Uncategorized

The unfolding story of forbearance and its impact on value

admin | April 17, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Borrowers with mortgages guaranteed by Fannie Mae and Freddie Mac or insured by the government can request temporary payment forbearance if they suffer hardship due to COVID-19, and the only requirement is a simple borrower attestation. The ease of attesting to hardship has raised concerns that borrowers will request forbearance in overwhelming numbers. But conversations with servicers so far indicate a more moderate response. Servicers suggest that some borrowers seem deterred by the requirement to attest to financial hardship or the realization they might lose the opportunity to refinance, and borrowers are generally requesting forbearance for only 60 or 90 days. The unfolding forbearance story still favors Ginnie Mae MBS over conventional, FHA loans over VA, low FICO and high LTV pools and poses risk to price premiums in loan balance pools.

Many servicers feel forbearance requests have been lower than expected

Multiple servicers have indicated that they have received fewer forbearance requests than they expected, and the pace has slowed in April after an initial surge. However, forbearance rates at some services in early April ranged as high as 8%, well above the 3.74% reported by the MBA’s forbearance survey. There are a few possible explanations:

- Timing probably plays a big role, as some servicers reported placing as many as 1% of their loans onto forbearance plans each day. So the MBA survey might reflect that increase next week.

- Some servicers likely ramped up their ability to offer forbearance faster than others. A loan in forbearance will not count towards a servicer’s overall delinquency rates, but a loan not on forbearance will.

Servicers hold a wide range of expectations for the likely peak levels of forbearance, ranging from about 5% to 15% for conventional loans and 10% to 25% for Ginnie Mae, with VA loans performing much better than FHA.

The March prepayment report showed little to no evidence that growing unemployment had prevented a large number of pending loans to fail to close. Most servicers confirmed a relatively small increase in the fall-out rate. The highest number reported was an additional 5% of loans failed to close.

Getting forbearance for COVID-19 is easy for loans in agency MBS

Virtually no documentation is required to receive forbearance for loans in conventional and Ginnie Mae pools. The borrower merely needs to attest that the hardship exists. This policy for granting forbearance is mandated in the CARES Act and must be followed by the GSEs and the various government programs that insure loans including the FHA, VA, USDA Rural Housing, and Public Indian Housing. The potential for borrowers to unnecessarily request forbearance in order to get “free money” seems large. However, servicers have seen many borrowers back away from a forbearance request when asked for their attestation of hardship or when the borrower is told that forbearance may prevent a future refinance.

The CARES Act also states that borrowers may initially request up to six months of forbearance and can extend an additional six months, for a total of 12 months. The request for forbearance or extension must be made prior to the later of two dates: (1) 120 days after enactment of the CARES Act, and (2) 120 days after the COVID-19 emergency declaration terminates.

During forbearance, the borrowers do not make any payments of principal, interest, taxes, and insurance (PITI). The agencies can record the delinquency, but the delinquency is not to be reported to credit agencies.

Servicers and the GSEs share responsibility for advancing P&I investors

Agency MBS investors are guaranteed timely payments of principal and interest on their securities. But there are vast differences between how each agency makes up the shortfall.

Fannie Mae requires the servicer to advance principal and interest (P&I) to Fannie Mae for loans in single-issuer and Major pools. Loans sold to the cash window often require the servicer to advance only interest or make no delinquent advances at all. For cash window loans that require advancing, the servicer advances regardless of whether a loan is in a pool or Fannie Mae’s portfolio.

Freddie Mac only requires servicers to advance the first four months of missed interest to Freddie Mac. Freddie Mac is responsible for all principal and interest advances to pools. The servicer’s requirement to advance interest does not depend on whether a loan is in a pool.

Ginnie Mae, however, requires servicers to advance P&I on all loans that are currently in Ginnie Mae pools. Ginnie Mae never makes advances for delinquent loans.

Non-bank servicers might have trouble with advances

Funding advances of principal and interest is a challenge for many non-bank servicers. However, principal and interest (P&I) advances are somewhat easier to cover. A natural source of funding are the custodial accounts. When a servicer receives a loan payoff, the funds are placed into an account and remitted to the agency the following month, so there is typically a balance in the account on which the servicer earns interest. The servicer can use that float to pay this month’s P&I advances. There might be enough funds, especially if prepayment speeds remain elevated, to cover a few months of advances.

