Uncategorized

In the political season

admin | September 18, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Elections bring uncertainty to markets, just like any other event. But the elections on November 3 have brought more than the usual, at least as measured by options markets. The expected volatility partly reflects an ideological gap between the major parties larger than any time in US history and partly reflects the risk of a contentious process in the time of Covid. The implications for markets, however, only seem clear in the case of a single party sweep of Congress and the White House. The impact on longer rates in that case seems the clearest. The impact on spreads seems reasonably clear. The impact on other markets seems more subtle.

High volatility, high public interest, high policy risk

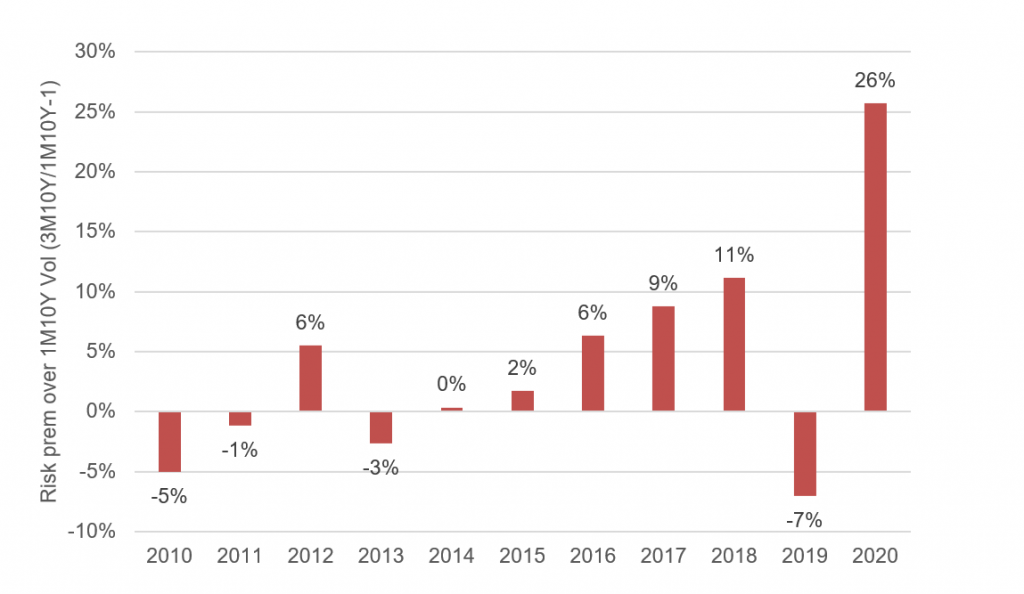

The interest rate options markets at this point reflects more risk for the 2020 election than any other presidential or mid-term election in at least the last 10 years. The current 1-month option to enter a 10-year swap does not cover the election, for example, while the 3-month option covers the election and its immediate aftermath, among other things. The 1-month option shows implied annual volatility of 52.50% while the 3-month option shows 65.98%, a 26% increase in risk (Exhibit 1). This compares to much smaller risk premiums at the same point for the elections of 2010, 2012, 2014 and 2016. Only the 2018 mid-term election comes remotely close with a risk premium of 11%.

Exhibit 1: Rate options imply more risk in 2020 than any recent national election

Note: The ratio of 3M10Y swaption volatility to 1M10Y swaption volatility. Chart shows percentage deviation from 1.0. Annualized normal implied volatility on 9/15/2020. Option prices reflect all events that occur before expiration including elections, Fed meetings, economic announcements, and other influences.

Source: Bloomberg, Amherst Pierpont Securities

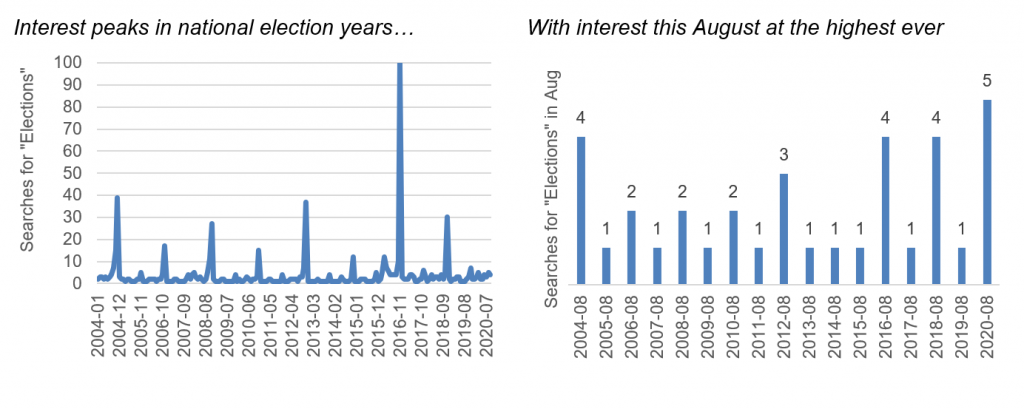

The broader public also has its eye on this race more closely than any other recent national race. Google Trend data on searches for “election” shows a peak in interest in November of each presidential and mid-term election year this century, with interest in November 2016 running at least two and a half times the rate of any earlier election (Exhibit 2). The peak in 2020 is likely to set a record. As of August, interest already stood well above levels for any prior presidential or mid-term year.

