Uncategorized

Themes from the investment grade new issue market

admin | March 27, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

The Fed’s announcement of a corporate backstop with an unlimited QE program which would include both primary and secondary corporate bonds and ETF stoked the flames of the Investment Grade new issue market. New issue concession spreads were lofty at the start of the week – triple digits in some cases – but compressed as the week wore on due to high demand. What was previously exclusive to only high quality issuers opened up to include names with BBB ratings and higher leverage. Investors are urged to exercise caution around new issue as there are fewer “deals” to be had. The “back the trucks up” mentality should evolve into one of “pick and choose your spots”.

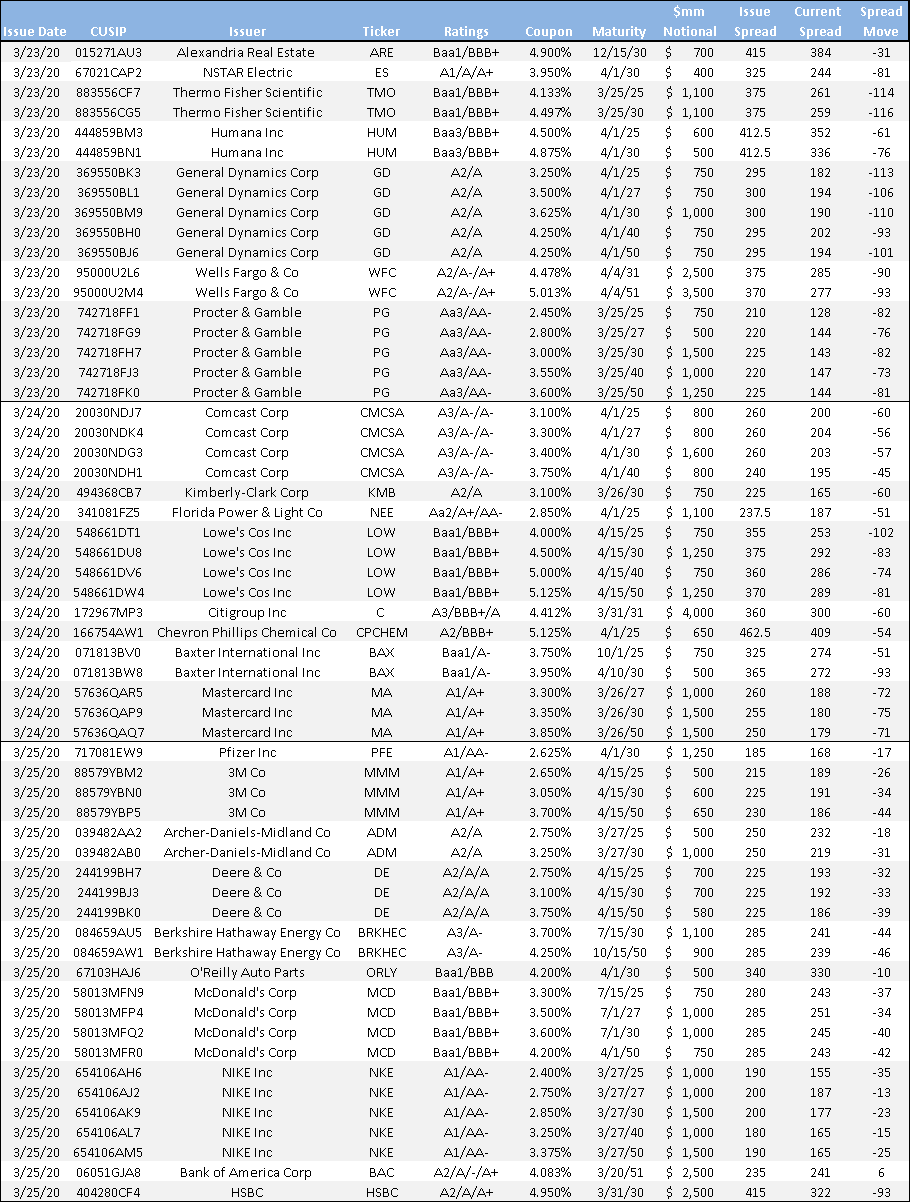

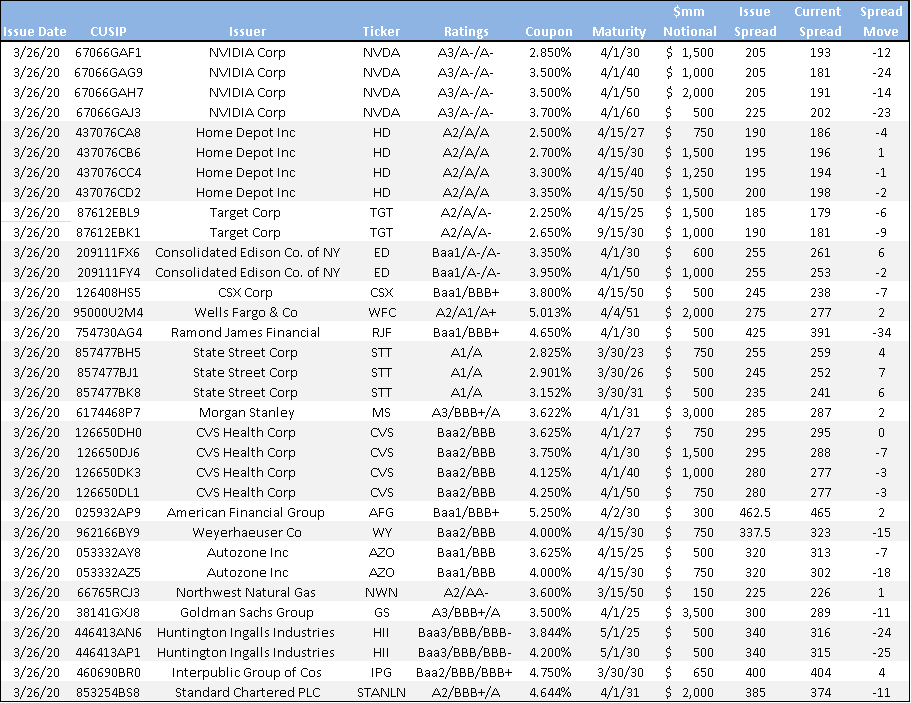

The market saw an average of $20 billion of new supply per day for the first 3 days of the week, with a sizeable jump towards the end of the week (Exhibits 1 and 2).

Exhibit 1: New Issue Supply (3/23/20 – 3/25/20)

Source: Bloomberg; TRACE; Amherst Pierpont Securities

Exhibit 2: New Issue Supply (3/26/20)

Source: Bloomberg; TRACE; Amherst Pierpont Securities

Concessions Get Squeezed

The week of March 23rd began with lofty concessions which were enticing to IG investors post Fed announcement. New issue concessions on Monday were on average 85 bp wide to secondaries, with some names wider than 100 bp. Even highly rated credits like Proctor and Gamble (PG – Aa3/AA-), came to market with concessions in the 40-75 bp range. Deals were largely oversubscribed by 5x on average with demand in the 20-year and 30-year part of the curve outpacing 10-years and in. This lead to approximately $20 billion of issuance, per day, for the first three days of the week. By Thursday March 26th, new issue volume nearly doubled from Wednesday’s total, however, at much tighter concessions than those at the start of the week. Thursday’s concessions were on average in the 20-30 bp range with some deals pricing relatively flat to secondaries, including Home Depot and CVS.

Double Tap

McDonalds Corp. (MCD – Baa1/BBB+ (n)) took advantage of the new issue window and tapped the market for $3.5 billion in an effort to shore up liquidity. This was the second time in the month of March that MCD was in the new issue market. Earlier in the month, MCD issued $1.25 billion across 5s and 10s. Both issuances were listed for general corporate purposes, but headlines surfaced that MCD may be looking to lend support to its franchisees as stores in Italy, Spain, France and the UK are currently closed. In the United States, MCD is operating stores for take-out and delivery in areas where stores do not have a drive-thru window. Additionally, MCD drew down $1 billion on a new 365-day revolver. Should demand for new issue remain, other non-bank/financial credits could follow MCD’s lead. At time of writing Omnicom Group (OMC – Baa1/BBB+) announced a $500 million 10-year deal. OMC is not an active issue by any stretch and was just in the market in February for $600 million.

US Banks Active amidst the Deluge

The US money center banks have been extremely active over the past two weeks, pricing $21 billion this week (through Thursday), following $11.3 billion in the prior week, for a two-week total of nearly $25 billion (including a $1.75 billion 3-part offering from State Street). Deals that priced in the prior week offered large concessions, led the charge in the re-ignition of IG primary markets. Issuers paid large premiums, but took advantage of low overall coupons, flat credit curves and investors’ fervent demand for long duration. Deals priced as follows:

3/17/20

GS $2.5 billion 10-yr +300

BAC $3 billion 31NC10 +260

3/19/20

JPM $2.5 billion 11NC10 +340

MS $2.0 billion 31NC30 +375

C $1.3 billion 21NC20 +350

At the start of this week, WFC led the charge with a two part offering ($6 billion), for which they paid maximum concessions. They tapped the long bond just three days later and were able to price an additional $2 billion at nearly 100 bp cheaper from the initial Monday launch. Goldman proved among the savvier issuers in both weeks, timing the market well and cutting back on its issuance costs. BAC also circled back to their long bond, able to shave off 25 bp of interest from their launch in the prior week. While concessions have compressed taking the ease of the trade away in broader IG corporates, investors should continue to accumulate these newer bank deals aggressively, in an effort to position portfolios defensively to the ongoing economic and event-driven uncertainty that will continue to drive volatility. This is highlighted in last week’s article APS Strategy: Sector view update, which updated Sector views for the next six months. The new GS 5-year notes are particularly attractive long-term among the mix of issues that are now trading actively on the turn.

3/23/20

WFC $2.5 billion 11NC10 +375

WFC $3.5 billion 31NC10 +370

3/24/20

C $4.0 billion 11NC10 +360

3/25/20

*BAC $3 billion 31NC10 +235 (TAP)

3/25/20

MS $3.0 billion 11NC10 +285

GS $3.5 billion 5-yr +300

*WFC $2.0 billion 11NC10 +275 (TAP)

An interesting wrinkle worth highlighting in GS’ efforts to tap the debt markets is management’s decision to forego the one-year call structure that has remained so prevalent over the past several years. They are among the only banks to do so recently, which is likely a sign that they are comfortable with their TLAC regulatory capital levels and do not feel obligated to “pay up” for the one year of callability. The reason the issuers have been doing this the past several years is that bonds lose TLAC eligibility in their final year, which mean these structures allow the bond to remain TLAC eligible for the fixed period, of typically 5, 10 or 30 years. GS’ decision to move away from the structure is a possible sign that as these bonds approach maturity, the likelihood that the banks call the bond if not economically sensible has dropped considerably, particularly in the current rate environment.