Besides using the custodial account, servicers would need to setup financing lines. This is much harder to do with Ginnie Mae, although PennyMac recently announced the first arrangement to receive Ginnie Mae’s approval. Ginnie Mae has also implemented their own program, called “PTAP/C19” (Pass-Through Assistance Program/COVID-19). Under this program Ginnie Mae will make fixed rate loans to servicers for the purpose of paying P&I advances. But Ginnie Mae considers this last resort financing and servicers need to document their attempts to secure other financing.

Servicers are also responsible for advancing tax and insurance (T&I) payments. Every servicer contacted stated that T&I advancing was far more troublesome, primarily since the custodial account cannot be used for this purpose. Any funds in an escrow account can be used before the servicer must remit its own funds, but the escrow accounts cannot be comingled. In the near term most T&I payments will be for insurance, not taxes, since tax bills are usually due near the end of the year. That helps minimize the size of the initial T&I advances, but the amount will grow later in the year.

Buyouts—when delinquent loans are removed from pools

Fannie Mae, Freddie Mac, and Ginnie Mae all have mandatory and optional conditions for removing loans from their pools. These removals are known as buyouts, and result in a prepayment of principal at par to the investor.

Fannie Mae and Freddie Mac’s MBS trust agreements require a buyout of loans that are modified, foreclosed, or have been delinquent for 24 months. They also have a policy, since early 2010, to buyout loans when they became 120 days delinquent. This policy can be altered at their discretion. An example is after the 2017 hurricanes, when the GSEs allowed loans on temporary disaster forbearance plans to remain in pools in order to given them a longer chance to recover.

Ginnie Mae also requires a buyout of loans that are modified or foreclosed, but does not require a buyout of loans that are 24 months delinquent. Ginnie Mae also grants servicers an option to buy out loans that are at least 90 days delinquent. A servicer with good liquidity might choose to buy out loans quickly to save on P&I advances if they can fund the loan more cheaply on their balance sheet or repool the loan later at a premium price. But a non-bank servicer might find that advancing P&I is the cheaper option. Non-bank servicers already behave in this manner—the 60+ day delinquency rate for non-bank servicers is currently 2.7% and for bank servicers is 1.2%, and the 180+ day delinquency rate is 0.94% for non-bank servicers and only 0.17% for bank servicers.

Will a loan be bought out while in forbearance?

Investors need to know how long the GSEs will allow loans on temporary forbearance for COVID-19 to remain in pools, but neither GSE has yet announced their plans. Fannie Mae initially indicated that they would leave loans on temporary forbearance in a pool beyond 120 days delinquent, as with other natural disasters. This makes sense if they feel many of these loans will eventually cure, but that notice was removed from their website. The two GSEs must follow the same buyout policy to maintain comparable prepayment speeds under UMBS. It is possible that Freddie Mac prefers a quicker buyout timeline since they bear the burden for advancing past four months, where Fannie Mae may be ambivalent since they do not advance on many loans. This possible disagreement might be behind the delay.

Avoiding the buyout—options to cure loans

Fannie Mae and Freddie Mac are responsible for the credit risk on the loans they guarantee, so they authorize the various programs that servicers can use to cure delinquent loans. Some of the options result in a loan modification, which requires the loan to be bought out of a pool.

Servicers do have a couple of options to cure a delinquent GSE loan. One is to have the borrower enter a repayment plan. Over a set time frame, the borrower makes their mortgage payment plus an additional payment to cure their delinquency. However, the more payments a loan has missed the harder it is for borrowers to afford a repayment plan. The GSEs also just introduced a plan called “payment deferral.” This permits borrowers that are only one or two payments behind, but have resumed making payments for at least three months, to defer the missed payments until the loan is paid off or matures. The deferral is done at no interest. If borrowers do not qualify for either of these options, they will eventually be bought out.

For Ginnie Mae loans, the workout options are provided by the FHA, VA, Rural Housing, and Public Indian Housing programs. All of these agencies have options for repayment plans and loan modifications.

The FHA, however, offers a unique program known as the partial claim. The servicer makes a claim against the FHA insurance on the loan, but only for a portion of the total insured amount. These funds can be used to cure up to 12 months of delinquent principal, interest, taxes, and insurance. The borrower owes the money to the FHA in the form of a no-interest subordinate lien. A borrower can use the partial claim program multiple times, up to a cumulative amount equal to 30% of the loan’s unpaid balance at the time of the first partial claim. A partial claim can be resubordinated on subsequent FHA-to-FHA refinances, but would need to be paid off to refinance out of the FHA.

