Uncategorized

A welcome slowdown in multifamily forbearance

admin | June 26, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

The pace of multifamily loans entering forbearance has slowed dramatically in June after surging in April and May. The proportion of tenants struggling to pay rent due to the economic impact of the crisis has also started to show modest improvement. The complicating issue now could be one of timing, as the first multifamily borrowers who entered agency forbearance programs in April are expected to start paying their loans again in July. Supplemental unemployment benefits, which have allowed many tenants to continue paying rent, are set to expire on July 31. If the economic rebound is vigorous and sustained, this mismatch should cause minimal issues. If the economic rebound sputters, additional government support and an extension of forbearance programs will likely be required to prevent a rapid transition from forbearance into default.

Timing the transition for borrowers and tenants

Forbearance periods and eviction protection for multifamily tenants established under federal powers in March were set as 120 days from enactment of the CARES Act; these protections expire at the end of July. Tenants in buildings where the borrower has entered into a forbearance agreement with one of the agencies can request extended rent forbearance through the period of the borrower’s loan forbearance. Given that the bulk of multifamily borrowers entered forbearance agreements in April or May, those 90-day terms will be up either at the end of June or July, assuming the forbearance period is not extended under the agreement. Borrowers will therefore be expected to begin remitting full payments on their loans and curing the forborne amounts as of the July or August payments.

Tenants who have been granted forbearance under the federal program should resume paying rent in August, and ostensibly begin curing the forborne rent. Many states and municipalities have extended tenant forbearance and protections from evictions due to COVID-19 for longer periods of time, putting additional pressure on multifamily property owners.

Based on the Household Pulse Survey conducted by the US Census, the percentage of renters who have not paid or deferred rent is beginning to fall modestly, improving from 17.8% to 16.1% week over week in mid-June. However most of these tenants have not yet returned to work or continue to work fewer hours due to the pandemic. Supplemental unemployment benefits of $600 per week are also scheduled to terminate on July 31 unless the program is extended by Congress.

A slowdown in multifamily loans entering forbearance

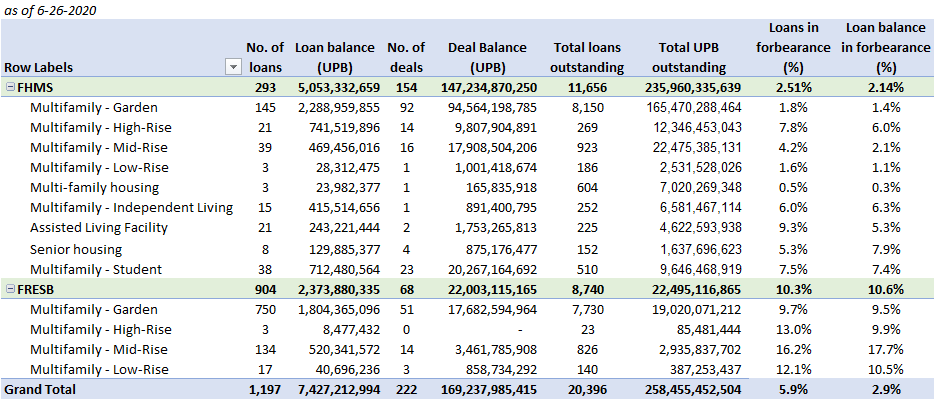

Freddie Mac’s multifamily forbearance rolls due to COVID-19 climbed by 170 loans in June to just shy of 2,000 total loans with unpaid principal balance (UPB) of $7.4 billion, up from $6.2 billion in May (Exhibit 1). This brings the percentage of loans in forbearance to 2.9% of Freddie Mac’s multifamily book outstanding across the FHMS and FRESB shelves. New loans entering forbearance continued to be heavily represented by the small balance loan (FRESB) program, which had 127 new loans in forbearance compared to 43 new loans from the FHMS shelf.

