Uncategorized

Nuances of agency multifamily forbearance

admin | April 24, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Mortgage servicers have begun accepting and processing applications for the multifamily forbearance programs launched by Fannie Mae, Freddie Mac and HUD. Differences in implementation, required documentation and ongoing surveillance between the three programs have already led to disparate rates of uptake by multifamily borrowers.

The agencies have taken various measures in an effort make sure that multifamily borrowers entering into forbearance agreements are actually in financial need. Fannie Mae’s forbearance agreement contains the strongest protections, by requiring borrowers to enter into a cash flow sweep agreement, where all operating cash flow is directed towards loan payments throughout the forbearance period. The sweep is subject to borrower certification each month that the remitted payment represents all operating cash flow.

Multifamily mortgage servicers have asked Freddie Mac and Ginnie Mae borrowers to document their financial need by providing monthly rent rolls, but those forbearance agreements do not require the cash flow sweep provisions. This stricter financial condition and the additional operational hurdles it imposes has led to a very small number of Fannie Mae multifamily loans so far entering forbearance – four loans totaling $94 million in principal balance as of 4/22/2020 (Exhibit 1). In addition, servicers have stated that the number of inquiries and active requests they have received from Fannie Mae borrowers has dropped precipitously when they learn of the cash flow sweep.

Exhibit 1: Fannie Mae multifamily loans in forbearance due to COVID-19

Note: The heat map score is a range from 1 to 48 that scores multifamily properties by Congressional district, based on how exposed renter households in that district are to job losses and income stress due to COVID-19. A heat map score of 1 is green, which is the lowest exposure; a score of 48 is red, the highest exposure. See Exhibit 2 for a frequency distribution. Source: Fannie Mae, Amherst Holdings, Amherst Pierpont Securities

Because there are only four Fannie Mae multifamily loans already in forbearance, and Freddie Mac and Ginnie Mae have not yet released details of their loans in forbearance, it’s unwise to draw any conclusions. However, it’s possible to make a few broader points based on the details of Fannie Mae’s forborne loans.

- Of the four loans already in forbearance, three of the loans have heatmap scores above average, with Brooklyn property located in one of the top 5 Congressional districts in the country where renters are potentially the most stressed by job and income loss.

- While the Dallas Texas property has an above average heat map score, perhaps a more significant sign of potential distress is the barely above breakeven debt service coverage ratio.

- Although the score for the White Plains property is roughly average, it’s a senior housing property, the multifamily segment that has come under the most stress due to COVID-19. Senior housing, nursing homes and assisted living/skilled nursing properties have experienced a dramatic rise in expenses due to the need for increased staff and better equipment as a result of health and social distancing measures. At the same time many seniors have left or been relocated from these properties due to the perceived higher risks of virus transmission, decreasing the number of tenants and putting downward pressure on rental income.

Another nuance is that Fannie and Freddie have both included senior housing within their forbearance programs. HUD has stated that nursing homes and assisted living/skilled nursing properties are not included in the streamlined forbearance protocol, but borrowers may apply for forbearance and those requests will be reviewed on a case by case basis.

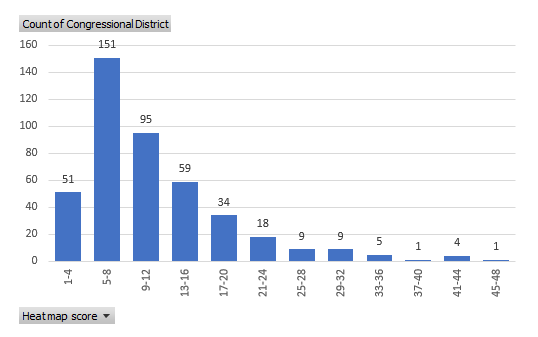

Exhibit 2: Distribution of heat map scores across 437 Congressional districts

Note: The average heat map score across the 437 Congressional districts is 11.3, with a standard deviation of 7.7. However the distribution of heat map scores is leptokurtic and skewed. Only 10.8% of districts have a heat map score of 21 or higher, and less than 7% of districts have greater than or equal to 25. Source: Amherst Holdings, Amherst Pierpont Securities

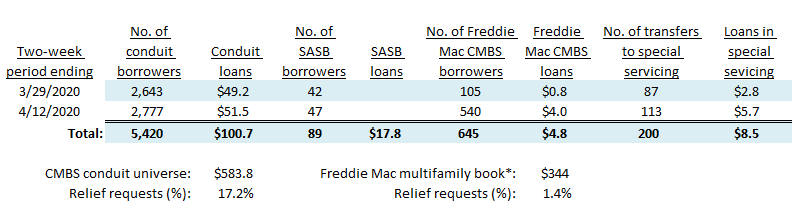

Freddie Mac and Ginnie Mae have not yet released data of their multifamily loans in forbearance, but Fitch Ratings has been collecting data from mortgage servicers across the CMBS universe to log the number of coronavirus related requests (Exhibit 3). The number of requests or inquiries for coronavirus relief from Freddie Mac borrowers was 645 by the middle of April, representing 1.4% of the total multifamily book, or 2.4% of the roughly 27,000 multifamily properties.

Exhibit 3: US CMBS coronavirus related relief requests

Note: During both of the first two period, loans secured by hotel, retail and multifamily assets represent approximately 75% of relief inquiries. Source: Data collected by Fitch Ratings from the four largest CMBS master servicers – Wells Fargo Bank, Midland Loan Services, KeyBank National Association and Berkadia Commercial Mortgage; *Freddie Mac multifamily securitization overview December 31, 2019; Amherst Pierpont Securities

It’s likely that a much larger proportion of the requests and inquiries for forbearance from Freddie Mac borrowers will become active forbearance agreements since the hurdles to execution are lower.

Background on the eviction moratorium in the CARES Act

All three of the housing agencies incorporated the provisions of the CARES Act into their forbearance programs. Tenant protections and landlord requirements are covered in Section 4024 of the Act. An excellent overview is available in the CARES Act Eviction Moratorium, by the Congressional Research Service. The Section prohibits landlords of rental properties that have federally backed mortgage loans, or participate in federal assistance programs, from initiating eviction proceedings against a tenant for the nonpayment of rent for 120 days from enactment (March 27, 2020). Landlords are further prohibited from assessing fees or penalties for nonpayment. At the end of the 120 day period (July 25,2020) landlords must provide the tenant at least 30 days-notice before they must vacate the property (August 24, 2020).

The need for higher frequency data

Payment reports for loans underlying agency CMBS are released on the 25th of each month, so investors only get a comprehensive view of how many borrowers are utilizing forbearance programs at the end of the month, weeks after the payment deadline. However, the COVID-19 emergency has forcefully demonstrated the need for higher frequency data to monitor economic, tenant and borrower stress in real time. This has led some mortgage servicers, property management software companies and the agencies themselves to release more frequent updates.

Fannie Mae has been the first agency to respond to the market, releasing a list of multifamily loans already in forbearance due to COVID-19 (Exhibit 1) on DUS Disclose, and promising to update the list weekly.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.