Uncategorized

New issue spreads tighten to pre-pandemic levels

admin | June 19, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

New issue spreads in agency CMBS are trading through pre-pandemic levels and are hovering near all-time tights. This is due to two factors: the lower, steeper yield curve has led to considerable spread tightening and compression across guaranteed classes of varying durations; and the Fed’s agency CMBS buying operations have been so successful supporting the market that the purchase amounts have rapidly declined.

New issue agency multifamily pricing close to all-time tights

The new issue agency CMBS market, anchored by Freddie K-series, has seen spreads begin to approach all-time tights after blowing wider in the middle of March (Exhibits 1 and 2).The peak spreads for new issue was the FHMS K-106 deal which priced on March 17th, when the agency CMBS OAS index was hitting 100 bp, still close to 60 bp below the wides it would touch the following week.

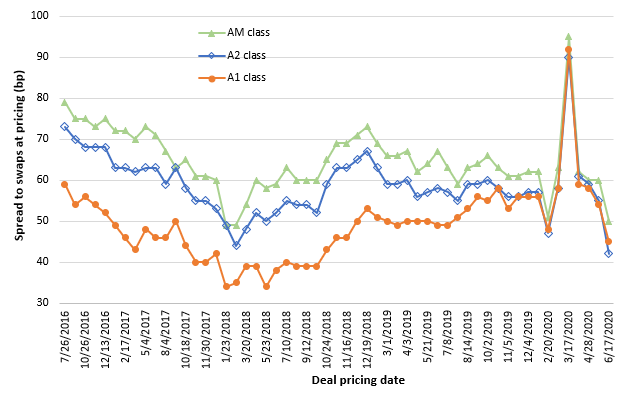

Exhibit 1: Freddie Mac K-deal spreads at pricing, guaranteed classes

Note: Includes standard collateral, 10-year fixed coupon K-deals only. Source: Bloomberg, Freddie Mac, Amherst Pierpont Securities.

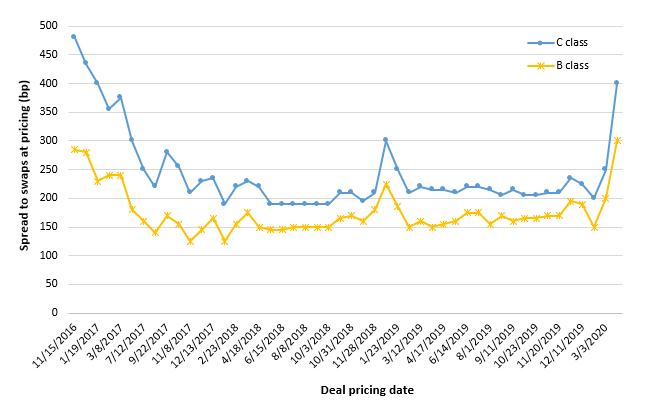

The guaranteed A1, A2 and AM classes of the K-106 deal priced at 90, 92 and 95 bp, respectively, while the unguaranteed B and C classes priced at 300 and 400 bp over swaps. By early April the GSEs introduced forbearance plans for single family and multifamily borrowers and the market remained exceptionally skittish about taking on credit risk. Freddie Mac began passing on issuing mezzanine securities in their K-deals in early April in favor of wrapping the collateral into the AM class and increasing the guarantee fee. Since then Freddie has temporarily suspended mezzanine issuance in K-deals, possibly due to the FHFA’s newly proposed capital rules that were published on May 20th.

Exhibit 4: Freddie Mac K-deal spreads at pricing, unguaranteed mezzanine classes

Source: Bloomberg, Freddie Mac, Amherst Pierpont Securities

Lower rates, a steeper curve and the whole panoply of Fed and government programs aimed at easing the economic and market stress due to the pandemic has brought a sense of normalcy back to the market. New issue agency CMBs are coming within a few basis points of all-time tights. The latest K-110 deal which priced on June 17th saw the benchmark A2 class with a WAL of 9.7 recently price at 42 bp, which was 3 bp inside of the A1 class with a WAL of 7.2. This deal had a slightly smaller collateral balance in the A2 class – 68% of collateral compared to a recent average of 73% – and a somewhat larger allocation of over 12% to both the A1 and AM, which on average have 8.3% and 5.1% of the deal balance. The market will continue to sort out how much the liquidity premium is worth in the A2 class and whether investors will migrate to the AMs, and in some cases the A1s, to pick up additional yield.

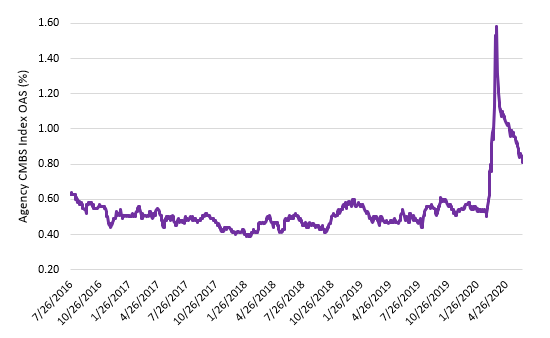

The spreads of agency CMBS had been fairly stable for the last several years up until the pandemic broke in early March (Exhibit 3). Spreads peaked in late March during the week of March 23rd – March 28th, with the OAS of a broad market agency CMBS index touching just below 160 bp. The Fed announced on Monday, March 23rd that it would begin buying unlimited amounts of Treasuries, agency MBS and agency CMBS to support the markets, and bolstered that with a range of other credit facilities and lending programs to support business owners and markets.

