Uncategorized

Valuing MBS forbearance

admin | May 1, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

The enormous number of borrowers entering forbearance plans is poised to have a big effect on MBS prepayment speeds. Forbearance in conventional MBS is expected to top 10% and in Ginnie Mae reach 20%. Within Ginnie Mae the FHA program should have even higher forbearance rates, approaching 30%. During forbearance, prepayment speeds should slow, but when forbearance ends many non-FHA borrowers are likely to be bought out of pools. Although there is significant uncertainty about future forbearance rates, cure rates, and buyout rates, it is useful to try to measure how much forbearance affects MBS valuations. Ginnie Mae TBAs look compelling, other plays on forbearance not so much.

Ginnie Mae pools are worth more, especially those with only FHA loans

FHA borrowers should have much higher forbearance rates than conventional and VA borrowers. The MBA’s most recent forbearance report shows that 9.73% of Ginnie Mae borrowers are in forbearance compared to 5.46% in Fannie Mae and Freddie Mac pools. It is likely that most of the difference comes from FHA borrowers, since VA borrowers tend to have credit performance comparable to conventional borrowers.

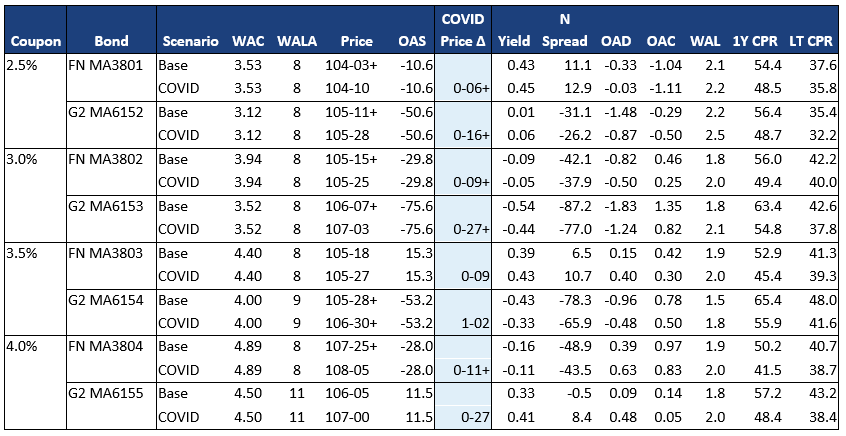

Ginnie Mae pools, especially at higher coupons, benefit more from forbearance than conventional pools (Exhibit 1). For each coupon the Fannie Mae major pool and Ginnie Mae multi issuer pool from September 2019 was run through Yield Book’s prepayment model. The model was then tweaked to account for estimated forbearance and buyout rates in each pool and re-run at the same OAS. The result is a theoretical price improvement from forbearance.

Exhibit 1: Ginnie Mae pools benefit more than conventional pools from forbearance.

Note: Run as of 4/29/2020 close using Yield Book’s v98 experimental model, which gives more realistic OASs but does not incorporate any adjustments for COVID-19. Borrowers enter forbearance over a 5 month period, more heavily weighted to the first 2 months. Loans are assumed to remain in forbearance for 12 months and are unable to prepay. An additional 20% reduction in housing turnover is incorporated for 12 months. After 16 months 50% of borrowers are assumed to cure and the other 50% are bought out. FHA borrowers are assumed to have a 90% cure rate due to the FHA’s partial claim program. Prepayment speeds behave normally after that point. Source: Yield Book, Amherst Pierpont Securities

The conventional pools benefit less from forbearance, and only slightly more at higher coupons even though those pools were assumed to have higher forbearance rates due to lower credit collateral (FICO scores fall at higher coupons). For example, the Fannie 2.5% pool is 768 FICO while the 4.0% pool is 706 FICO, the pools were assumed to have 12% and 21% peak forbearance, respectively But the prospect that many of these loans will eventually prepay as pool buyouts eliminates a lot of the potential increase in value. Forbearance adds 6.5/32s of value to the 2.5% and 11.5/32s to the 4.0% pool.

The Ginnie Mae pools fare much better than the conventional pools at each coupon. Higher coupons generally improve more than lower coupons due to higher concentrations of FHA loans. FHA loans should have higher forbearance rates but also lower buyout rates due to the FHA’s payment deferral program[1]. For example, the 2.5% Ginnie Mae, which is only 25% FHA, is worth 16.5/32s more due to forbearance. That is 10/32s more improvement than the Fannie Mae pool. The Ginnie Mae 3.5% pool (57% FHA) shows the largest increase, $1-02 vs. only 9/32s for the Fannie 3.5%.

Conventional FICO and LTV pools look modestly worse

Loans with low FICO scores or high LTV scores are more likely to be placed on forbearance plans, which should slow speeds over the next year. However, the GSEs don’t currently have an effective program to cure borrowers after a long forbearance while avoiding a buyout. The GSEs’ existing repayment plans are likely to be too burdensome for borrowers that missed 12 payments, so many will need loan modifications. This spike in buyouts could be large enough to wipe out the gains from slower initial prepayment speeds (Exhibit 2).

Exhibit 2: Forbearance does not improve FICO and LTV pool pay-ups

Reference footnote to Exhibit 1 for methodology. Source: Yield Book, Amherst Pierpont Securities

[1] The FHA calls this program the “partial claim” program, but it can cure a borrower of up to 12 missed payments and the loan does not need to be bought out of a pool.

For example, 1-year prepayment speeds on the 3.5% FICO pool are expected to slow nearly 10 CPR, but life time speeds only fall 1 CPR. The generic pool only slows 7.5 CPR in the first year, but the life speed is 2 CPR slower. The result is the FICO pool’s pay-up is projected to fall by 7/32s.

Amherst Pierpont has developed a proprietary model for valuing conventional MBS pools. It was tuned to run using the same forbearance assumptions that were used for Yield Book. This model also shows lower pay-ups for FICO and LTV pools under the COVID scenario (Exhibit 3). For example, the LTV 3.5%s theoretical pay-up dropped 19/32s on the Amherst model and 11.5/32s on Yield Book’s model. Amherst’s model is typically slower than Yield Book, which results in higher pay-ups in the base case. More of this premium is eroded by the spike in buy-outs after forbearance.

Exhibit 3: Amherst’s model also shows lower pay-ups for FICO and LTV pools

Reference footnote to Exhibit 1 for methodology, except uses Amherst Pierpont’s prepayment model, not Yield Book’s model. Source: Amherst Pierpont Securities