The FHA has announced that all borrowers receiving temporary forbearance for COVID-19 will first be evaluated for a COVID-19 partial claim. This could allow a significant number of FHA borrowers to cure and reduces the risk of large buyouts of FHA loans.

The partial claims are funded from the FHA’s insurance fund, the Mutual Mortgage Insurance Fund or MMIF. The most recent actual review reported that the fund had $54.6 billion of capital available. The total PITI for FHA loans in Ginnie Mae pools, assuming 50 bp for T&I, is just under $7 billion a month. This implies that partial claims would total $21 billion if 25% of FHA loans use 12 months of forbearance and make partial claims. This would likely reduce the capital ratio of the MMIF to roughly 2.75%, still above the statutory minimum of 2%.

Forbearance should slow prepay speeds, but buyouts are a critical factor

If loans remain in pools while on forbearance plans, it is very unlikely those loans will be able to prepay. This means that speeds on those pools should slow, possibly significantly. For example, a pool with 10% of loans in forbearance should slow by that same factor.

The GSEs likely pose a greater buyout risk than Ginnie Mae pools. There is the risk that the GSEs will buyout loans during a longer forbearance period, and the GSEs have limited options to cure loans that have been delinquent for a long period of time. Ginnie Mae’s heavy dependence on non-bank servicers, which handle roughly 70% of servicing, means that early buyouts are less likely to happen, giving loans more time to cure. And the FHA’s partial claim program could allow a significant number of loans that use a full 12 months of forbearance to cure without a buyout. The VA does not have a partial claim program so may see more loans require buyout, although VA forbearance rates are likely to be much lower than FHA.

