Uncategorized

Looking for upside surprise from the consumer

admin | June 19, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Consumer spending is central to the US economy as it represents roughly two-thirds of GDP. In recent months, the consumer has become even more pivotal. Lockdowns led to a drastic drop in consumer activity in March and April and the gradual reopening has already led to a dramatic improvement in retail sales for May. Further gains are likely in June, though the quarterly decline in the second quarter will still be catastrophic. Beyond June, the consumer looks likely to continue delivering upside surprises.

May retail sales

The recently-released May retail sales report showed a much stronger-than-expected rebound in May after April’s record drop (Exhibit 1). The figures backed up anecdotal reports and high-frequency data on credit card swipes and mobility that pointed to a robust pickup in consumer activity after April’s lockdown-imposed doldrums.

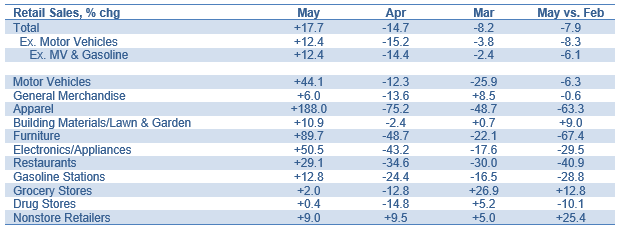

Exhibit 1: May Retail Sales

Source: Census Bureau

The breakdown by category shows that nonessential stores, the ones predominantly closed in late March and April, saw the biggest rebounds in May. Apparel outlets offer the most extreme example. This category suffered through a nearly 90% drop in sales in March and April. In that context, the 188% rebound in May, as impressive as it sounds, still left the May level of sales down over 63% from the February reading. Furniture and electronics and appliance stores also saw big gains in percent change terms, but sales remain far below normal. On the other side of the spectrum, sales at grocery stores, nonstore retailers, and building materials outlets were higher in May than in February.

Auto dealers fall in between the two extremes. Relative to expectations, auto sales have held up much better than feared back in March and April. The May retail sales tally for motor vehicle dealers was only 6% below the February level, though unit sales still have much further to go, down by more than 25% from February with part of that gap reflecting a collapse in fleet sales mainly by rental car companies.

Retail sales only measure goods purchases with one exception: restaurants. Restaurants have only been able to open on a limited basis due to social distancing. Thus, the category enjoyed a sizable bounce in May but remained over 40% below the pre-COVID pace of sales. This offers a window into how some services components may perform in May.

May consumer spending

Retail sales figures point the way to a detailed forecast for overall May consumer spending. The contours of the goods pieces largely reflect the retail sales figures, with autos rebounding sharply, gasoline lagging due to price drops—which will reverse to a degree in June—and other goods posting a double-digit advance.

Within the services sector, the restaurant figures from the retail sales report and high-frequency data on other types of service providers offer insights into the May performance. Services categories illustrate that there were divergent impacts from the lockdown across sectors. Housing services, utilities, and communications were essentially unaffected, and financial services, education, and professional and business services only saw modest declines due to the lockdowns. In contrast, restaurants and hotels, transportation (air travel), personal care (hair and nail salons), and recreation were crushed. Ironically, health care services also dipped sharply, as doctors’ and dentists’ offices were closed and many hospitals sat empty in parts of the country not hit hard by COVID early on.

May should be a mixed bag. Restaurants rebounded substantially and health care outlays also likely bounced sharply, as people addressed pent-up medical needs. In contrast, many states have been slow to reopen some types of activity, and spending for personal care services, transportation, and recreation may only rise modestly from depressed levels.

Look for a 5.2% increase in services outlays in May, which would restore about 20% of the losses recorded in March and April. Such a result for the services sector would likely lead to a gain for overall consumer spending of about 7.5% in May, retracing about half of the April plunge and just over 30% of the combined March-April drop.

June consumer spending

Looking ahead to the current month, motor vehicle sales probably continued to recover, approaching pre-COVID levels. Gasoline station receipts undoubtedly surged, reflecting both an increase in driving and a rebound in pump prices. The rest of the goods sector likely increased but at a much slower pace than in May. Still, the advance ought to be substantial, as June is the first month when nonessential stores would have been open for a full month in most states.

On the services side, some of the sectors that were slow to recover in May should see a more substantial bounceback, including hotels and personal services. Restaurants also likely enjoyed another sharp rise. Other sectors, such as air travel and recreation, may have remained depressed.

Look for consumer spending to rise by another 5% in June. That would put the level of outlays still far below the pre-COVID pace. In fact, it would mean that the May-June rebound retraced just over half of the March-April drop.

Quarterly readings

These projections for May and June would yield a quarterly drop of almost 38% annualized for real consumer spending in the second quarter despite the sizable bounce back in May and June. Nonetheless, the fact that the June level would be well above the quarterly average sets the stage for a powerful increase in the third quarter. Assuming further but decelerating gains over the summer, real consumer outlays in the third quarter look set to bounce by an annualized 45%.

These estimates seem reasonable, not overly aggressive. Nonetheless, it likely lands on the sunny side of the consensus, particularly for the third quarter. The second quarter projection is actually not very far from consensus. Prior to the May retail sales report, the median forecasts in the Bloomberg monthly survey called for a 40% annualized drop in real consumer spending. However, the median forecast for the third quarter was a 25% annualized gain.

On its face, a 25% annualized rebound seems plenty aggressive. However, when you do the arithmetic, up 25% is actually extremely conservative. The projections here for May and June would put the June level so far ahead of the second quarter average that flat monthly readings for July, August, and September would yield nearly a 24% annualized third gain. Flat monthly performances in the summer strike me as exceedingly pessimistic, as air travel and several other categories will be slowly but surely ramping back up.

This arithmetic constitutes a key underpinning of an outcome likely since the early days of the pandemic lockdowns – that the consensus was too conservative about the third quarter rebound in GDP growth. Consensus forecasts have risen somewhat but remain substantially too gloomy for the third quarter. To be sure, consumer spending by the end of the summer will still be substantially below pre-COVID levels, but upside surprises from the consumer relative to the consensus will likely continue beyond the May retail sales report.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.