Uncategorized

Keeping track of servicer behavior in RMBS

admin | September 18, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

As borrowers in RMBS trusts rolled into forbearance this year, it became increasingly apparent that treatment of these loans would vary across servicers and across different types of mortgage credit. As servicers have extended payment forbearance terms, these differences remain pronounced, affecting not only cash flows to various RMBS trusts but the optics of loans in forbearance as well.

Unlike servicers of Fannie Mae, Freddie Mac and Ginnie Mae loans, servicers of loans in private-label trusts have significantly more latitude in the treatment of loans in forbearance. The duration of forbearance terms, extension of those terms, classification of borrowers in payment forbearance to trustees and advancing policies have diverged fairly significantly across servicers. Some of the key differences across servicers have been whether they have reported a borrower as delinquent while in forbearance or employed capitalization modifications and continued to mark the borrower as current. And even in the case where the borrower is marked as delinquent, there are noticeable differences in the amount of loans where the servicer makes a full advance of principal, interest, taxes and insurance to the trust.

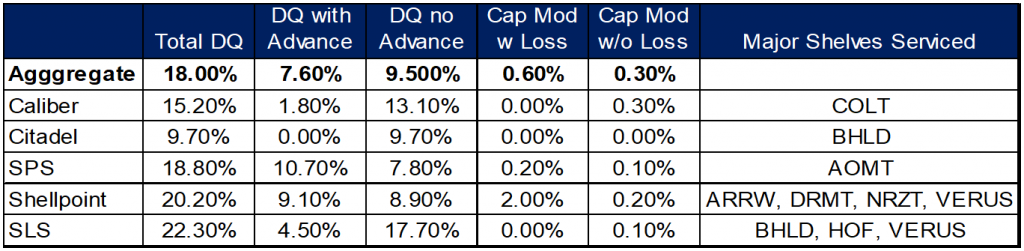

Breaking down the non-QM sector

Total delinquency rates across the non-QM sector remain elevated. As of the August remittance cycle, roughly one fifth of loans in non-QM trusts were in some stage of delinquency or were marked as current with payments capitalized. Based on the August remittance, more than half of delinquent loans in non-QM trusts are not receiving full advances. This is somewhat surprising given that the majority of non-QM trusts employ a 180-day stop advance policy. Servicers have likely not yet made six months of advances on loans in forbearance given that the earliest most of these borrowers could have entered forbearance would be the April remittance cycle on their March payment. Select Portfolio Servicing (SPS) and Shellpoint appear to be advancing more against delinquent loans than their peers at 56.9% and 46% advance rates on delinquent loans respectively, while Citadel and Caliber exhibited some of the lowest advance rates in the sector. In the case of Citadel, per prospectus language in Bunker Hill non-QM trusts, they are not required to advance principal and interest, so the absence of principal and interest advances by that particular servicer is to be expected. (Exhibit 1)

In addition to advances, investors have been focused servicers’ employment of capitalization modifications, especially those that generate a current period loss to the trust if capitalized payments are deferred to the maturity date of the loan in non-accrual status. These capitalization modifications made up 3.3% of August delinquencies and were localized mainly to Shellpoint where they accounted for roughly 10% of delinquent loans serviced by them.

Exhibit 1: Breaking down servicer behavior in non-QM trusts

Source: Amherst Insight Labs, Amherst Pierpont

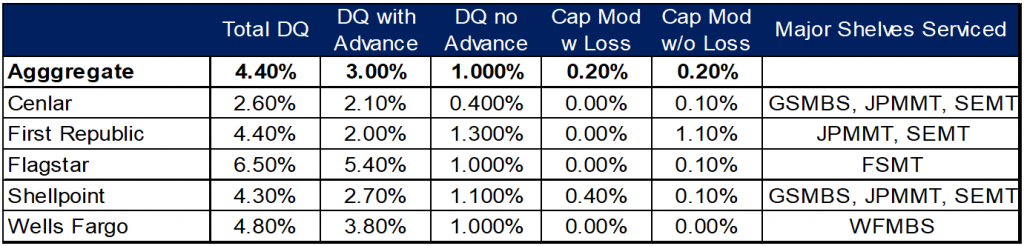

Breaking down the prime 2.0 sector

Looking across servicers of prime 2.0 trusts there are similar disparities. Unsurprisingly, aggregate delinquency rates in August were significantly lower than non-QM with aggregated delinquencies totaling 4.4%. Advance rates were generally elevated relative to non-QM trusts as well with an aggregate advance rate of nearly 70% for the sector, likely driven by lower overall delinquency rates. With that said, certain servicers exhibited far higher advance rates than others. Cenlar, Flagstar and Wells Fargo all had advance rates in the neighborhood of 80% on delinquent loans in August, while First Republic and Shellpoint exhibited far lower advance rates. (Exhibit 2)

Exhibit 2: Breaking down servicer behavior in prime 2.0 trusts

Source: Amherst Insight Labs, Amherst Pierpont Shelves analyzed exclusive to FSMT, GSMBS, JPMMT, SEMT, WFMBS . No performance data available for Chase FSB or Chase Mortgage

Lower advance rates in prime trusts were largely commensurate with a greater incidence of capitalization modifications by prime servicers. Consistent with the prior analysis of the May remittance, First Republic and Shellpoint exhibit a higher incidence of capitalization modifications than the broader peer group. By and large the incidence of capitalization modifications was limited in the SEMT shelf likely driven by the 120-day stop advance policy on delinquent loans securitized in those trusts. One important distinction is that while capitalization modifications made up 25% of delinquencies in August, the capitalization modifications did not generate a loss to the trust. Conversely, roughly 10% of Shellpoint delinquencies received a capitalization and deferral modification where the trust realized a current period loss as that current period deferred interest, taxes and insurance were effectively converted to principal forbearance and capitalized with the option for potential future recovery at maturity, sale or refinancing in the future.

