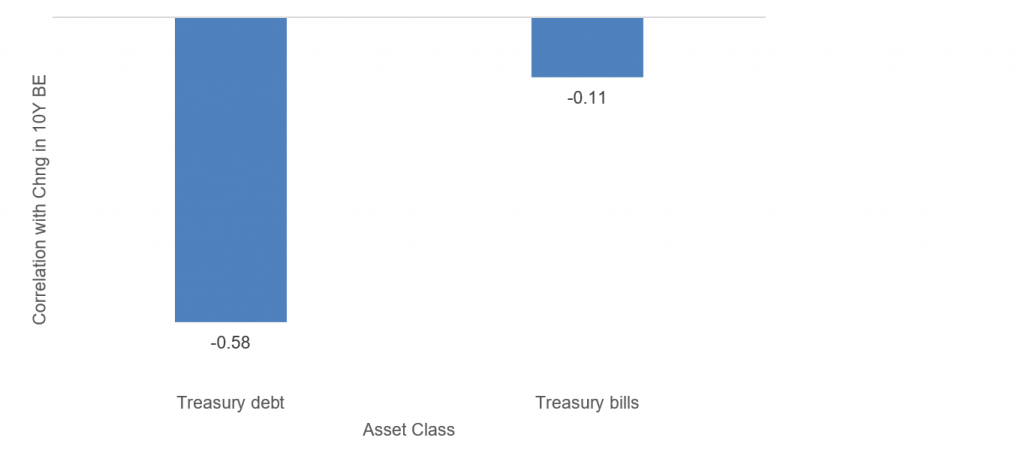

The safest assets lose value as inflation rises and gain value as it falls. Treasury debt is the best example. Rising inflation expectations add to the yield required as compensation, driving down price. The negative correlation between changes in 10-year implied inflation and returns on Treasury debt (-0.58) bear that out (Exhibit 3). Even the correlation with Treasury bills is negative (-0.11).

Exhibit 3: Negative correlations between expected inflation and riskless assets

Note: data shows the correlation of monthly changes in the 10-year US Treasury breakeven inflation rate and monthly returns on the Bloomberg Barclays indices of Treasury debt and Treasury bill returns from 2000 to 2020.

Source: Bloomberg, Amherst Pierpont Securities.

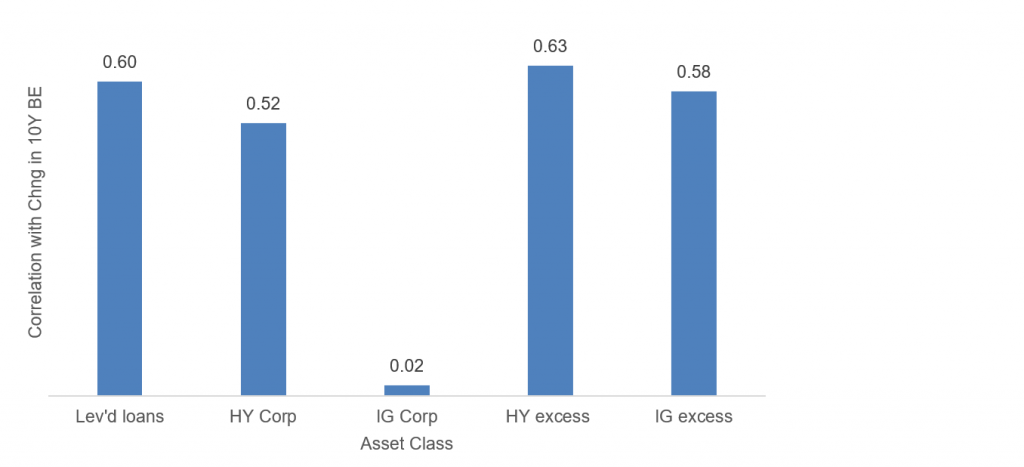

Some risky assets are net beneficiaries from inflation, rising in value as inflation rises and falling as inflation falls. Corporate debt offers good examples, although debt backed by households could serve, too. Correlations between expected inflation and leveraged loan returns (0.60) and between expected inflation and high yield returns (0.58) are positive. This is debt from highly leveraged issuers potentially able to pay off nominal balances with revenues enhanced by rising inflation. If revenues to highly leveraged companies—or wages to highly leveraged households—rise faster than interest costs, the issuer improves its ability to pay down debt, and spreads on the debt should tighten. Leveraged loan borrowers have floating-rate debt and high yield issuers have fixed-rate, but spread movement in those markets usually dominate interest rate effects. The correlation with returns on investment grade debt is low (0.02), but that mixes both the impact of interest rates and spreads. After stripping out the effect of interest rates by looking only at excess returns, the correlation with high yield excess returns rises (0.63) and with investment grade excess returns jumps (0.58).

