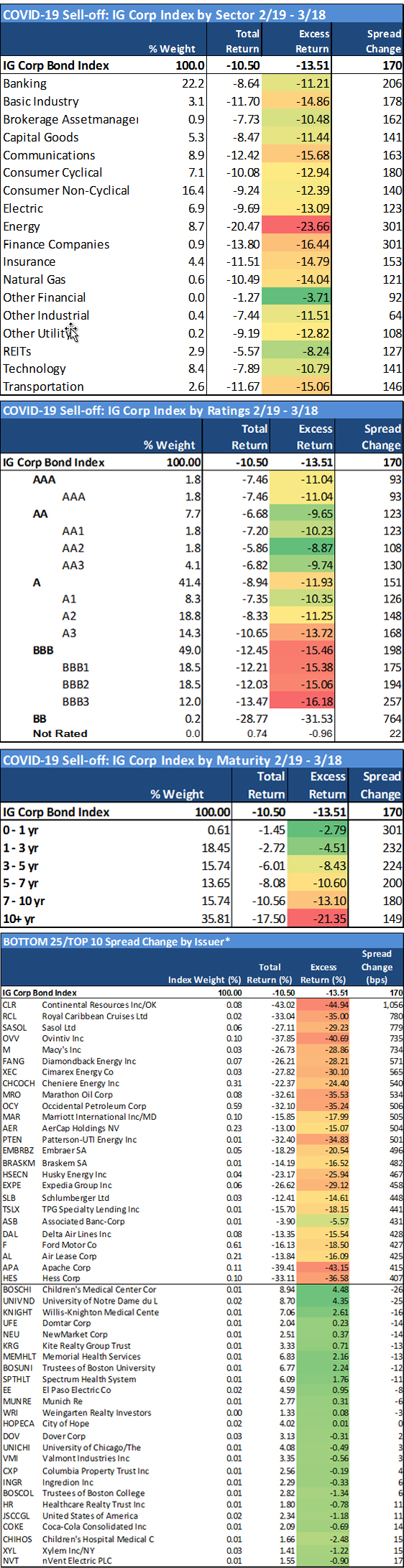

Uncategorized

Adopt defensive posture emphasizing domestic banks and technology

admin | March 20, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

Investors should move to a more defensive posture based on expectations that the global economic fallout of the COVID-19 outbreak will continue well into the second half of 2020, with limited prospect for relief in near-term volatility. The compounded stress on energy/commodity markets is making it extremely difficult to time fluctuations in valuation among commodity credits, which further supports a call to overweight more defensive segments within the Index. The long-term valuation proposition in higher rated, less cyclical credits is compelling enough to forego more aggressive strategies that are susceptible to day-to-day swings in volatility.

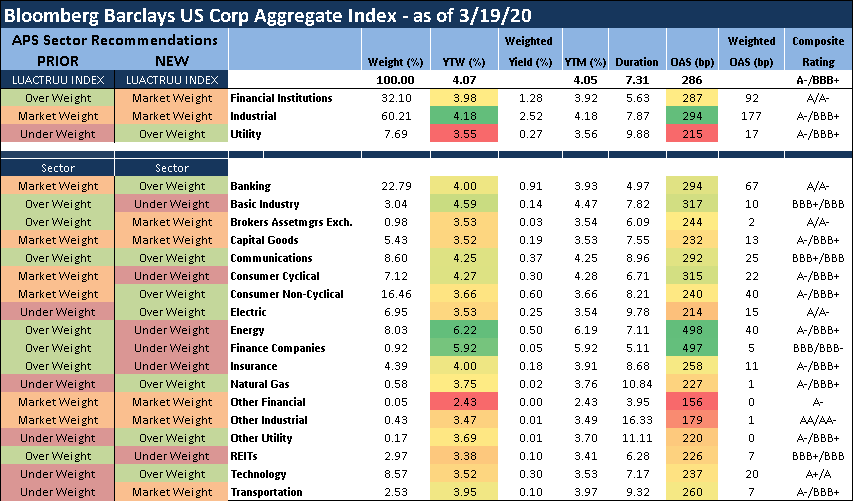

Exhibit 1: Updated sector recommendations

Note: Updated sector recommendations within the IG Index are based on performance expectations over the next several months on an Excess Return basis (total return net of commensurate UST return). These weightings serve as a proxy for how portfolio managers should position their holdings relative to the broad IG corporate bond market. Source: Bloomberg/Barclays US corporate index, Amherst Pierpont Securities

