Uncategorized

The Fed loads up on securities but little else

admin | July 10, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

It started looking likely a month ago that growth in the Fed’s balance sheet would fall well short of prevailing projections. The evolution of the balance sheet since then underscores the point. The only meaningful expansion is the ongoing purchases of Treasuries and agency MBS. Most other items have contracted or held steady, and the overall size of the Fed’s balance sheet has declined. Moreover, unless the Fed tinkers with the Main Street Lending Facility to make it more attractive to banks and borrowers, there may not be much growth going forward aside from asset purchases.

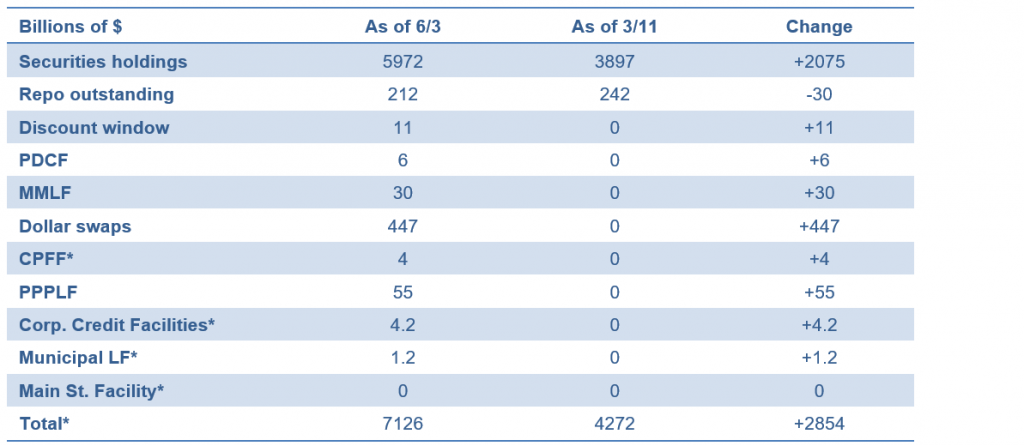

Balance sheet from start to peak

The Fed balance sheet has jumped by $2.8 trillion from the launch of QE on March 11 to the peak of Fed balances on Jun 3 (Exhibit 1). The bulk of the expansion came from Fed purchases of Treasuries and agency MBS. The next largest increase reflected dollar swaps used to provide dollar liquidity to overseas banks through their central banks.

Exhibit 1: Limited growth in the Fed balance sheet outside of securities

Note: * Figures for these categories exclude the equity capital supplied by Treasury to the Fed that backs these programs. Source: Federal Reserve.

The facilities created in response to the pandemic and its fallout generally had modest usage through June 3. At that time, however, the Municipal and Main Street Lending Facilities were just getting going, and there was still at least some hope that these programs would see substantial usage.