Exhibit 2: Public interest in this election is also likely to set a record

Source: Google Trends, Amherst Pierpont Securities

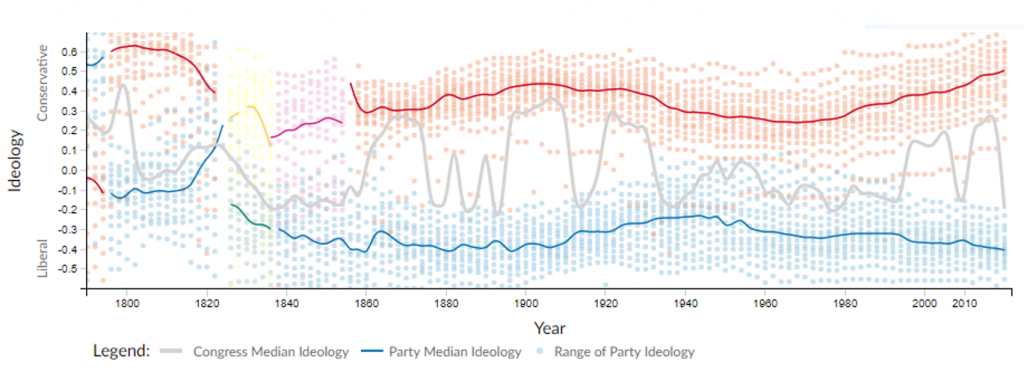

The high implied volatility and public interest reflect a Congress with an ideological and policy split larger than any other time in US history. Since the 1950s, the Democratic Party has become steadily more liberal and the Republican Party more conservative (Exhibit 3). The Democratic Party is as liberal as it has been in 100 years. The Republican Party is as conservative as it has been in 200 years. The significant overlap between the parties from 1940 through 1980 has disappeared. In an election without single party control across Congress and the White House, the potential for policy swings is low. With single party control, the potential is high.

Exhibit 3: The ideological gap between major US parties has never been wider

Source: Voteview.com from the UCLA Department of Political Science

The probability of a single party sweep

The probability of a single party sweep largely amounts to the probability of a blue wave. Republicans could win the House, but predictit.org currently puts the probability of Democratic control at 84% with the Iowa Electronic Markets at 79%. Outcomes for Senate and White House are much more likely to tip the scales on single party control. Predictit.org shows the probability of Democratic control in the Senate at 61% with IEM at 60%. Good Judgment estimates the probability of Democratic control of House and Senate at 68%. That leaves the White House. Predictit.org puts the probability of a Democratic win at 57%, IEM at 72%, Good Judgment at 74% and fivethirtyeight at 76%. Nevertheless, these outcomes are not independent, and Predictit.org still sees the chance of a Democratic clean sweep at 50%. As 2016 showed, a lot of things can happen in the last few weeks of an election campaign.

Fiscal policy, FAIT and impact on rates

Fiscal policy looks most likely to swing depending on Democratic or Republican control with clearest impact on longer rates and the slope of the yield curve. The Democratic-controlled House in May passed a $3 trillion fiscal stimulus bill with the Republican majority in the Senate proposing in August a $1 trillion bill. A scoring of the Biden tax plan in March by the Urban-Brookings Tax Policy Center showed a net gain in the next 10 years of nearly $4 trillion in federal revenue. Although negotiations even under single party control could move plans from aspirational to practical, a Democratic sweep suggests a swing in fiscal policy of at least several trillion dollars.

A surge of fiscal policy stands to have an especially big impact under the Fed’s new flexible average inflation targeting. Fiscal stimulus would likely drive unemployment down without generating the kind of preemptive tightening of monetary policy used by the Fed in the past. The Fed would get its first test of FAIT, and longer rates would likely rise to reflect new risk premium, steepening the yield curve.

A steeper curve would have the usual effects on other parts of fixed income. All MBS and other callable bonds would generally trade to longer durations. In MBS, 15-year pass-throughs would likely outperform 30-year, and higher coupons would likely outperform lower. Capped floaters would likely underperform.