Exhibit 1: Freddie Mac multifamily loans in forbearance

Note: FHMS totals include all progams, with some non-core property subtypes (other, health care, medical office / assisted living, cooperative and mixed use) excluded if there are no outstanding loans in forbearance. FRESB totals include all property subtypes, though several (independent living, student, and senior) are small and have no outstanding loans currently in forbearance. Defeased (FHMS) and prepaid (FRESB) loans are also excluded in the total loan numbers and total balances. Defeased and prepaid loans are not excluded from the deal balance numbers. If deal balance is zero those loans are included in a deal that has other loans in forbearance to avoid double-counting. Data is as of May 2020. Source: Bloomberg, Intex, Amherst Pierpont Securities.

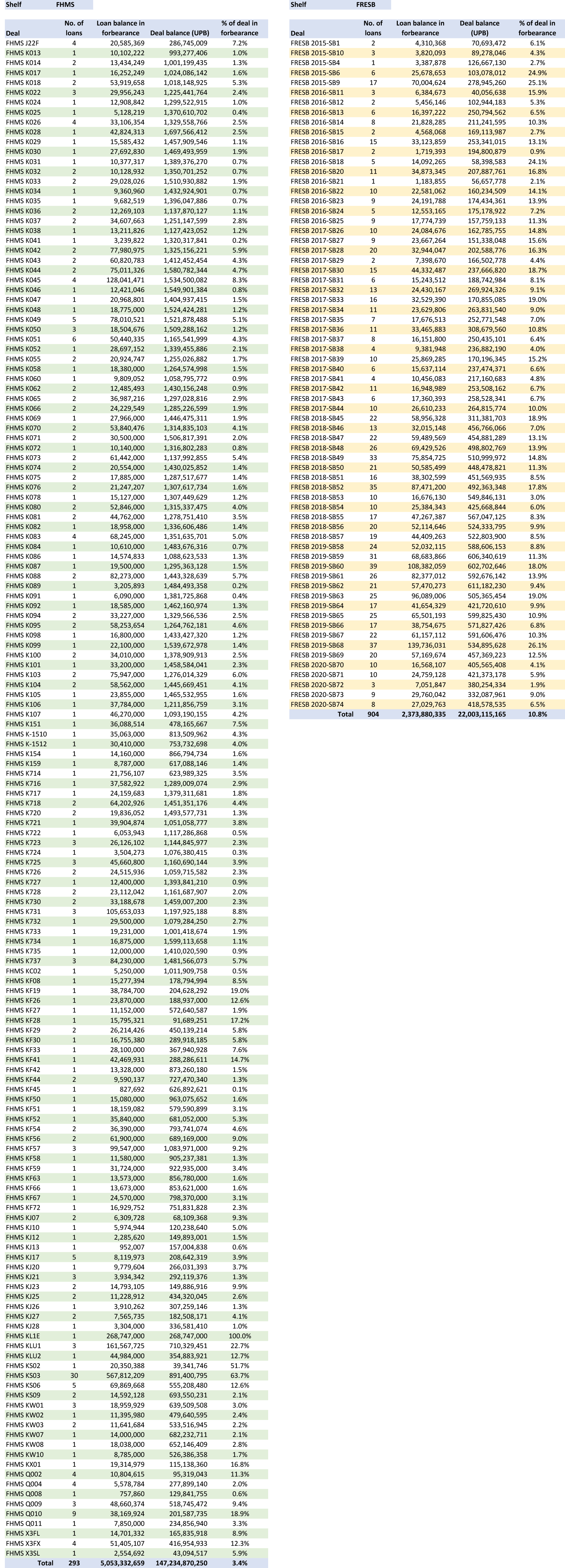

The number of K-series deals with loans in forbearance climbed to 154, up from 139 in May. Non-standard K-series deals continue to struggle most, with seniors deals (KS), lease-up (KLU), Q and floating rate series (KF) often having 15-20% or more of the balance in forbearance (Exhibit 2). There are a few standard K-series deals where the % of the deal in forbearance is close to or above 7.5%, which exceeds the attachment point for losses of the C mezzanine tranche. There is no expectation that all loans in forbearance will default, and certainly not all default with 100 loss severity. However, mezzanine tranches for those deal are likely to reflect the high levels of forbearance in the price. There are 68 FRESB deals with loans in forbearance, with 10.7% of the balance of these deals in forbearance on average. There are several FRESB deals with 25% of the loans in forbearance.