Exhibit 3: Agency CMBS spreads widen then broadly recover

Note: Bloomberg Barclays Agency CMBS OAS index. The index includes bonds from several types of Freddie Mac K-series incorporating both guaranteed (heaviest weights on A2 classes with some A1, A3 and AM bonds) and mezzanine classes (both B and C), and bonds across classes of Fannie Mae Aces deals. The duration of the index is 5.66 years and there are 786 bonds currently in the index. Source: Bloomberg, Amherst Pierpont Securities.

The agency CMBS index has since broadly recovered, but still remains wide of pre-pandemic levels primarily because over 5% of the bonds in the index are the B and C mezzanine tranches of Freddie K-deals. These unguaranteed classes are part of the credit risk transfer program and function as loss absorbing capital in the unlikely event that losses were to exceed 7.5% of collateral, which is covered by the D subordinate class. The C class would absorb losses from 7.5% to 10%, then the B class would absorb any additional losses between 10% and 14% of the collateral underlying the deal. The surge of multifamily loans in forbearance has resulted in the B and C bonds remaining under some pressure until it becomes clearer what the trajectory of the economic recovery will be and how it will ultimately impact these multifamily borrowers.

Fed agency CMBS operations provided essential support

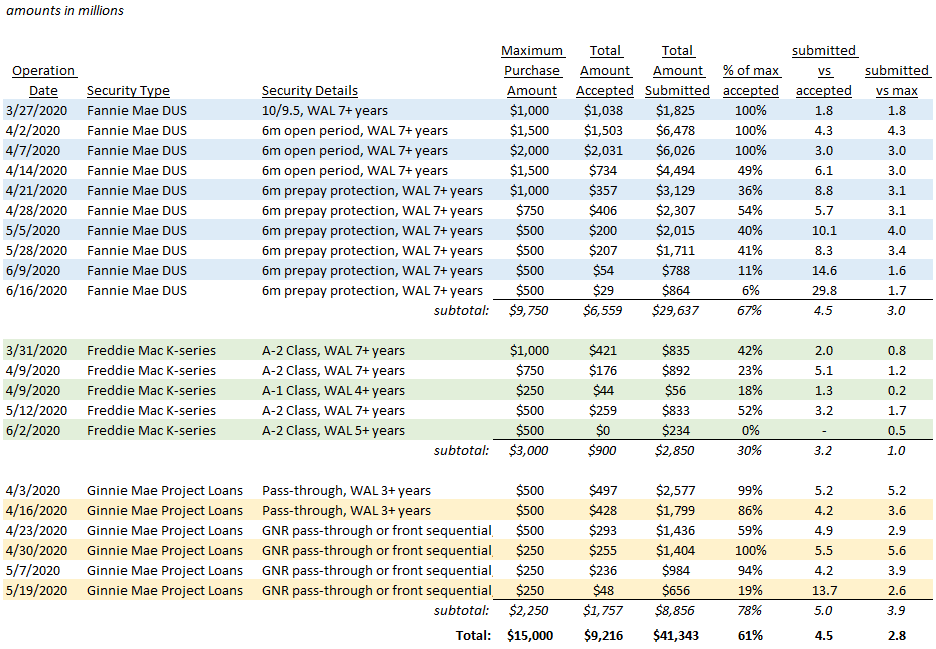

The Fed’s agency CMBS operations provided critical support that enhanced liquidity, took pressure off of dealer balance sheets and began to normalize spreads. The buying operations were across three multifamily products: Fannie Mae DUS pools, Freddie Mac K-series, and Ginnie Mae project loans. The first operation took place on Thursday, March 27th, when spreads peaked at 158 bp, and was for $1 billion of Fannie Mae DUS pools (Exhibit 2). There is a 3 to 5 bp financing advantage to Fannie Mae DUS pools and Ginnie Mae project loan pools over securitized Freddie Mac K-series, so these tended to be popular instruments for leveraged investors, including hedge funds and mortgage REITs. Similar to the crisis in 2008, though on a much smaller scale, the dramatic increase in financing costs and haircuts applied to collateral forced many leveraged investors into liquidation and their agency CMBS holdings, among others, flooded the street and dealer balance sheets.

Exhibit 3: Fed agency CMBS operations

Source: Federal Reserve Bank of New York, Amherst Pierpont Securities

The Fed’s buying operations in DUS and project loans became heavily oversubscribed, and the Fed twice increased its maximum purchase amount in DUS to $2 billion at the peak in early April before tapering them down as the liquidity and credit crisis began to subside.

By contrast the buying operations in Freddie K-series seldom saw the volume of bids submitted reach the maximum purchase size of the operation, and at each operation the Fed purchases were well below the potential size. In fact, the Fed completely passed on buying any securities during most recent Freddie K operation on June 2nd, perhaps because it did not want to bid at or through market levels to buy a smattering of bonds. Based on how well the market has recovered for agency CMBS and Freddie K-series in particular, its likely the Fed won’t schedule any new purchase operations in that sector.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.