Impact on credit

Credit looks a little harder to predict than rates, but the broad outcome here depends less on party than it does on resolution of uncertainty. Resolving any source of uncertainty tends to lift risk assets, which is likely why equity markets on average rally in the months after a presidential election. The additional impact of a Democratic sweep would depend on whether the market sees fiscal spending as having a bigger impact on growth and profitability than the proposed Biden increases in corporate taxes. Regardless of control after results of the election become final, credit spreads in general, with the Fed’s continuing support, look likely to take another leg tighter.

Impact on the Fed

Fed policy looks unlikely to change even with single party control largely because the Senate has been a careful gatekeeper to the Federal Reserve Board. The board currently has two of its seven seats open, and Powell’s term as chair ends in 2022. Criticism in recent years from the White House aside, the Fed has enjoyed significant support for its approach in the Senate. The Senate has discouraged several nominees with views outside the Fed consensus on best approaches to monetary policy and is stuck for now on the pending nomination of Judy Shelton. Even though Congress could modify the policy goals of the Fed, as it has several times in Fed history including through Dodd-Frank in 2010, it looks unlikely to interfere with the Fed’s approaching to reaching those goals. Powell may not get reappointed as chair at the end of his term, but continued success of monetary policy should keep the seat occupied by someone with consensus credentials.

Impact on mortgage finance

A Democratic sweep could change the direction of policy in mortgage finance through its impact on the Federal Housing Finance Agency. The current director of FHFA, Mark Calabria, would like to recapitalize Fannie Mae and Freddie Mac and put them in private hands. A Democratic White House would likely look for other ways to get the GSEs out of conservatorship, and a sweep could open the door to legislative reform. Legislative reform could very likely involve an eventual full-faith-and-credit guarantee for Fannie Mae and Freddie Mac securities. A sweep could also expand programs to finance affordable housing.

A contested election

A contested election would likely make good on the volatility priced into the options market. Close results that shift back and forth as votes get counted, contested or both would likely leave changes in policy hanging on relatively few ballots. It might also deepen the divide between the major parties, raising the risk of further policy extremes.

Politics becomes P&L

As probabilities shift for the outcomes and aftermath of November 3, the market should see it priced into the yield curve, the spread of risk assets, the niches of the corporate and structured credit market likely to win or lose with changes in policy, and elements of MBS. In the political season, politics becomes market P&L.

* * *

The view in rates

The Fed’s new framework for managing monetary policy—flexible average inflation targeting that only offsets shortfalls in employment—should steepen the yield curve as the implications sink in in coming weeks and months. The Fed will likely only tighten if inflation shows up, not necessarily if unemployment runs too low. The new approach could see inflation run clearly above 2.0% and possibly above 2.5% for periods of time before the Fed might act to rein it in. That should pose the most uncertainty and most risk for longer maturities, push yields higher as the Fed holds the front of the yield curve down.

Rates in general have remained in roughly the same range since the end of March, although actual and implied rate volatility picked up slightly in August. The 10-year real rate has stayed around -100 bp for several weeks while the market holds onto its expectations of inflation with the spread between 10-year notes and TIPS implying inflation of 167 bp. Real rates still could drop further if the Fed this fall shows willingness to let inflation return to target and go higher, all the while holding nominal rates down.

The view in spreads

The next leg of tighter spreads looks likely to come after the conclusion of the coming elections. That conclusion may land well after November 3. Spread compression took a holiday in August as spreads broadly moved sideways and interest rate and equity volatility picked up, and that seems a reasonable expectation through November 3 and its aftermath. After final results, however, an important element of uncertainty should resolve and risk assets should rally. In the aftermath of elections, risk assets remain caught between Fed buying on one hand and heavy net supply of Treasury debt on the other. There is still fundamental risk in the most leveraged corporate balance sheets with corporate leverage going up through 2020, and only there might spreads continue lagging the rest of the market.

As a side effect of the steeper Treasury curve, projected OAS in MBS should rise as should option-adjusted duration. A steeper curve presents prepayment models with rising rates, and with almost the entire MBS market trading at a premium, rising rates mean slower prepayments and better spreads.

The view in credit

Fundamental credit remains as uncertain as the economy, and the lack of new fiscal stimulus increases risk for households and small businesses. The downside in leveraged credit has outweighed the upside since March, and the imbalance without fiscal stimulus looks likely to get worse. Many investment grade companies have stockpiled enough cash to survive protracted slow growth, but highly leveraged companies and consumers are at risk. Prices on some sectors of leveraged loans suggest distress ahead, despite the broad leveraged loan market completely recouping its losses in February and March. Elevated unemployment and delinquency rates in assets from MBS to auto loans show pressure on the consumer balance sheet. A rebound in growth in the third quarter should help, but the US has only recouped half of jobs lost since February. The next half looks likely to be harder.