Key Sector View Changes

Banking – Overweight from Marketweight: Over the past few days, three of the US money center banks brought long duration new issues (JPM $2.5 billion 11NC10s, MS $2 billion 31NC30s, C $1.3 billion 21NC20s), with large concessions to investors but attractive overall yields to the issuers. Investors should be positioning these new issues aggressively at these current valuations. While the macro and yield curve environment present obvious challenges and obstacles to near-term profitability, bank balance sheets remain extremely well capitalized with added flexibility available (throughout postponement of shareholder payouts). The banks are being utilized in Fed policy as a source and backstop to systemic liquidity, and are at present reportedly being told to keep “dry powder” – a favorable posture for bondholders. Investors should favor US money center banks over the regionals, while there is good long-term valuation in the otherwise conservative, smaller regional and community banks with debt outstanding.

Consumer Cyclical – Underweight from Marketweight: The sector is suffering heavy negative impact from COVID-19 as retailers close stores and restaurants primarily move to to-go orders. While expectations are for an increase in online sales for retailers, the consumer will be focusing mostly on non-discretionary purchases. Large restaurant chains are currently forecasting same store restaurant sales to be down 50% in the current quarter, which arguably will put them into free cash flow negative territory. Lodging is seeing occupancy rates across North America and Europe below 25%, forcing hotels to shut down and workers to be furloughed in an effort to stem the cash drain.

Consumer Non-Cyclical – Overweight from Marketweight: Packed Food and Grocers are benefiting from pantry stocking which will likely be somewhat short lived. Panic buying of shelf stable items will take the consumer some time to consume, that said the initial volume burst will taper off a bit. This could change buying patterns of the consumer though for an extended period of time as a larger portion of the global population will need to look at home prepared meals as a way to offset lost income.

