Uncategorized

Bank stock sell-off: time to panic or hold tight?

admin | May 15, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

US bank stocks have been in rapid decline, with heavy selling over the past week. Equity investors have grown increasingly wary of the likely inevitable cuts to shareholder payouts, and the prospect that a deeper US economic recession will result in lower-for-longer rates. Despite the spike in stock price volatility, domestic bank credit has remained steady, with spreads little changed over the past week. Bond investors should continue to maintain an overweight in domestic bank credit, and look at add exposure if any equity-related selling spills over into corporate debt markets.

Since the early weeks of the COVID-19 crisis we have been stressing an overweight on domestic bank credit with an emphasis on the big US money center banks (APS Strategy: adopt-defensive-posture). This point was further emphasized during heightened volatility (APS Strategy: remain-defensive) and highlighted as the banks reported 1Q20 earnings (APS Strategy: Bank Earnings) with sizable provisions for current and future credit costs.

Exhibit 1. Bank Stock Returns (4/29 – 5/14) vs S&P 500

Source: Bloomberg LP

Bank stock selling took a pause on Thursday, as reports of a rumored tie-up between Goldman Sachs (GS: A3/BBB+/A) and Wells Fargo (WFC: A2/A-/A+) surfaced, fueling some speculative relief in bank stocks, but ultimately leaving valuations significantly lower from late April (although it’s not the topic of discussion here, the prospects of a GS/WFC tie-up are extremely dim from a regulatory perspective; politically indefensible).

