Uncategorized

Lessons from asset returns in the second quarter

admin | July 10, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

After the Fed and fiscal policy reset market conditions in late March, credit has delivered a run of strong returns. It was a comeback from a dismal start to the year. Rates, by contrast, ran strong through March and weak afterwards. The shift in market conditions that drove those returns should carry the market well into 2021. That argues for going underweight rates, neutral MBS, overweight investment grade corporate and structured credit and very light on high yield corporate and structured risk.

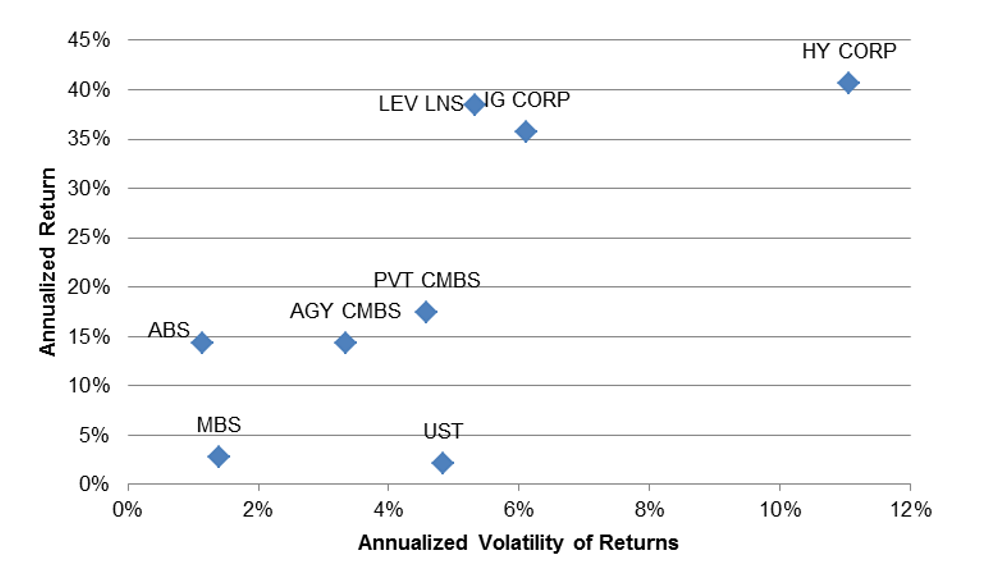

The last quarter saw both Fed and fiscal policy drive asset performance, with the Fed launching a major round of market support on March 23 followed four days later by passage of the CARES Act. Annualized returns on high yield (40.6%) and investment grade (35.7%) corporate credit along with leveraged loans (38.4%) led the market. Structured credit followed with good annualized returns in private CMBS (17.4%) and ABS (14.4%). Agency CMBS (14.3%) finished next, with the Fed’s other QE targets of agency MBS (2.7%) and Treasury debt (2.1%) trailing (Exhibit 1).

Exhibit 1: Returns on corporate and structured credit led rates in 2Q2020

Note: Based on daily returns measured by Bloomberg Barclays indices and the S&P/LSTA Leveraged Loan Total Return Index from 4/1/2020 to 6/30/2020. Source: Bloomberg, Amherst Pierpont Securities

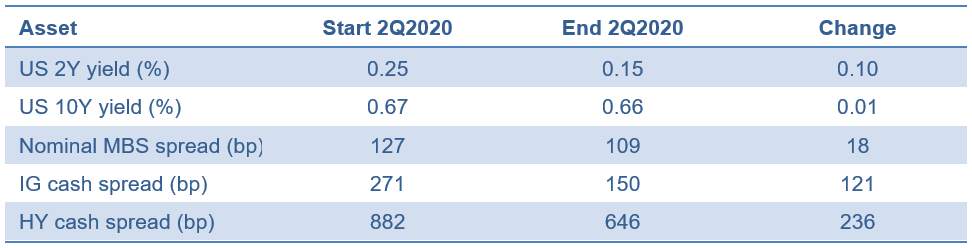

The returns reflected low and stable rates and steady spread compression, both echoes of the Fed’s post-2008 QE and forward guidance (Exhibit 2). The 2-year rate only dropped 10 bp through the second quarter and the 10-year by 1 bp, limiting price returns from lower interest rates. Most of the Treasury sector return came from coupons on outstanding issues. Agency MBS spreads tightened sharply in the days after March 23 but only tightened through the quarter by another 18 bp. The short effective duration on most MBS meant tighter spreads added little to returns, and the sector had to rely on payments from outstanding coupons for return. Investment grade corporate spreads tightened by 121 bp through the quarter, and, with an index duration of more than 10 years, the tightening added significant return. High yield tightened by 236 bp with an index duration of more than four years, giving high yield returns a big lift.