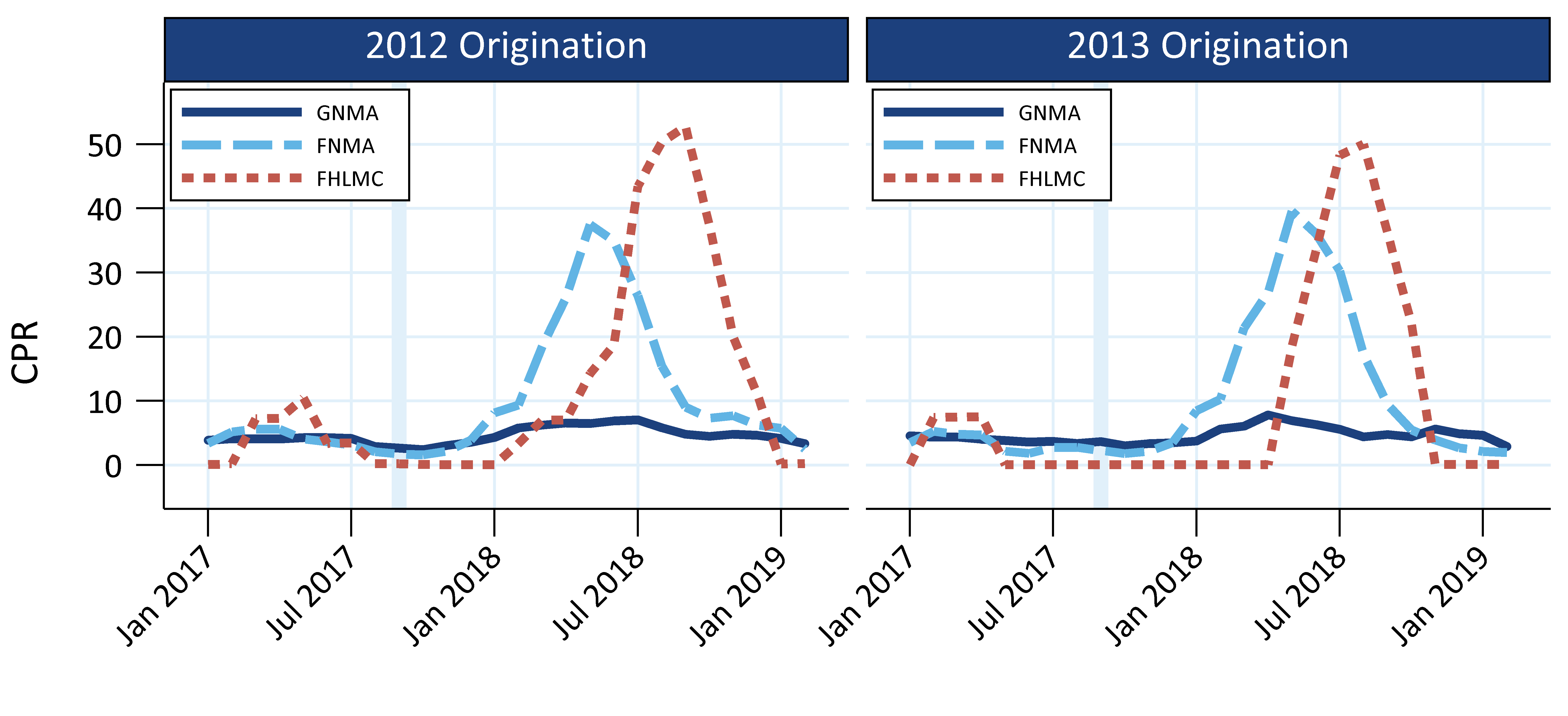

Prepayment speeds in Puerto Rico following Hurricane Maria illustrate the difference between the GSEs and Ginnie Mae (Exhibit 1). Ginnie Mae speeds on these loans remained very slow, showing a very small uptick in buyouts in early 2018. GSE speeds, however, spiked as high as 50 CPR when loans exited their 6-month forbearance plans and could not be cured. Note that most Ginnie Mae Puerto Rico loans are FHA, so the slow speeds are very likely a result of the FHA partial claim program.

Exhibit 1: Ginnie Mae Puerto Rico loans prepaid well after Hurricane Maria

Source: Ginnie Mae, eMBS, Amherst Pierpont Securities

Therefore, prefer Ginnie Mae to conventional, and FHA to VA

Ginnie Mae pools have the greatest chance to benefit from slower prepayments due to forbearance. This is because FHA loans should face much higher forbearance rates, be more likely to remain in pools, and be cured without a buyout. VA loans are less likely to be cured but should have lower forbearance rates. The best performing pools should have a very high percentage of FHA loans. The majority of Ginnie Mae loans are not serviced by banks, making it unlikely those servicers would exercise their buyout option.

Conventional pools currently face greater policy risk. The uncertainty around the timing of buyouts means that there is some chance loans that might otherwise cure could be removed from pools. This means those pools would have fewer months of slower speeds from loans with forbearance followed by higher buyout rates.

