Uncategorized

Yield pick-up available in off-the-run paper as new issuance surges

admin | May 29, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

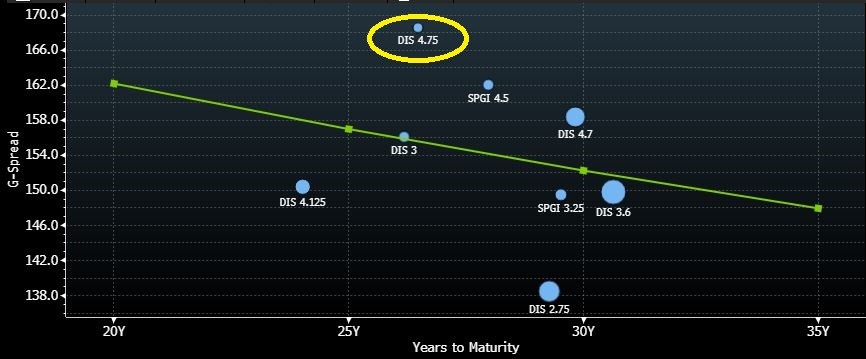

The influx of new issue activity has resulted in some off-the-run bonds being overlooked, particularly in the long end, where there are now opportunities for attractive yield pick-up. In high quality paper, the DIS 4.75% 11/15/2046 (New Disney notes) is a good buy candidate given the g-spread pick up relative to other DIS long bonds.

The DIS 4.75% 11/15/2046 is currently 19 bp g-spread behind the newly issued DIS 3.6% 1/13/51 bonds. These bonds also offer a considerable spread pick-up to other similarly dated off-the-run DIS issues, including the DIS 4.125% 6/1/44 and DIS 3.0% 7/30/46 bonds (19 bp and 13 bp, respectively). While all the aforementioned DIS issues are index eligible, the DIS 4.75% 11/15/2046 bonds have the smallest notional outstanding of roughly $400 million.

Exhibit 1. Single A – Media 30-year curve

Source: Bloomberg; APS

Debt Exchange and Capital Structure

As part of the June 2018 amended merger plan, The Walt Disney Company (TWDC) and 21CF became wholly owned subsidiaries of the New Disney (DIS – A2/A- (*-)/A- (n)). The New Disney is the parent and will be the issuing entity going forward. The New Disney and the existing TWDC debt will be unconditionally cross guaranteed. In an effort to simplify its capital structure, DIS conducted an exchange for any and all 21CF bonds ($18.13 billion) into New Disney notes. Participation was high in the exchange with the majority of tranches achieving a 95% or higher participation rate. Notably the 21CF debt that was not exchanged does not benefit from the aforementioned cross guarantee structure and is located under the TFCFA ticker. As such, Moody’s withdrew its ratings on the remaining TFCFA debt.

Given the cross guarantee structure of the TWDC and the New Disney notes, there does not need to be such a large trading differential between the different entities. In cases where debt is assumed but not guaranteed, large trading differentials are common. Even different operating subsidiaries could warrant trading differentials given the underlying assets of each subsidiary. However, in this case, an unconditional cross guarantee structure means that while the operating subsidiary may be in a better asset position to the parent, the cross guarantee limits the trading differential due to the equalized ratings. As an example, the Comcast Corp and NBC Universal paper (both A3/A-/A-), which also are cross guaranteed, have historically traded only 5 bp apart.

Dividend Suspended in an Effort to Preserve Ratings

As DIS continues to be negatively impacted by the pandemic, the company was downgraded by S&P to A- with its ratings still on review for a downgrade. S&P’s rating action was largely based on their estimate that leverage will increase well above 3.0x for the next two years. S&P does not foresee leverage falling below 3.0x until fiscal 2022, as they believe theme parks are not likely to return to normal capacity utilization rates until long after stay at home orders are lifted. While the company has shored up liquidity and addressed upcoming debt maturities with its two recent bond deals, S&P will look to resolve its credit watch only after it can assess the rate of return to theme parks as well as any long term negative affects to the company’s out of home entertainment business. Management did take a bold step by suspending its July 2020 semi-annual dividend, which will save $1.6 billion from being paid to shareholders. The suspension not only helps to modestly improve net leverage, but demonstrates management’s commitment to both reduce leverage and to its current ratings.

The New Normal

While DIS reopened its Shanghai theme park on 5/11/20, the Chinese government has placed restrictions on capacity, limiting it to one-third. Currently, the park is welcoming 20,000 guests per day which is roughly 25% of capacity. DIS announced earlier this week that it will be looking to open Magic Kingdom and Animal Kingdom on 7/11/20 with Epcot and Hollywood Studios to follow on 7/15/20. Capacity will be limited by the company to less than 50%. A new reservation system will be added for entry into the parks, ending the ability for guests to walk up and buy a ticket. Temperature checks and face masks will be mandatory. Seats on rides will be purposely left empty to adhere to social distancing rules and parades and fireworks displays will be on hold to limit crowds. Menus will be disposable to limit cross contamination.

While there is limited visibility into what type of capacity the theme parks need to operate at to turn a profit, the cash drain of opening them at a reduced capacity is less than keeping them closed all together. To that extent, DIS expects the reopening to be a “positive net contribution” to the parks business. Furthermore, DIS does not plan to offer discounted tickets to bring back guests to the park as they believe there will be enough demand for the limited reservation slots.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.