Uncategorized

Make way for more private CRT

admin | July 24, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

JPMorgan came to market this week with a transaction that combines legacy mortgage credit and unsecured corporate risk in a private credit risk transfer transaction. The deal presumably will provide the bank with potentially valuable regulatory and economic capital relief as it is substantially similar structurally to a deal the bank issued last fall. The novel nature of the reference collateral also potentially paves the way for private CRTs backed by not only different flavors of mortgage loans but other flavors of consumer loans as well.

Breaking down the transaction

The deal, CHASE 2020-CL1, is structurally similar to a transaction the bank issued last fall in that it uses a credit linked note (CLN) to transfer risk on a reference pool of mortgage loans. Investors buy par-priced notes that the sponsor can use to cover future losses on the reference pool. In turn, the sponsor pays investors in the notes a stream of interest to bear the credit risk of the pool.

While the deal is fundamentally akin to the mechanisms used by both Fannie Mae and Freddie Mac to transfer mortgage credit risk, there are some key differences.

- The notes are unsecured general obligations of JPMorgan Chase Bank, implying that both the principal and interest due to investors are unfunded, making the deal a hybrid of both residential mortgage and unsecured corporate credit risk.

- The deal also transfers roughly three times the amount of risk common to GSE credit risk transfer deals. GSE CRT deals generally issue notes where the junior-most tranche has a nominal amount of credit enhancement and the senior-most tranche is ‘BBB’, or roughly 4% of loss coverage. The CHASE deal transfers risk on the first dollar of loss through the first 12.5% of losses. The senior-most tranche in the structure is ‘AA’. Given the unsecured nature of the transaction, the rating on the senior-most tranche is capped at the corporate rating of the issuer. The ratings cap implies that the risk JPMorgan, or any bank for that matter, may choose to transfer may be more driven by regulatory capital efficiency than ratings, and the structure may only be viable for highly rated institutions that can issue investment grade unsecured debt at the top of the capital structure.

- The JPMorgan deal uses a pro-rata structure on the five mezzanine classes with a locked-out first loss Class B, which provides a floor to the credit enhancement on the deal. Assuming the reference collateral is passing certain performance triggers, the five mezzanine classes will receive both scheduled and unscheduled principal. The pro-rata structure potentially makes deeper mezzanine bonds more negatively convex than the 4-tranche sequential structure commonly used by the GSEs creating both potential positives and negatives for the investors. Investors deeper mezzanine classes will likely have less exposure to longer dated tail losses than they would in a sequential structure. Conversely, given the fact that the notes are par priced, uncapped LIBOR floaters, the pro-rata structure provides little opportunity for investors to benefit from roll down and subsequent total return from spread tightening as the deal seasons and deleverages.

- What looks to be another departure from GSE CRT is investors’ exposure to modification losses. In GSE CRT, once existing credit enhancement is depleted, investors will bear losses as a result of rate modifications in the form of interest shortfalls followed by principal losses to the junior-most outstanding tranche expressed as the difference between the original interest rate of the loan and the modified rate times the outstanding principal balance of the loan on a monthly basis. In GSE deals, all the losses associated with interest deficiencies would be allocated to the subordinate bonds. It appears that in the JP structure any deficient interest or WAC reduction would be shared pro-rata between the senior reference tranche and the mezzanine and subordinate notes and would reduce the interest on the junior-most bond by the amount of that pro-rata interest deficiency. For example, if the collateral experiences a $1,000 interest modification 12.5% of that modification loss would be passed through in the form of an interest shortfall of $125 to the B class of the deal.

- The key departure from last year’s transaction as well as GSE CRT is the pool of loans referenced in the deal. The current transaction references just over $2 billion in notional balance of modified Pay Option ARM negative amortization loans originated between 1986 and 2008 and likely acquired by JPMorgan through their purchase of Washington Mutual during the Global Financial Crisis. The transaction effectively marks a crossroads where new issue CRT technology is married to pre-crisis mortgage credit risk. All of the loans have been modified to fixed-rate coupons by JPMorgan or a prior servicer. In all likelihood, the majority of the loans were modified as part of the large scale mortgage servicer settlement that occurred in February of 2012 which JPMorgan was a party to along with Bank of America, Citigroup, Wells Fargo and GMAC/Ally.

