Uncategorized

Reframing fundamental risk in legacy RMBS

admin | April 24, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Investors across mortgage credit continue to grapple with fundamental risk associated with the economic effects of COVID-19. Estimating the impact on legacy RMBS may prove especially challenging, however, and creating a framework for reassessing fundamental risk is likely a first critical step in identifying relative value.

Evaluating fundamental risk in legacy RMBS may be uniquely challenging. Borrowers that back these pools show significant seasoning, generally low mark-to-market LTVs and quite often a history of one or multiple loan modifications. Simple shocks to short-term or even long-term drivers of default may not distill the new and unique fundamental risk to the asset class as a result of COVID-19. For example, simply shocking home prices lower by 20% on a loan with a 40% mark-to-market LTV will, in almost all cases, not drive a model to forecast a default or even a delinquency especially if the borrower has strong payment velocity to date. Simply shocking traditional model inputs will likely underestimate the amount of loans that may ultimately default or receive permanent modifications as a result of the large economic disruption associated with the virus. Underestimating rates of modification and default will likely drive investors to overvalue legacy RMBS, particularly more levered classes of risk in excess spread deals that are exposed not only to increased defaults and losses but to declining excess spread as a result of modifications.

So what to do? One potential solution is to tackle this issue from the perspective of the borrower’s propensity to make next month’s payment or the one after that. Discounting the borrowers’ propensity to pay should mimic the real-life effects of the virus on borrower behavior and provide more intuitive results than simply shocking macroeconomic variables like home prices or the rate of unemployment as those will likely only impact performance much further out in the future, and potentially not at all in some cases. Additional assumptions like curtailing prepayments and foreclosures as well as stopping loans that are already in default from being liquidated for some period of time should help frame likely borrower and servicer behavior for the near term as well.

The framework adopted reduces the probability that a borrower will make a payment by 20%. For example, if the borrower is a perfect pay always performing loan with a low mark-to-market LTV, the probability that borrower will make their next payment is nearly 100%, the ‘COVID-19 scenario’ will reduce that probability to just under 80%, meaning that in 80% of borrower and servicer outcomes he pays and in 20% of those paths he does not. And the process is repeated every month for six months, meaning that if that same perfect pay borrower had a 50% chance to pay in month two after missing one payment, the model discounts that to a 40% probability to pay. From there the model, takes over and will run a number of different paths where the borrower can cure, re-perform via modification or ultimately default in the cases where a payment is missed.

Once changes to payment velocity and other assumptions are implemented, existing scenarios can be compared to those using the COVID-19 overlays to assess potential changes to fundamental performance as well as the impact to spreads based new fundamental risks. (Exhibit 1)

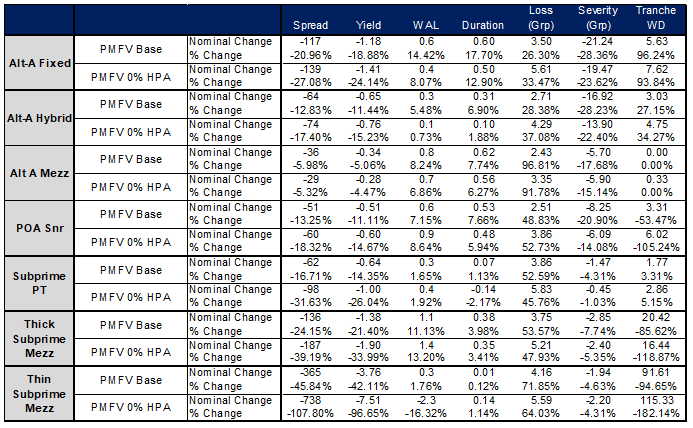

Exhibit 1: Comparing risk and return across base case and COVID-19 scenarios

Source: Amherst Insight Labs, Amherst Pierpont Securities

Looking at both nominal and percentage differences on a handful of legacy profiles with and without COVID-19 overlays across base case and zero HPA scenarios, increases in cumulative losses are relatively modest across Alt-A, Option ARM and subprime profiles due to a decline in payment velocity appear relatively modest. However, depending on capital structure leverage, the impact can be outsized. One somewhat counterintuitive result is seeing negative percentage tranche write downs on Option ARM seniors and subprime mezzanine bonds. This is a function of the bonds forecasting negative losses, or writing up in the base case scenarios versus taking losses in the COVID-19 scenarios as a function of increased defaults and losses as well as a reduction in excess spread due to increased incidence of modifications.

One absolute certainty is that fundamental risk has increased across all flavors of mortgage credit as a result of COVID-19. Payment velocity or the lack thereof may the best way of sizing this risk going forward. Given the uncertainty around the potential impact to levered cash flows, they may be overvalued despite lower prices, they may face increased write downs from a rise in cumulative losses as well as a reduction in excess spread from modifications.