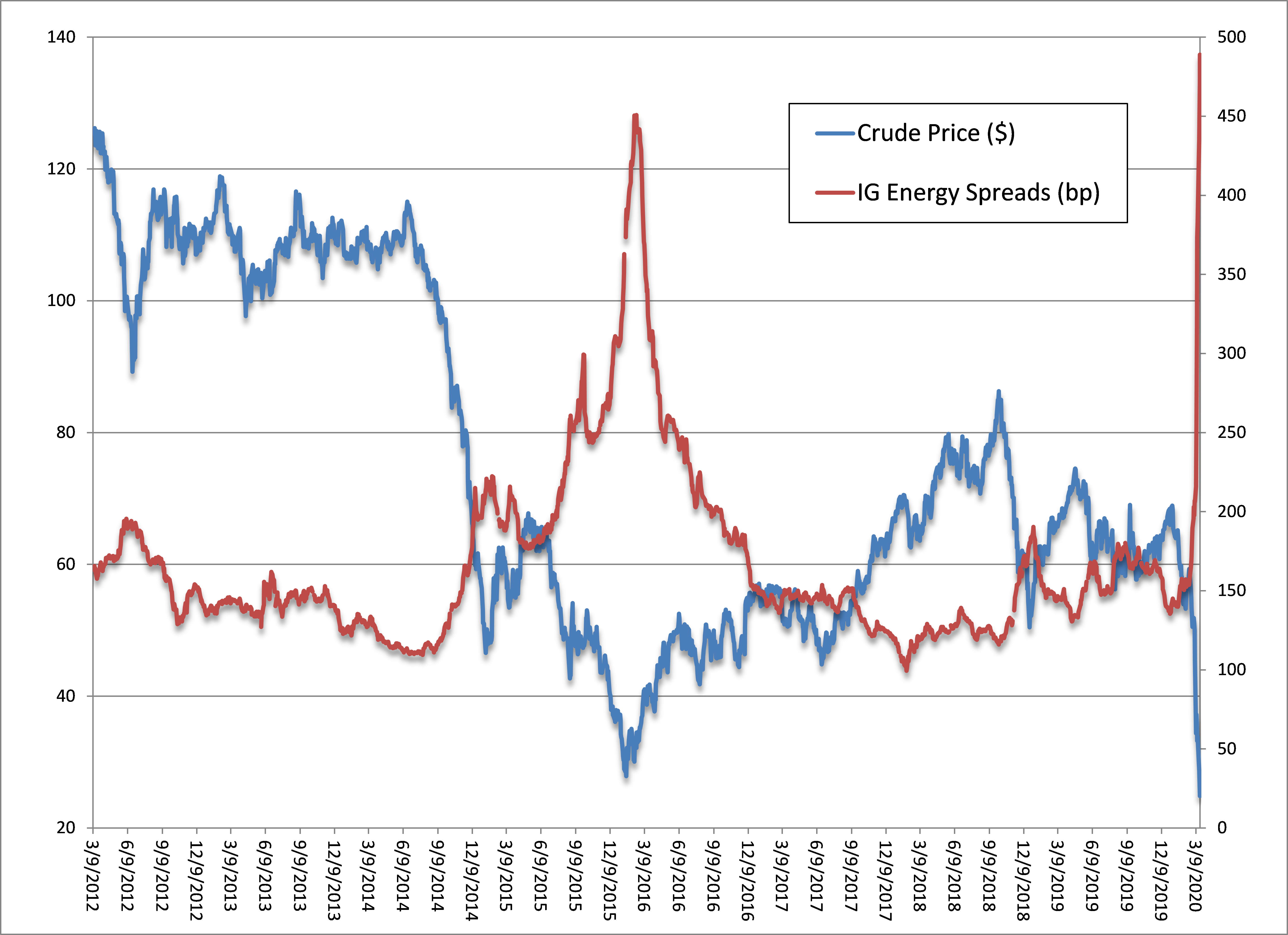

Exhibit 2: IG Energy spreads vs. crude prices

Note: Bloomberg/Barclays Corporate Agg Index, Bloomberg Generic 1st CO Futures Contract. Source: Bloomberg, Amherst Pierpont Securities

Insurance – Underweight from Overweight: The Insurance industry—in particular the Life insurers—are facing challenges on numerous fronts in the current market environment. The flat yield curve, low re-investment yields, annuity exposure, and volatile investment returns are among the more obvious issues surrounding the sell-off in the industry. Investors should maintain less exposure to Insurance overall, while concentrating holdings in the highest quality issuers that have sold off with the broader segment (ALL, PGR, BRK, CB).

REITs – Underweight from Overweight: With retailers implementing store closures and office employers following telecommuting protocols for coronavirus, there are significant concerns that this temporary period of displacement will have more permanent impacts on both Retail and Office REIT commercial real estate. Retailers are likely to make store closures permanent, accelerating the pre-existing meltdown in traditional commercial real estate for mall operators. Recommend investors shift weightings within the sector to the Industrial, Health Care, Cell Tower and well-diversified Single-Tenant (triple-net) segments.

Technology – Overweight from Underweight: Liquidity is king and the cash rich balance sheets of the large cap technology/Internet credits, with some boasting large net cash positions, are providing a relative safe haven during these volatile times. The space further benefits from high free cash flow conversion rates, which helps to boost liquidity.