Forbearance may lower loan balance pay-ups

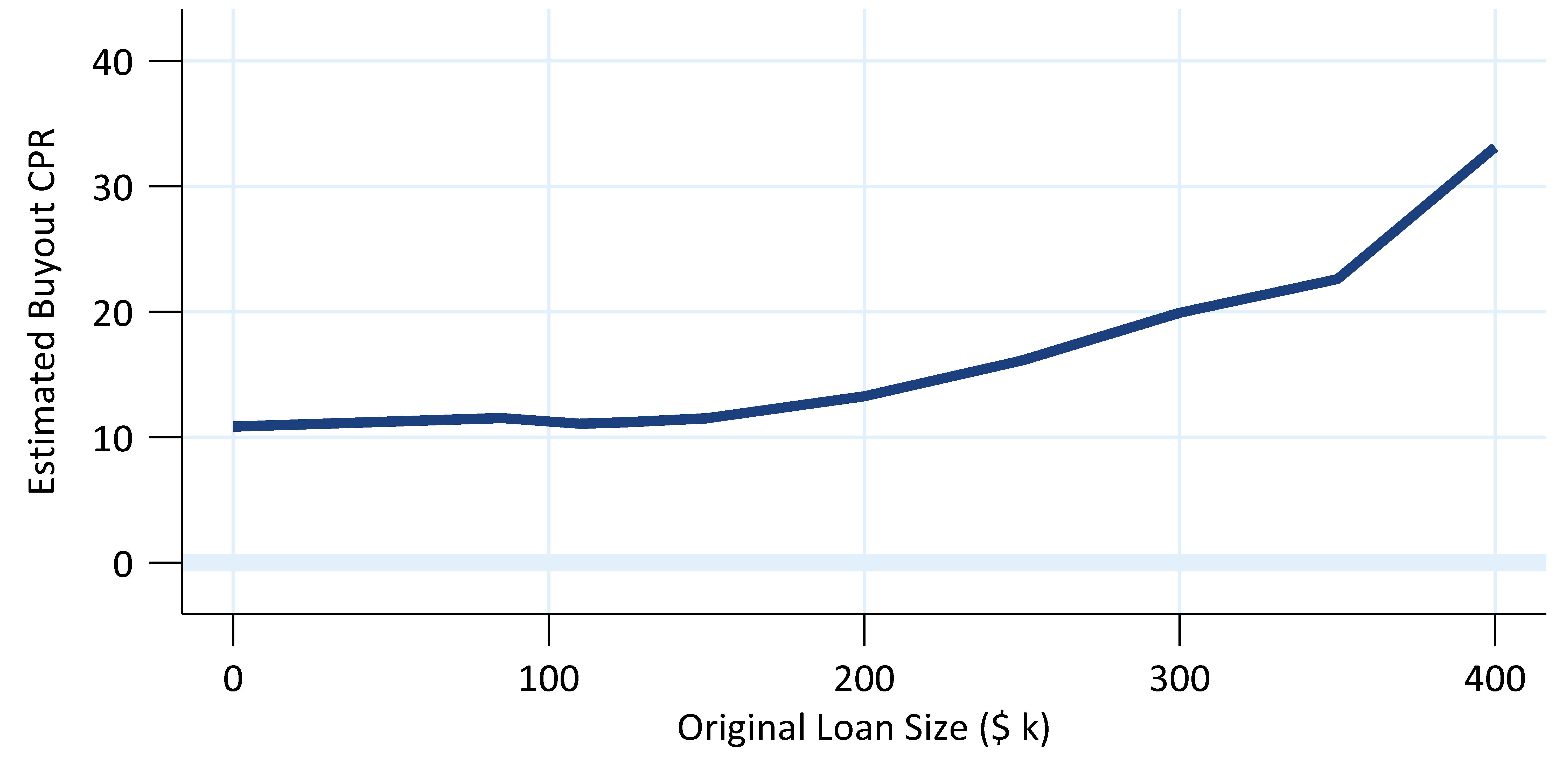

Prepayment data following the 2008 financial crisis suggests that higher balance pools may exhibit higher delinquency rates than lower loan balance pools. If this happens during the current crisis the improved convexity of TBA pools would cause loan balance pay-ups to decline. The relative default rates for different collateral types over 2008 and 2009 can be estimated from Freddie Mac’s loan level prepayment data in February 2010.

Loans with higher balances showed much larger month-over-month prepayment speed increases than lower balance loans (Exhibit 2). At the time most Freddie Mac loans were below the $417,000 conforming limit. While loans in the LLB/MLB range had an estimated 10 CPR buyout rate, loans near the conforming limit had a 30 CPR buyout rate. This implies higher balance loans defaulted roughly 3× faster than the lower balance loans over the prior two years.

Therefore, the S-curves of worst-to-deliver pools may flatten more than lower loan balance S-curves, which should lower pay-ups. However, those pools will eventually be at greater risk of elevated prepayments from buyouts since some loans will not be able to cure by the end of their temporary forbearance plans.

Exhibit 2: Larger loans defaulted faster during the 2008 financial crisis.

Prepayment speed increase from January 2010 to February 2010. Includes 2005–2007 vintage loans with FICO≥700 and Case Shiller Mark-to-Market LTV≤80. Source: Freddie Mac, eMBS, Amherst Pierpont Securities