An additional consideration in prime jumbo space is the presence of variable servicing fee structures. Both Flagstar and Chase currently employ a variable servicing fee structure where they receive minimal compensation for servicing performing loans. These structures were particularly susceptible to prepayment related interest shortfalls and elevated prepays coupled with relatively elevated delinquencies could lead to an increase in capitalization modifications as servicing income declines and advance liabilities increase.

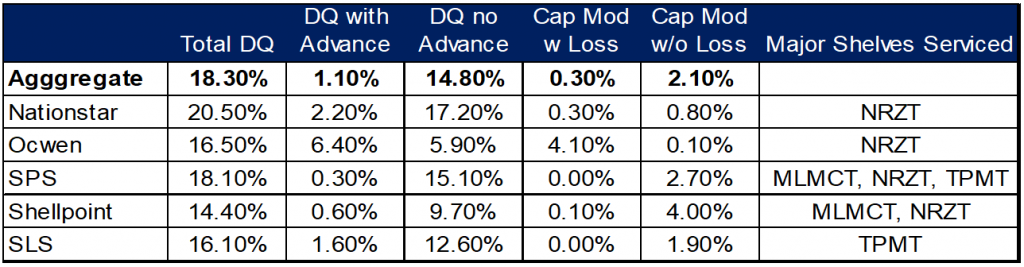

Breaking down the RPL sector

By and large the RPL sector is somewhat fundamentally different than other areas of mortgage credit in that servicers are generally only obligated to advance taxes and insurance on delinquent loans while interest deficiencies associated with delinquent loans will generally result in an interest shortfall that can be reimbursed to bond holders in the future. However, there is some nuance to this as shifting interest securitizations of loans called from previously outstanding legacy RMBS trusts do require the servicer to make advances of principal and interest. Given this, couple with the fact that Ocwen services a significant population of loans in shifting interest RPL structures, they tend to look like somewhat of an outlier with regards to servicer behavior across RPL trusts.(Exhibit 3)

Exhibit 3: Breaking down servicer behavior in RPL trusts

Source: Amherst Insight Labs, Amherst Pierpont

Ocwen advanced on roughly 40% of delinquent loans they service across all RPL trusts while performing capitalization modifications that resulted in a loss on roughly 25% of what would otherwise be delinquent loans making it somewhat difficult to predict how Ocwen may handle loans in forbearance securitized in RPL trusts. Both SPS and Shellpoint are employing capitalization modifications in RPL trusts as well. However those modifications are not generating a current period loss. Given the fact that that investors in RPL structures by and large have no expectation of receiving delinquent interest on loans in forbearance they may be more agnostic to capitalization modifications, specifically those that do not erode credit enhancement. However, if the servicers’ primary motivation for using these types of modifications is to keep the borrower current and reduce the advance liabilities, it seems somewhat curious that servicers would employ them in instances where they are not obligated to make those advances.

Breaking down the legacy sector

Increasing delinquencies in legacy RMBS this spring gave rise to a new wave of idiosyncratic servicer behavior. In addition to advancing and modification issues, Ocwen provided at additional level of complexity and opacity to the market in Ocwen was making advances on loans in forbearance but still marking them as current pay. This phenomenon was discovered as a result of an analysis why legacy subprime loans serviced by Ocwen exhibited lower delinquency rates than those of other servicers even after accounting for capitalization modifications. And in a reporting nuance apparently unique to the legacy market, a certain subset of loans serviced by Ocwen have been marked as current for the purpose of trustee reporting but are being tagged as in forbearance by Ocwen and the trust is receiving advances of borrowers’ arrearages from Ocwen. This issue appears to be primarily relegated to loans securitized in trusts where Deutsche Bank is the trustee and the issue appears to be ongoing. (Exhibit 4)

Exhibit 4: Breaking down servicer behavior in legacy trusts

Source: Amherst Insight Labs, Amherst Pierpont

This treatment of loans in forbearance continues to be prevalent amongst Ocwen serviced legacy loans. Roughly 12% of delinquent Ocwen legacy loans were marked as current in August with no capitalization and subsequent increase in the balance of the loan. Despite this incremental opacity and potential understatement of Ocwen serviced loans in that are delinquent and in forbearance, there has been little to no perceivable price concession on Ocwen serviced legacy trusts. This is somewhat surprising given the fact that Ocwen has employed this servicing practice on roughly 10-15% of their population of delinquent loans every month since the May remittance. Additionally, Ocwen has a much higher incidence of capitalization modifications and as a result a far lower advance rate on delinquent legacy loans than other legacy servicers. The confluence of idiosyncratic forbearance reporting, higher frequency of capitalizations and lower advances should add up to lower prices on bonds serviced by Ocwen relative to other servicers all else equal.