Exhibit 2: Freddie Mac multifamily deals with loans in forbearance due to COVID-19

Source: Freddie Mac, Bloomberg, Amherst Pierpont Securities

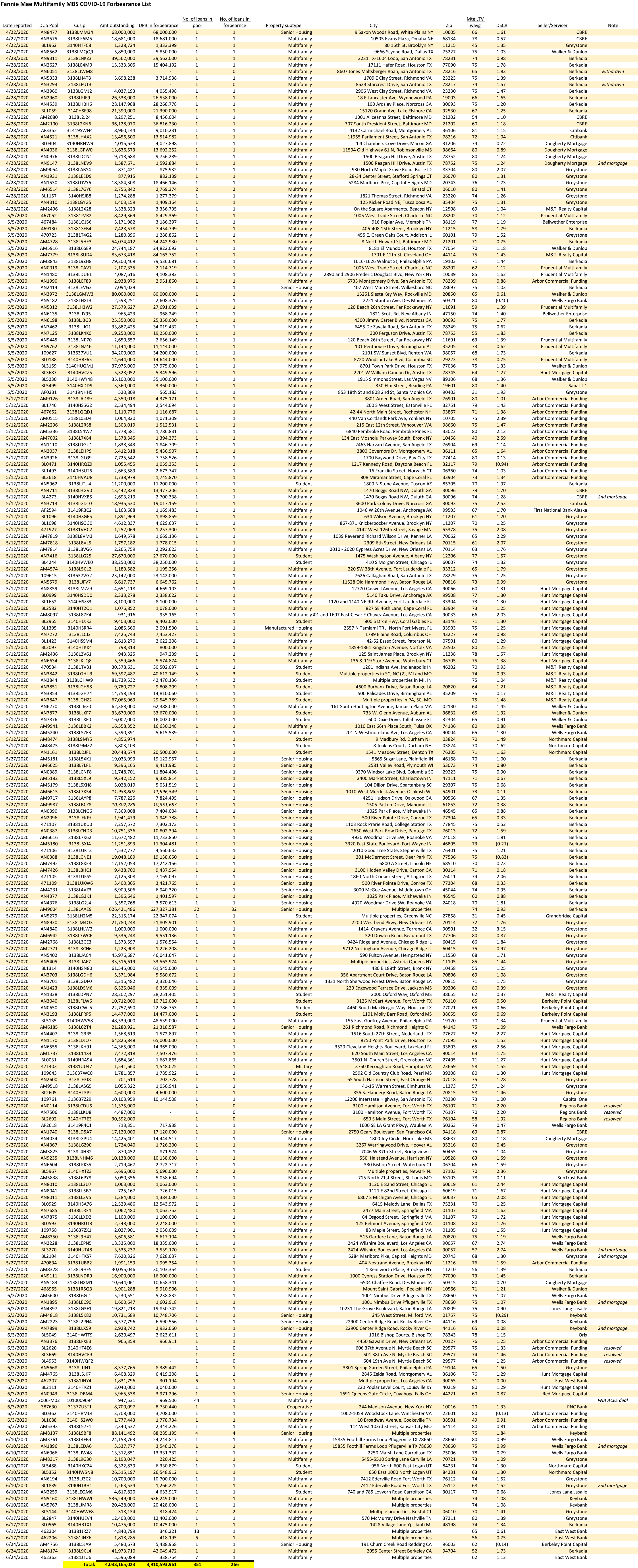

This slowdown mimics that seen at Fannie Mae, where only a handful of loans have entered forbearance over the past two weeks (Exhibit 3).

Exhibit 3: Fannie Mae multifamily loans in forbearance due to COVID-19

Source: Fannie Mae, Bloomberg, Amherst Pierpont Securities

The peak of forbearance has hopefully passed, and the speed and strength of the recovery may allow both tenants and borrowers to meet their obligations going forward.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.