Exhibit 2: Low and stable rates, tightening spreads in 2Q2020

Source: Bloomberg, Amherst Pierpont Securities

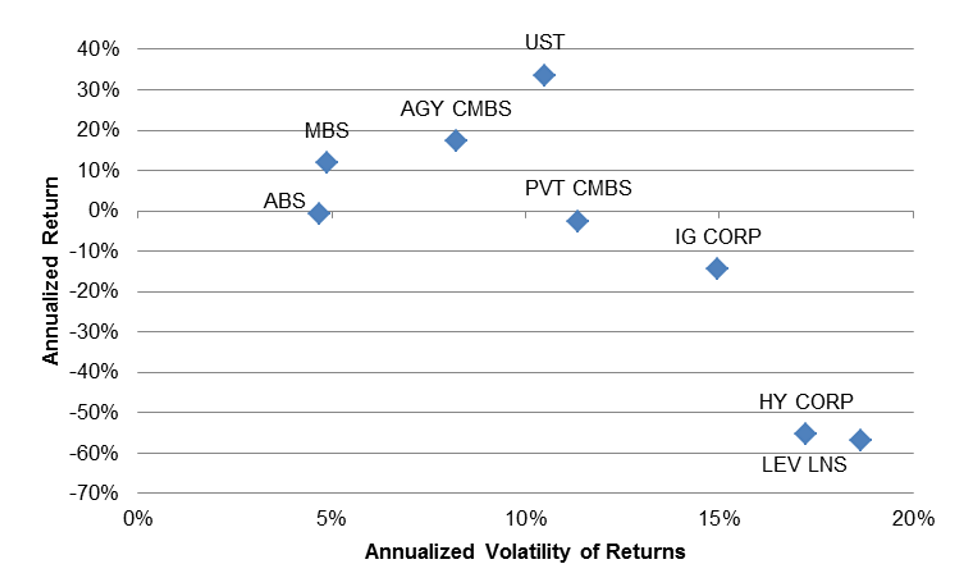

To put second quarter returns in context, they look very different in some ways and very similar in others to returns in the first quarter. As for the differences: corporate and structured credit started the year with annualized losses instead of gains. High yield (-56.8%) and leveraged loans (-55.3%) lost the most followed by investment grade corporate debt (-14.4%), private CMBS (-2.5%) and ABS (-0.8%). The strongest returns came from Treasury debt (33.6%), agency CMBS (17.4%) and agency MBS (11.8%). It was a picture of flight-to-quality. As for the similarities: high yield showed the most return volatility in both quarters, investment grade corporate debt along with Treasuries and CMBS showed intermediate volatility in both quarters and ABS and MBS showed consistently low volatility (Exhibit 3).

Exhibit 3: To start 2020, corporate and structured credit lagged rates

Note: Based on daily returns measured by Bloomberg Barclays indices and the S&P/LSTA Leveraged Loan Total Return Index from 12/31/2020 to 3/31/2020. Source: Bloomberg, Amherst Pierpont Securities

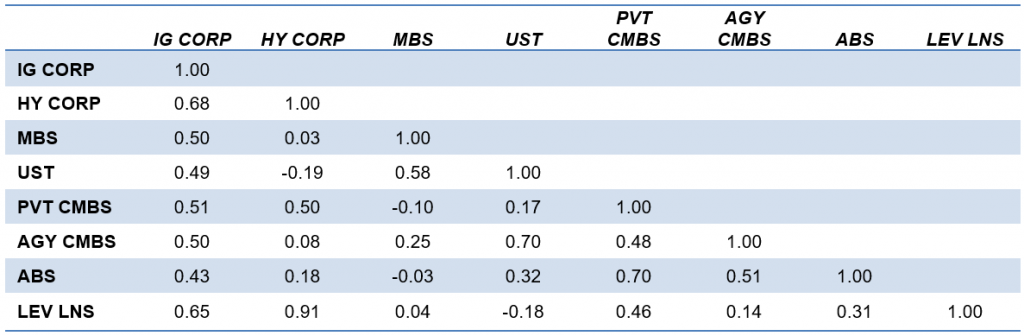

The other aspect of performance worth noting is the correlation of returns, where differences in rate and spread exposure create some diversification. The most notable, which is consistent with earlier periods, is the slight negative correlation between performance on credit and rates. That is highlighted by the negative correlation between high yield and loans and Treasury debt (Exhibit 4). Rates and credit diversify one another.