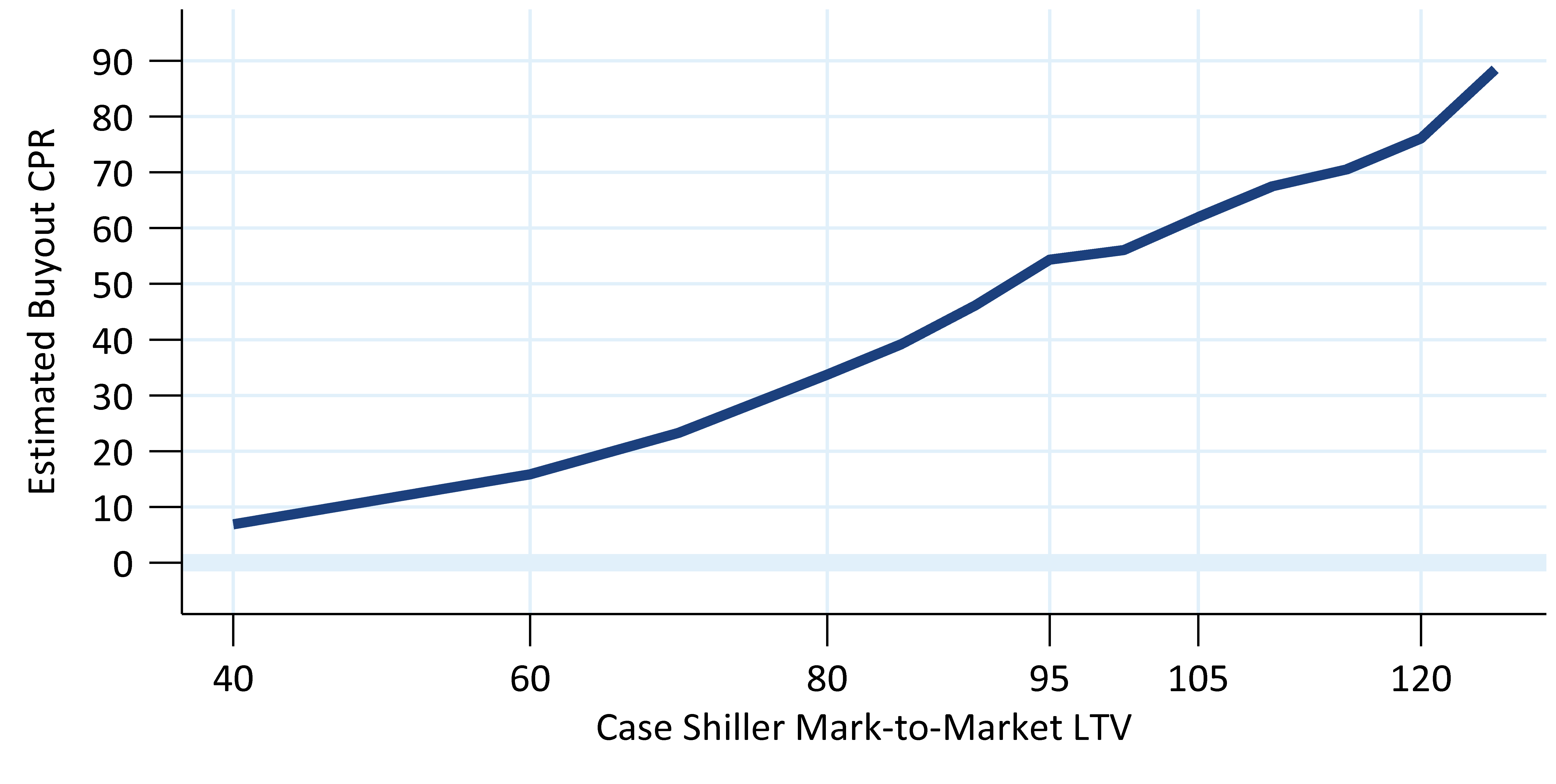

High LTV loans should see much higher delinquencies

High LTV pools are likely to have higher delinquency rates and flatter S-curves, but are more likely to have faster buyout rates as forbearance ends (Exhibit 3). High LTV borrowers, especially those with initial LTVs above 95, generally stretched to buy their homes and have fewer assets to rely on to make payments. And borrowers with little equity are more likely to walk away from the home altogether. So these loans may experience lower cure rates than others. Loans between 95 and 105 mark-to-market LTV (estimated using Case Shiller’s home price index) prepaid roughly 45 CPR faster than a 60 LTV loan due to buyouts.

Exhibit 3: Higher LTV loans defaulted faster during the 2008 financial crisis.

Prepayment speed increase from January 2010 to February 2010. Includes 2005–2007 vintage loans with original loan size≥150,000 and FICO≥700. Source: Freddie Mac, eMBS, Amherst Pierpont Securities