Motivation of the issuer

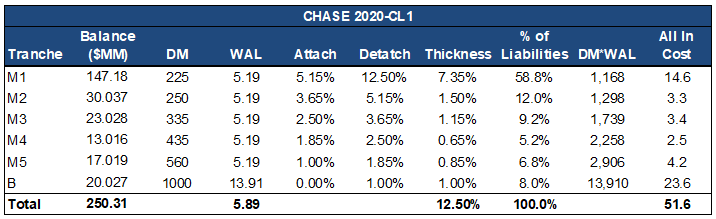

The primary motivation for the issuer appears to be an attempt to free up regulatory and economic capital on what can effectively deemed be non-core assets for the bank. To the extent that the bank was able to transfer risk at a level that is less than the cost of holding capital against these assets, it should likely pave the way for future transactions. Deriving the cost of insurance simply involves using the spread and WAL for each bond to derive the total spread paid out over the expected life of the transaction. That spread is then weighted by the portion of the reference pool that each tranche represents and divided by the weighted average life of the notes issued to get an annualized spread for each tranche. The cost of insurance on each tranche is then summed to derive the total cost of risk transfer. (Exhibit 1)

Exhibit 1: Calculating the cost of risk transfer – CHASE 2020-CL1

Source: Amherst Pierpont Securities

Based on this methodology, the estimated cost of risk transfer is 51 bp which looks to be a savings versus the cost of the risk-based capital associated with holding the whole loans. Assuming a 50% risk weighting and JPMorgan’s current Tier 1 leverage ratio of 14% implies the bank would have to hold 7% of regulatory capital against the position. At a current dividend yield of 9.6%, the bank would have to pay out 67 bp of dividend yield on the capital held against the position, potentially making the CRT a viable alternative for a larger swath of their loan portfolio assuming there is no residual economic or regulatory capital held against the position.

There may be additional benefits to the transaction for JPMorgan, although somewhat difficult to quantify. Given that the entirety of the pool has been modified at least once, the loans were flagged as Troubled Debt Restructurings (TDR)s and may have required some incremental capital or loss reserves held against them relative to always performing 1-4 family loans. However, given the pool has been clean pay for 36 months, the loans may not have still had any TDR designation associated with them. Additionally, while the loans have exhibited strong payment velocity, seasoned Pay Option ARMs have exhibited higher delinquency and forbearance rates than most other types of legacy collateral and the transaction likely affords JP Morgan protection against deterioration in borrower performance that would require them to increase potential loan loss reserves against the pool.

Projecting collateral performance

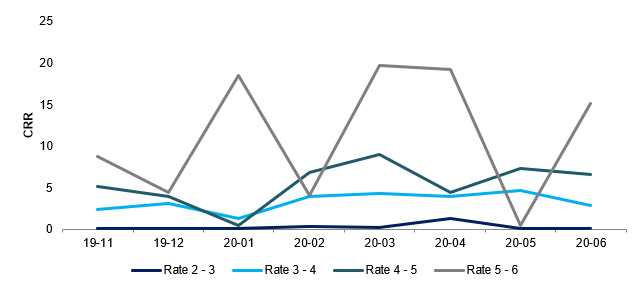

Despite a 36-month clean pay history and an average 4.2% gross WAC, the deal may prepay significantly slower than investors may expect. Looking at prepayment rates on post modified re-performing option ARM loans backing legacy WAMU trusts shows that loans with comparable WACs have prepaid recently in the range of 5 CRR in recent months. Additionally, it appears that if the sponsor were to refinance the loans and put them back on balance sheet they would lose the benefit of the initial risk transfer. While this would not be a deterrent to cross-servicer refinancing or borrowers proactively refinancing their loans, it may be a modest potential headwind to the sponsor soliciting refinances. (Exhibit 2)

Exhibit 2: WAMU re-performing POA have paid slow

Source: Amherst Insight Labs, Amherst Pierpont Securities

From a credit perspective, despite being seasoned negative amortization loans, the credit appears to be relatively pristine. The pool is 100% full documentation with a weighted average updated model FICO score of 742 and a mark-to-market LTV of 54. Comparing this pool to the credit performance of modified RPLs in legacy WAMU trusts with comparable mark-to-market LTVs suggests that default rates on the pool should be muted. However, the pool does not appear to be without tail risk as there is a considerable concentration of loans with current credit scores lower than 600 and a small amount of loans with current LTVs greater than 100.

The outlook for future issuance

The deal is clearly a milestone in terms of marrying CRT with off-the-run, non-core assets and its’ issuance certainly implies that JP Morgan’s prior transaction achieved their desired risk management and regulatory capital goals. With that said, the deal still maintains call language not dissimilar from their prior transaction which allows them to collapse the transaction if some regulatory ruling would render the transaction illegal or cause the bank to incur regulatory fines, so the deal appears to account for future regulatory uncertainty that would be a material deterrent to continued issuance. Absent that, it seems that banks may continue to look to capital markets solutions to reduce regulatory capital in the face of rising pandemic related loan loss reserves. And given Fannie Mae’s current pause in CRT issuance, private CRT may have an opportunity to fill the void in issuance to some extent.