Exhibit 4: Slight negative correlation shows rates and credit diversify one another

Note: Based on daily returns measured by Bloomberg Barclays indices and the S&P/LSTA Leveraged Loan Total Return Index from 12/31/2020 6/301/2020. Source: Bloomberg, Amherst Pierpont Securities

The differences between first and second quarter returns highlight factors likely to persist into 2021 and longer and continue driving asset performance:

- Low and steady rates, especially in shorter maturities. Fed QE and forward guidance should keep rates low and stable through 2021, although the curve should bear steepen over time as the mix of economic recovery and stimulus raises concerns about inflation. This should make it hard for Treasury debt to outperform other assets, especially longer debt most vulnerable to a bear steepening curve.

- Steady spread compression. QE by design takes safe assets out of the market and forces investor into neighboring but riskier assets. The Fed’s $80 billion in monthly purchases of Treasury debt and $40 billion monthly increase in MBS balances will give it a rising share of the outstanding market. The Fed’s potential to buy up to $750 billion of 5-year and shorter corporate debt would give it an important share of the investment grade market. Spreads in MBS and investment grade corporate and structured credit should continue tightening. The much longer spread duration of most credit, however, should lead the sector to outperform MBS.

- The risk of high volatility in leveraged credit. Even though high yield debt and leveraged loans should get a lift from spread compression, the downside from fundamental weakness in the economy is much larger than the upside from tighter spreads. The recent performance of high yield makes the case: up an annualized 40.6% in the second quarter, but only after losing an annualized 56.8% in the first. The International Monetary Fund’s recent economic projections highlighted the greater downside than upside for now in projected GDP, which would feed directly into the performance of high yield and leveraged loans. Congress and the White House look likely to pass another round of fiscal stimulus. That should buffer some of the downside, but not all of it.

The lessons from asset performance so far this year and from the factors most likely to shape performance at least through the rest of the year have clear implications for asset allocation:

- Underweight Treasury debt for its low likely returns into 2021 and moderate volatility

- Neutral weight agency MBS for its modest likely returns into 2021 and relatively low volatility, and instead add performance through agency, sector, coupon and specified pool selection all possibly leveraged in MBS derivatives

- Overweight investment grade corporate and structured credit for its relatively high return from carry and spread tightening, return sufficient to compensate for relatively high volatility. My colleagues Dan Bruzzo and Meredith Contente offer corporate credit sector recommendations elsewhere in this issue to help add return.

- Underweight high yield corporate and structured credit, where return downside outweighs upside for now. That imbalance could change by the end of the year when colder weather forces more people inside and makes the course and timing of the pandemic clearer.

* * *

The view in rates

The Fed’s dots, fed funds futures and OIS all price a Fed on hold through 2022, with futures and OIS pricing a small chance of negative rates in 2021. The current 0.59% rate on 10-year Treasury debt implies an average real rate of -80 bp and inflation of 140 bp. Real rates have generally continued to fall and Implied inflation has continued to climb since mid-March. That should keep pressure on the yield curve to steepen from 2-year to 10-year and from 5-year to 30-year. So far, the steeping from 5-year to 30-year has outpaced the shorter part of the curve. This is a replay of the rate impact of previous episodes of QE.

The view in spreads

Portfolio balances at the Fed, banks, and money market funds have slipped since early May although lately fixed income ETFs and mutual funds have sizable amounts of money to spend. Demand from these quarters for high quality assets should keep squeezing spreads tighter. As spreads tighten in the highest quality assets, investors will have to move to the next tier of higher risk to get sufficient spread, but it is likely to happen. Spread compression across rating categories or credit quality is highly likely. There is fundamental risk in the most leveraged corporate balance sheets, and only there might spreads continue lagging the rest of the market.

The view in credit

The downside in leveraged credit outweighs the upside for now. Beyond the current uptick in Covid-19 in the US, the arrival of the school year in the next two months should create an important test of the ability to safely assemble people indoors. If that proves difficult, then potential productivity and growth should fall. Many investment grade companies have stockpiled enough cash to survive protracted slow growth, but highly leveraged companies and consumers are at risk. Prices on some sectors of leveraged loans, rating agency downgrades in leveraged loans and high yield and rising bank loan loss reserves signal a wave of distressed credit. Rising unemployment and delinquency rates in assets from MBS to auto loans show pressure on the consumer balance sheet. However, monetary and fiscal policies are both shoring up these fundamentals for now. The course of leveraged corporate and consumer credit also depends on renewal of CARES Act unemployment benefits and support for small businesses, along with moratoriums on eviction and foreclosure.