Exhibit 4: Positive correlations between expected inflation and risky assets

Note: data shows the correlation of monthly changes in the 10-year US Treasury breakeven inflation rate and monthly returns on the Bloomberg Barclays indices of HY, IG, HY excess and IG excess and the S&P/LSTA index of leveraged loan returns from 2000 to 2020.

Source: Bloomberg, Amherst Pierpont Securities.

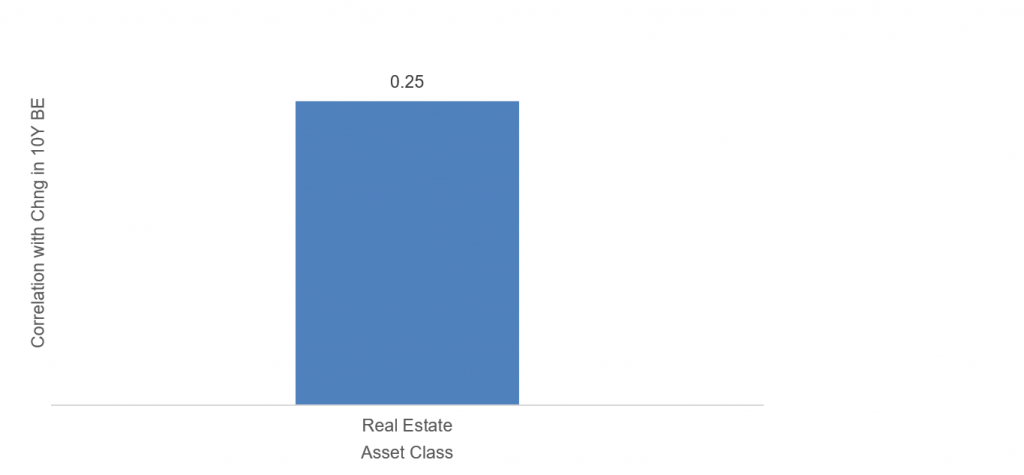

Some debt gets issued against collateral that can appreciate as inflation rises or depreciate as it falls, including real estate. A rising value for underlying collateral should tighten debt spreads. In the case of residential MBS backed both by real estate and implicitly by the borrower’s ability to pay, rising wages would reduce risk in the debt and tighten spreads, too. The positive correlation between changes in expected inflation and returns on US REITs (0.25) bears that out.

Exhibit 5: Positive correlations between expected inflation and real estate

Note: data shows the correlation of monthly changes in the 10-year US Treasury breakeven inflation rate and monthly returns on Dow Jones US Real Estate Total Return index from 2000 to 2020. Source: Bloomberg, Amherst Pierpont Securities

Of course, investors able to go long and short could also take a position in inflation by buying TIPS and selling appropriate nominal Treasury debt against it. The position would neutralize interest rate exposure and profit from interest cash flows and principal balance that rises with inflation.

Position for rising expectations

The prospects for rising inflation argue for allocating away from assets that provide return largely for interest rate risk and toward assets that provide return for credit risk. The time seems right for trimming allocations to Treasury debt and adding to allocations in high yield corporate or structured credit.

* * *

The view in rates

The 5s30s curve continues to steepen faster than 2s10s, reflecting more sensitivity to inflation risk. QE, the Fed’s flexible average inflation targeting and possible fiscal stimulus are all helping. With a Democratic sweep, the prospect of Biden’s proposed $4 trillion of additional federal spending over the next 10 years would add to the pressure. Some of the pressure toward higher, longer rates comes from supply, some from potential inflation. The market now bids 10-year breakeven inflation at 171 bp, slightly below the 180 bp peak right after Jackson Hole.

The view in spreads

The next leg of tighter spreads should come after the conclusion of the coming elections. That conclusion may land well after November 3. At that point, an important element of uncertainty should resolve, and risk assets should rally. In the aftermath of elections, risk assets remain caught between Fed buying on one hand and heavy net supply of Treasury debt on the other. There is still fundamental risk in the most leveraged corporate balance sheets with corporate leverage going up through 2020, and only there might spreads continue lagging the rest of the market.

The view in credit

Fundamental credit remains as uncertain as the economy, and the lack of new fiscal stimulus increases risk for households and small businesses. The downside in leveraged credit has outweighed the upside since March, and the imbalance without fiscal stimulus looks likely to get worse. Many investment grade companies have stockpiled enough cash to survive protracted slow growth, but highly leveraged companies and consumers are at risk. High yield and leveraged loans have nevertheless done well. But the hard part is about to start as winter approaches and some of the outdoor activity that sustained bits of the economy starts to go away.