An update

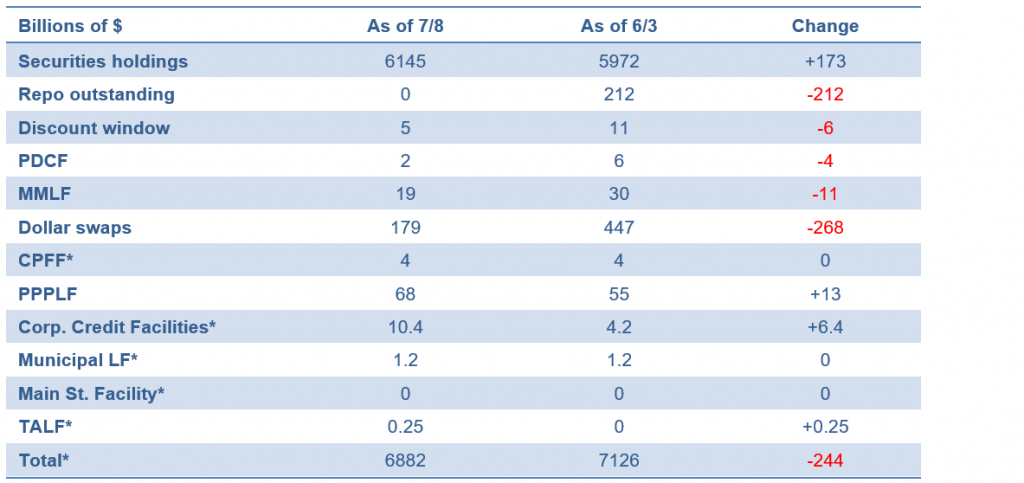

Since early June, the Fed’s balance sheet has been shrinking. Many of the programs that were created in the early days of the crisis to boost liquidity in markets have receded, as market functioning has returned to a more normal stance. Meanwhile, the Muni and Main Street facilities are not seeing much demand, and the Primary Corporate Credit Facility seems unlikely to get much interest either.

The Fed balance sheet has dropped by $244 billion since early June (Exhibit 2). The decline has been driven mainly by an unwinding of liquidity in the funding market. The NY Fed made the pricing of its repo offerings less attractive in June, reflecting the view that the market could stand on its own, and went from a major player to a last resort in the domestic repo market. In fact, as of last week, the Fed’s repo program has moved to zero take-up. Similarly, the central bank liquidity swaps outstanding has been cut by more than half over the past month, as 3-month swaps that were issued in the height of the funding crisis in March rolled off and were only partially replaced.

Exhibit 2: Federal Reserve Balance Sheet: Contraction

Note: * Figures for these categories exclude the equity capital supplied by Treasury to the Fed that backs these programs. Source: Federal Reserve.

In addition, other programs that rolled out in March to bolster liquidity, such as liberalized discount window borrowing, the PDCF, and the Money Market Mutual Fund Liquidity Facility have begun to recede noticeably. The CPFF has not had any new issuance since early May, and the CP in the program will be rolling off in a matter of weeks.

Meanwhile, the new lending programs that the Fed rolled out to support the economy more broadly are, for the most part, proving to be duds. The Fed is programmatically buying a small amount of investment grade corporate paper, but even that is now tapering down, since that market is doing quite well and does not need Fed support. The Fed had been buying about $1.7 billion per week, first in ETFs and then in individual bonds, but the head of the NY Fed markets desk publicly noted this week that the pace is likely to slow going forward and indeed, already did so in the latest week. The Muni facility did one deal with the State of Illinois and has done no more. The TALF is finally open, but there has been just $250 million done.

The program with the greatest usage at the moment is the PPP Liquidity Facility, which allows banks to repo out their PPP loans for cash. Even that program, however, declined for the first time in the latest week, and, in any case, usage should dwindle once the government begins to forgive the PPP loans.

Finally, there is the Main Street Lending Facility. A month ago, there were murmurings that the program might see surprisingly low usage, as the terms were not especially favorable. Now, we know. Only a few hundred of the 11,000 banks in the U.S. have registered to make these loans, and businesses are not very excited to tap the facility. It is too soon to write the program off entirely, and the Fed is likely at some point to tweak the terms to strengthen participation, but for now, Main Street is unlikely to be a source of notable balance sheet growth.

Balance sheet outlook

This description of the landscape allows for a more precise projection of the size of the balance sheet going forward. The FOMC locked in a $120 billion per month asset purchase pace—$80 billion in Treasuries and $40 billion plus rollovers in agency MBS—in June, which, if maintained through year-end, would add about $700 billion to the balance sheet. Corporate bond purchases could add another $10 billion to $20 billion. The only other potential major source of expansion would be Main Street Lending. Let’s say for the sake of argument that Main Street sees $100 billion in lending, which may prove generous. Meanwhile, central bank liquidity swaps and other liquidity programs, including the PPP liquidity facility, are likely to contract, perhaps by around $200 billion. That would put the Fed’s balance sheet at the end of this year at around $7.5 trillion, just a few hundred billion dollars above the June peak. To provide perspective on how much of a shift that is from earlier expectations, the April survey of Primary Dealers by the NY Fed found that the median estimate of the balance sheet size as of September 30, 2020 was close to $9 trillion.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.