Uncategorized

Return attribution summary for July 2020

admin | August 7, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

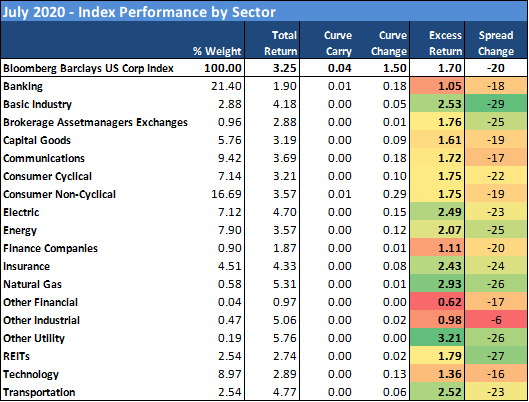

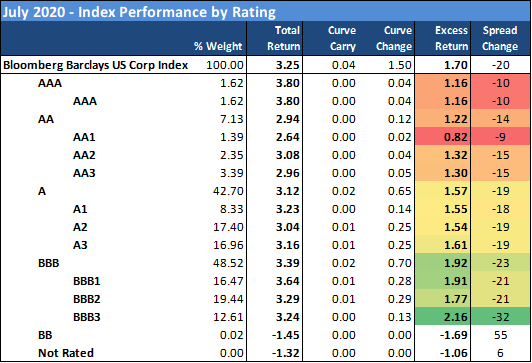

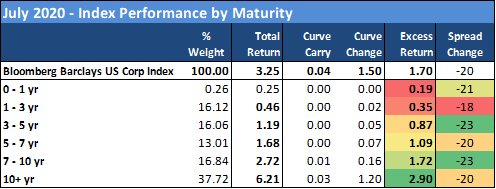

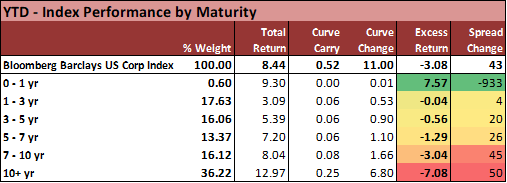

For another consecutive month, investment grade corporate bond investors targeted more risk and favored higher beta credits, but appeared to be bit more selective about which sectors they took on more credit and duration risk than in previous months. The IG Index tightened -20 bp in aggregate to +130 bp at month-end, trimming the year-to-date spread sell-off to a +43 bp move since the start of the year. July excess return was +1.70% with a total return of +3.25%, and 2020 returns stand at -3.08% and +8.44%, respectively.

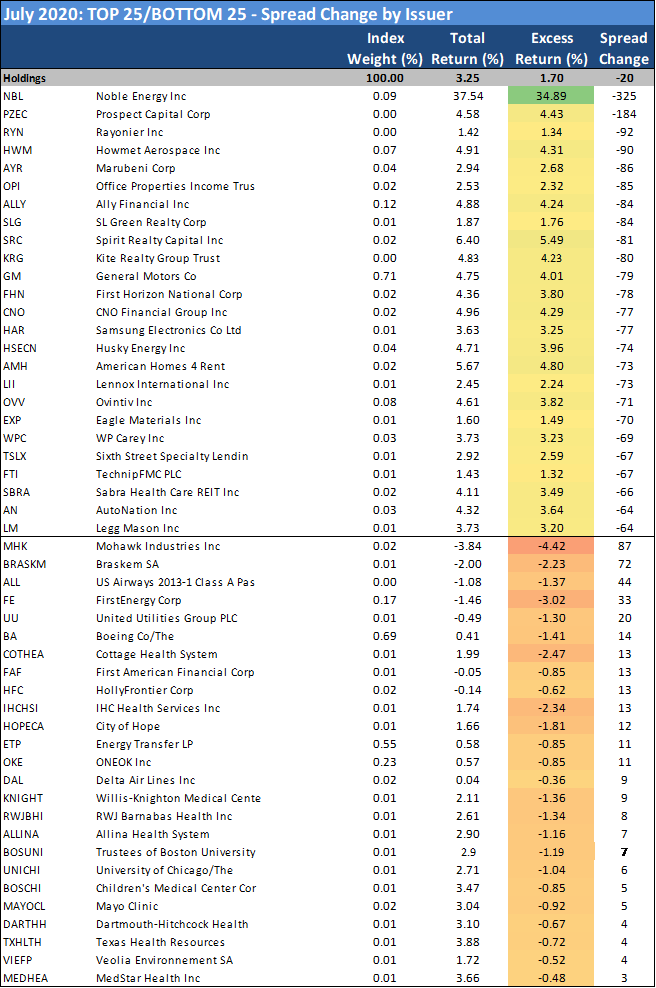

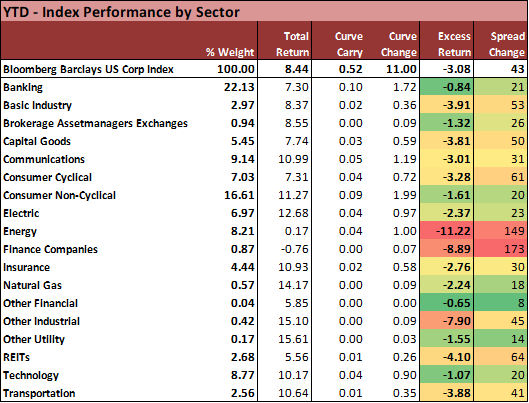

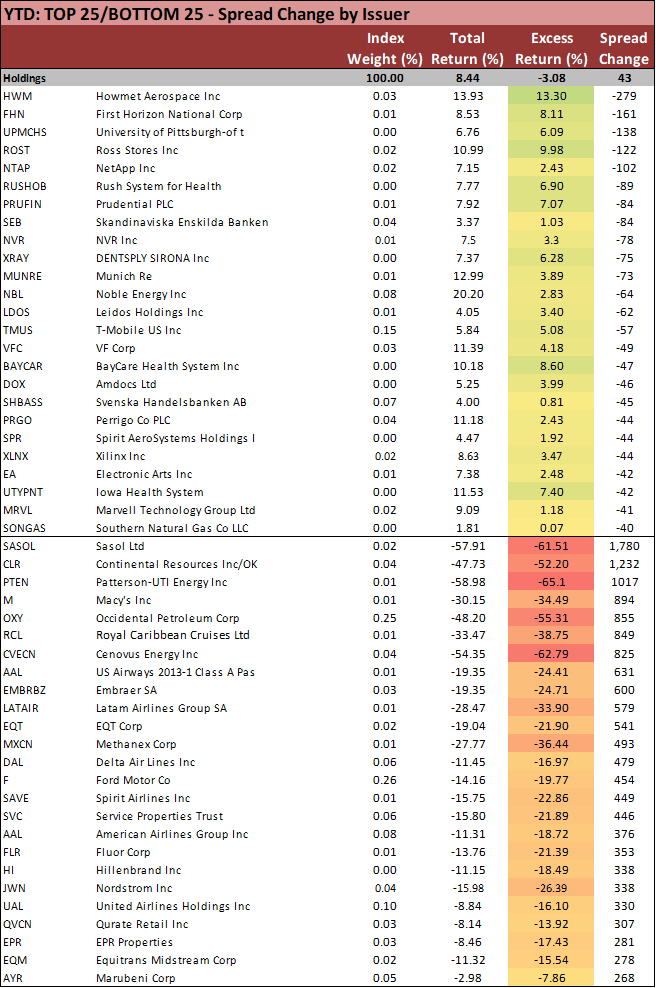

After leading the Index for two consecutive months, Energy (+2.07% excess return) fell out of the Top 5, as the recovery in oil prices stalled out in July, leading to more mid-tier performance in credit. Utilities were a favored strategy for July, with Electric (+2.49%) and Natural Gas (+2.93%) among the leading performers in the Index. Rounding out the top 5 were Basic Industry (+2.53%)—led by chemicals and precious metals credits—as well as Transportation (+2.52%) and Insurance (+2.43%), with investors seeking out long duration plays in credit. The 30-year US Treasury rallied to +1.20% at month end from over 1.40% at the prior month close. On the other side of the coin, Banking (1.05%) registered the single weakest return in July as the Treasury curve collapsed and projected interest margins compressed. Also falling out of favor from the prior month were Finance Companies (+1.11%) as the GE recovery story stalled on weak earnings and outlook in their 2Q20 results. Other bottom performers included Technology (+1.36%), Capital Goods (+1.61%)—due in large part to incredibly weak performance and disappointing outlook at Boeing—and Communications (+1.61%).

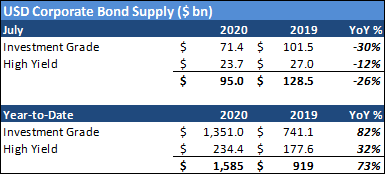

For the first month since February, IG corporate bond new issue failed to outpace volume for the prior year, posting a -30% drop year-over-year to $71.4 billion. High Yield volume also dropped by -12%. Issuance fell well short of expectations, even with muted estimates ($90-100 billion) coming into the seasonally weak month of July. The market is expecting comparable volume in the $50-60 billion range for the also light month of August, ahead of the seasonal deluge in September.

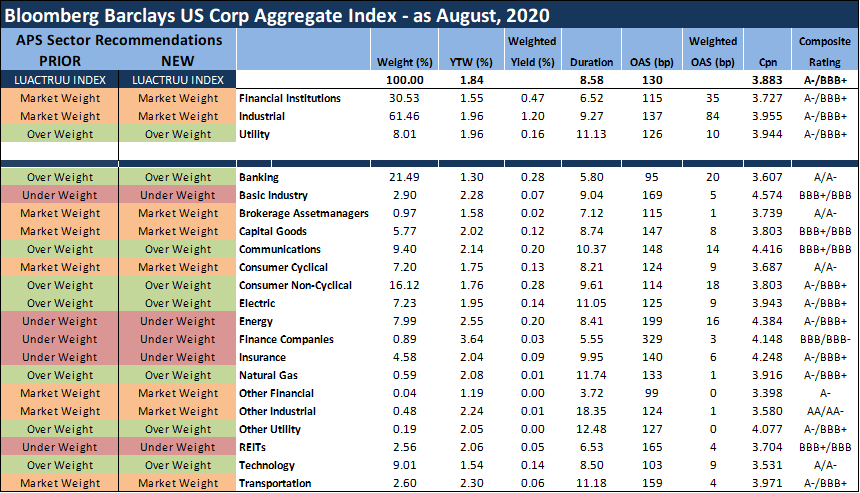

Sector recommendations remain unchanged

Investors should remain in a more defensive posture, based on concerns about the longer-term global economic fallout of COVID-19 outbreak and related earnings volatility, with the prospect for recurring spikes in volatility for the near-to-intermediate term. The compounded stress on energy/commodity markets is making it extremely difficult to time fluctuations in valuation among commodity credits, which further supports a call overweighting more defensive segments within the Index. With the re-pricing of credit risk year-to-date, the long-term valuation proposition in higher-rated, less-cyclical credits is compelling enough to forego more aggressive strategies that remain susceptible to shorter-term swings in volatility.

Exhibit 1. APS Sector Recommendations for August 2020

Note: The table summarizes how APS expects sectors within the IG Index to perform for the next several months, on an Excess Return basis (total return net of commensurate UST return). These weightings serve as a proxy for how portfolio managers should position their holdings relative to the broad IG corporate bond market. Source: Bloomberg/Barclays US Corporate Index, Amherst Pierpont Securities

Source: Bloomberg/Barclays Corporate Index, Amherst Pierpont Securities

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.