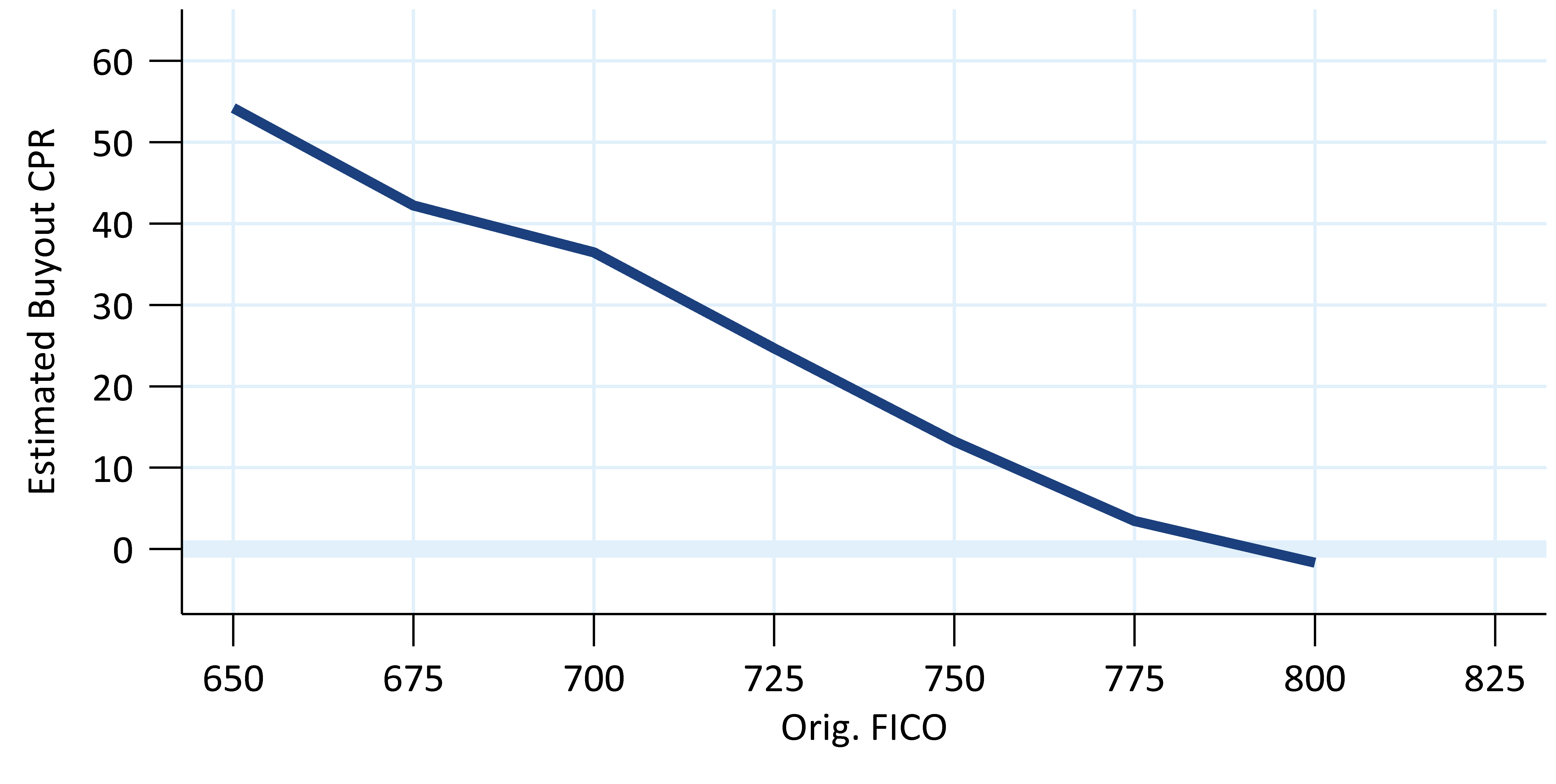

Low FICO loans are more exposed to unemployment too

Low FICO loans defaulted faster than high FICO loans during the 2008 financial crisis, while the best credit borrowers had very low buyout rates (Exhibit 4). The typical low FICO borrower in current GSE pools is roughly 675 FICO, which prepaid about 40 CPR faster than a 750 FICO borrower due to buyouts. Therefore S-curves should flatten significantly on these pools. This also implies that FICO pools should see slightly lower delinquency rates than high LTV pools. However, low FICO pools will likely exhibit a better cure rate than high LTV pools since low FICO pools usually have lower LTVs.

Exhibit 4: Lower FICO loans defaulted faster during the 2008 financial crisis.

Prepayment speed increase from January 2010 to February 2010. Includes 2005–2007 vintage loans with original loan size≥150,000 and Case Shiller Mark-to-Market LTV≤80. Source: Freddie Mac, eMBS, Amherst Pierpont Securities