Uncategorized

A cure for at least some pandemic delinquencies

admin | October 16, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Investors continue to focus on the risk that servicers might buy out delinquent loans from Ginnie Mae MBS at par. Bank servicers have taken quick advantage of this, but non-bank servicers not so much. Delaying buyouts gives loans time to cure and remain in the pool. Ginnie Mae data shows that nearly 11% of loans that first became delinquent after March have already cured as of October 1 and no longer pose an imminent buyout risk. FHA loans show the highest cure rate, likely due to the FHA’s partial claim program, which permits the borrower to defer repayment of delinquent payments at no interest until the loan is paid off or matures.

Both the MBA and Black Knight have reported that many loans, as high as 18% of delinquent FHA/VA loans, have exited forbearance in the first week of October. Many borrowers reached the end of their initial 6-month forbearance term at the start of October. Unless these loans re-enter forbearance—perhaps there have been delays placing borrowers on forbearance extensions—it means that a significant number of delinquent loans should cure or prepay this month.

Fewer new loans are becoming delinquent

The balance and number of loans in Ginnie Mae MBS that became delinquent after the economy was disrupted is shown in Exhibit 1. Only loans that were current on March 1 are included. Each row shows how many loans first reached 60 days delinquent in that month. The table shows that the pace of new delinquencies has fallen sharply. For example, on June 1 roughly 475,000 new loans reached 60 days delinquent, but only 91,000 loans did on September 1.

Exhibit 1: The pace of new 60+ day delinquencies has plummeted since June

Each row shows the balance and number of loans that first reached 60 days delinquent in that month. A loan that subsequently cures and redefaults is only included the first time it reached 60 days delinquent.

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities

A loan that is 60 days delinquent poses a buyout risk. If that borrower misses the payment that was due at the start of the current month, the lender will be able to buyout the loan this month. The table starts in May because a loan that was current on March 1 but missed payments due March 1 and April 1 would be 60 days delinquent on May 1. The largest months for loans to reach 60-days delinquent were June and July, since most borrowers first missed their April or May payment.

However, not every loan has been bought out. Many loans are still delinquent, but some borrowers have cured their delinquencies. Bank servicers have been aggressive at buying out delinquent loans since they have access to inexpensive funding and are required to consolidate delinquent loans onto their balance sheet regardless of whether the loan is in a pool. But non-bank servicers have been far less aggressive at buyouts (Exhibit 2)

Exhibit 2: Over 13% of non-bank serviced delinquent loans have cured

Each row shows October 1 status of every loan that became 60 days delinquent for the first time between May and September. The delinquency status is shown for loans that are still in pools, otherwise it reports whether a loan prepaid or was bought out. All data is percent by balance.

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities

Banks have bought out 72% of these loans as of October 1, but non-banks have only bought out 7%. The lower non-bank buyout rate has allowed 13% of delinquent loans to completely cure, compared to only 8.1% of bank loans. A few large banks have been responsible for most of the buyouts.

More FHA loans have cured than VA loans

More FHA loans have already cured than either VA or rural housing loans. This is likely due to the FHA’s partial claim program, which permits the borrower to defer repayment of delinquent payments at no interest until the loan is paid off or matures. The FHA requires servicers to evaluate borrowers exiting Covid-19 forbearance for the partial claim before considering any other alternative. The USDA’s program (“Mortgage Recovery Advance”) is not prioritized in the same fashion; lenders must first assess borrowers for repayment plans and loan modifications. The VA and Ginnie Mae recently tweaked their rules to permit VA servicers to offer no interest payment deferrals. However, these deferrals would be funded by the servicer and not the VA, so are unlikely to be used very often. HUD and USDA fund their payment deferral programs.

Exhibit 3: FHA loans have higher cure rates than VA and rural housing

The table shows the % by balance for each government loan type, for all loans that were current on March 1 and subsequently became at least 60 days delinquent. Status is as of October 1.

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities.

VA loans have slightly higher voluntary prepayment speeds than the other government agencies. The VA permits lenders to refinance delinquent loans, which cures the delinquency. This might be more attractive to some borrowers and lenders than a loan modification.

Public Indian Housing (PIH) loans show the highest cure rates—17.6% of delinquent loans are no longer delinquent. PIH loans also have the highest 30-day delinquency rates, and those loans are not eligible for buyout. The sample is small but suggests that buyers of PIH specified pools may face somewhat lower buyout risk.

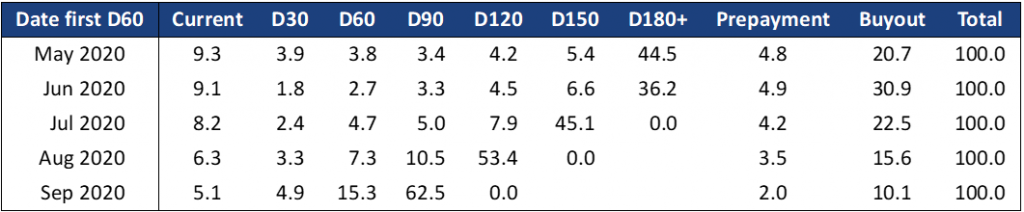

Exhibit 4 shows the October 1 status of each monthly cohort of delinquent FHA loans. Each row includes loans that first became 60-days delinquent in that month, and the columns show the status of those loans as of October 1. This means that the loans in the May 2020 cohort have had five months to buyout, prepay, cure, or remain delinquent. Over 13% of loans in the June cohort, the largest group, have cured. Even 6.5% of loans that were 60-days delinquent on September 1 cured by October 1.

Exhibit 4: FHA loans, status of delinquent loans as of October 1 (% by balance)

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities.

VA cure rates are lower than FHA cure rates for every cohort (Exhibit 5). But the gap is larger for the longer delinquencies, suggesting the propensity for VA loans to cure drops rapidly as the borrowers fall further behind. The VA has fewer options to cure delinquencies other than through loan modification. The VA does not fund payment deferral plans or repayment plans, so the servicer is more likely to refinance or modify the loan. VA buyout rates also tend to be lower than FHA buyout rates, but this may be driven more by the behavior of the VA-focused servicers than any underlying difference in the program.

Exhibit 5: VA loans, status of delinquent loans as of October 1 (% by balance)

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities.

Rural housing loans have fared a bit worse than FHA loans (Exhibit 6). The cure rates are closer to that of VA loans, while the buyout rates have been slightly higher than FHA loans.

Exhibit 6: Rural Housing Service (RHS), status of delinquent loans as of October 1 (% by balance)

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities.

Many Public Indian Housing (PIH) loans have cured over the last 5 months (Exhibit 7). Although the sample size is small this outcome is evident across each of the 5 cohorts. Consequently, fewer PIH loans have ended up as buyouts than have loans from the other agencies.

Exhibit 7: Public Indian Housing (PIH), status of delinquent loans as of October 1 (% by balance)

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities.