Uncategorized

The trajectory of the labor market

admin | July 31, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Monthly US employment figures posted a combined 7.5 million rebound through May and June, far stronger than most economists would have imagined a few months before. With the summer surge in the virus, there are fears that the economy and net hiring faltered in July. Rising initial unemployment claims in the second half of July have substantially added to that impression. However, the recent backup in initial claims appears to mainly reflect a seasonal adjustment that does not accurately track the unique underlying economic situation this year.

A summer stall in the labor market?

The resurgence of Covid in June and July led to a flattening out of a number of high-frequency economic indicators, especially those related to sectors most sensitive to the restrictions imposed by government lockdowns. With bars being re-closed and indoor dining being scaled back, foot traffic at those venues has stalled. Likewise, after rapid growth in May and June, private sources of labor market information, such as HomeBase and Kronos, showed a significant slowdown in the pace of gains in employees working in July.

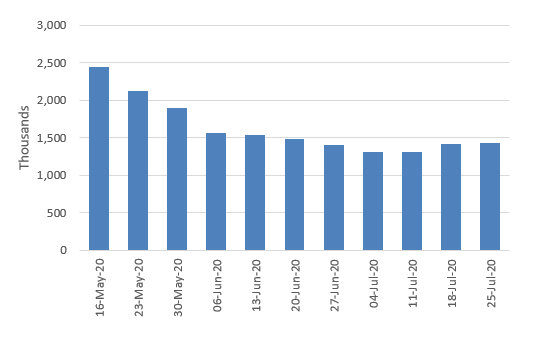

In this context, market participants are especially sensitive to any negative news on the economy and the labor market. That news came through in late July. After falling for months, the number of seasonally adjusted initial unemployment claims increased in the week ended July 18 and again in the period ended July 25 (Exhibit 1). Some in the market took these moves as a signal that the demand for workers is petering out.

Exhibit 1: Seasonally adjusted initial unemployment claims

Source: Labor Department, Amherst Pierpont Securities

An illusion?

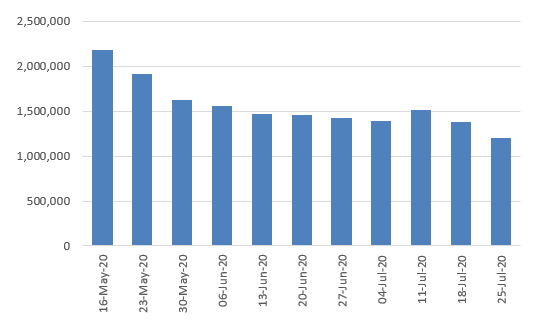

The recent moves shown appear to reflect a powerful seasonal adjustment more than a substantial rise in actual layoffs. As the non-seasonally adjusted numbers show, initial claims did flatten out in late June and early July, more in line with the timing of when a number of southern states were forced to scale back their reopenings, but actually resumed their downtrend in the last two weeks (Exhibit 2).

Exhibit 2: Non-seasonally adjusted initial unemployment claims

Source: Labor Department, Amherst Pierpont Securities

The divergence between the seasonally adjusted and unadjusted figures in July can be easily explained. In a typical year, a number of factories shut for one or two weeks, often for worker vacations or factory retooling. In this scenario, there is usually a flurry of layoffs, as suppliers and other businesses that are dependent on the factories are forced to temporarily furlough their workers. Once the factories return to full operation in the second half of July, layoffs recede.

The seasonal adjustments for initial claims assume a 14% increase in the number of new filers over the first two weeks of July and a 27% drop in the back half of the month. Of course, in 2020, most of the manufacturing sector was shuttered for a month or longer during the lockdowns, including the most prominent industry to feature the summer shutdowns, the automakers. As a result, there was no need for the plants to be closed again, no flurry of seasonal layoffs in early July, and no corresponding dive in the number of new filers later in the month.

While there may be other seasonal forces that remain in place, the largest driver of the big swings in the seasonal factors for initial claims was probably not applicable, and the factors themselves were arguably inappropriate.

While the degree of improvement in the labor market inarguably slowed in July from June, the unadjusted numbers offer a more accurate picture of the evolution of the labor market over the past month or two. The point here is not to argue that net hiring remains as robust as it was in May and early June. It clearly is not. However, the “Oh dear, initial claims are backing up. The economy is falling apart!” narrative that has been so prominent in the media and among less informed market participants—even some economists who failed to do their homework—over the past week or so is, at a minimum, overwrought, and potentially entirely misguided.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.