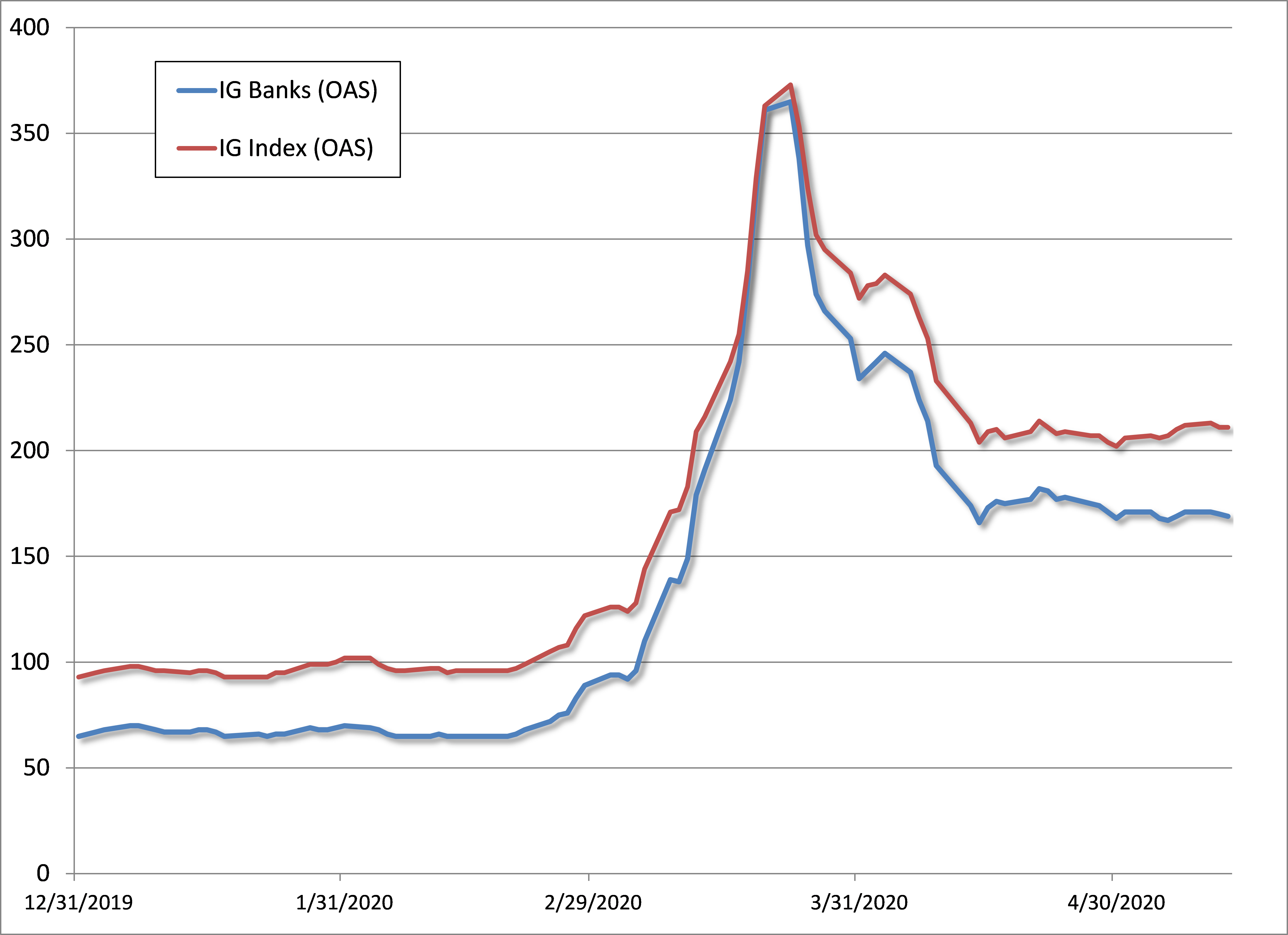

Exhibit 2. Banking OAS vs Broad IG Index

Source: Bloomberg/Barclays IG Corporate Indices

Banking has maintained its position as the top performing sector within the entire IG Index* since the start of the crisis. From February 17 through yesterday, the Banking sector recorded a -5.70% excess return (vs comparable US treasuries) with just +105 bp in aggregate OAS widening. That compares with -9.19% excess return and a +117 spread change for the IG Index, and compares with the double digit losses among some of the worst performing segments in the market, including: Energy (-18.91%, +243 bp), Finance Cos (-17.15%, +321 bp), Basics (-11.86%, +144 bp) and REITs (-111.62%, +182 bp). Banks have even outperformed the most traditionally defensive segments of the Index, including Tech (-6.01%, +80 bp), Consumer Non-Cyclical (-7.59%, +86 bp) and Utilities (-8.61%, +82 bp). Investors are best served maintaining an overweight of domestic bank credit, or seeking opportunities to add exposure if any selling related to equity concerns materializes in the corporate bond market in the immediate term.

In last year’s US bank stress test, there were record allotments of capital approved by the Fed for dividend and repurchase activity in the approved Comprehensive Capital Analysis and Review (CCAR) results announced mid-summer 2019. Bank of America (BAC: A2/A-/A+) alone instituted a +20% dividend increase and raised their buyback program by $10 billion to a staggering $31 billion for the upcoming 4 quarters. To put that into context, regulators were enabling BAC’s plan to pay out nearly $9-10 billion more to shareholders than they were actually forecast to generate over that time period – meaning that they were very likely to dip into their existing capital surplus to do so. Moving forward, this provides a tremendous amount of flexibility for BAC to postpone, scale back or otherwise eliminate plans for shareholder enhancements in order to preserve their balance sheet and maintain capital ratios. The bank booked a $4.8 billion provision for credit losses in 1Q20 (including a $3.6 billion reserve build), and appears more than likely to follow with additional charges in subsequent quarters. With over $168 billion in Tier 1 capital on the balance sheet as of quarter end, with a Tier 1 Common CET1 ratio in excess of 10%, we believe that BAC can easily scale back its existing shareholder enhancement program and maintain strong capital ratios in even the more pessimistic of economic scenarios to come. Bank bondholders should not be swayed by the inclinations of equity holders, or the prospect of overvaluation based on expected payouts.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.