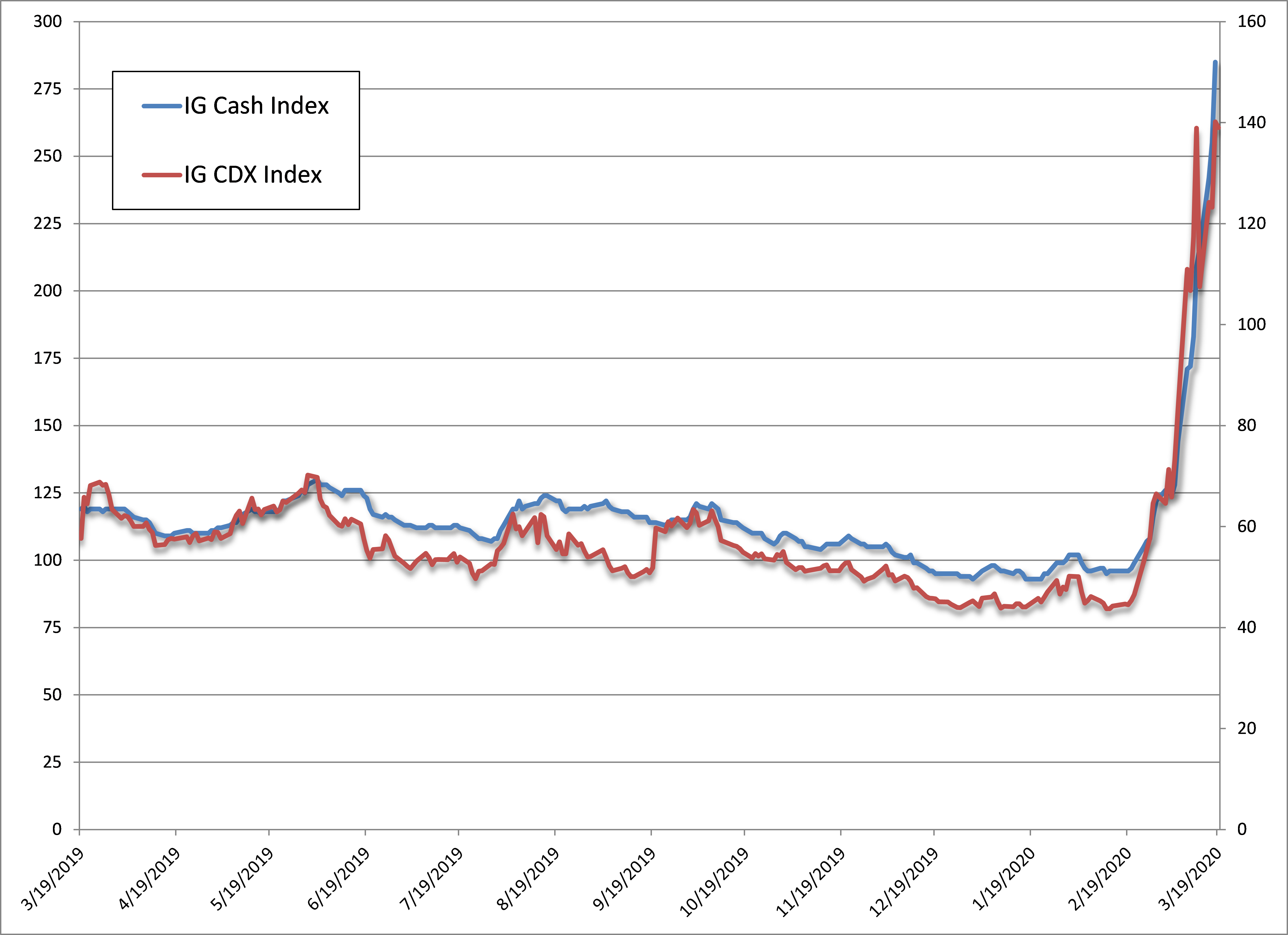

Exhibit 3: Corporate bond spreads (cash and CDS)

Source: Bloomberg/Barclays Corp Agg Index, Markit CDX NAIG Index, Amherst Pierpont Securities

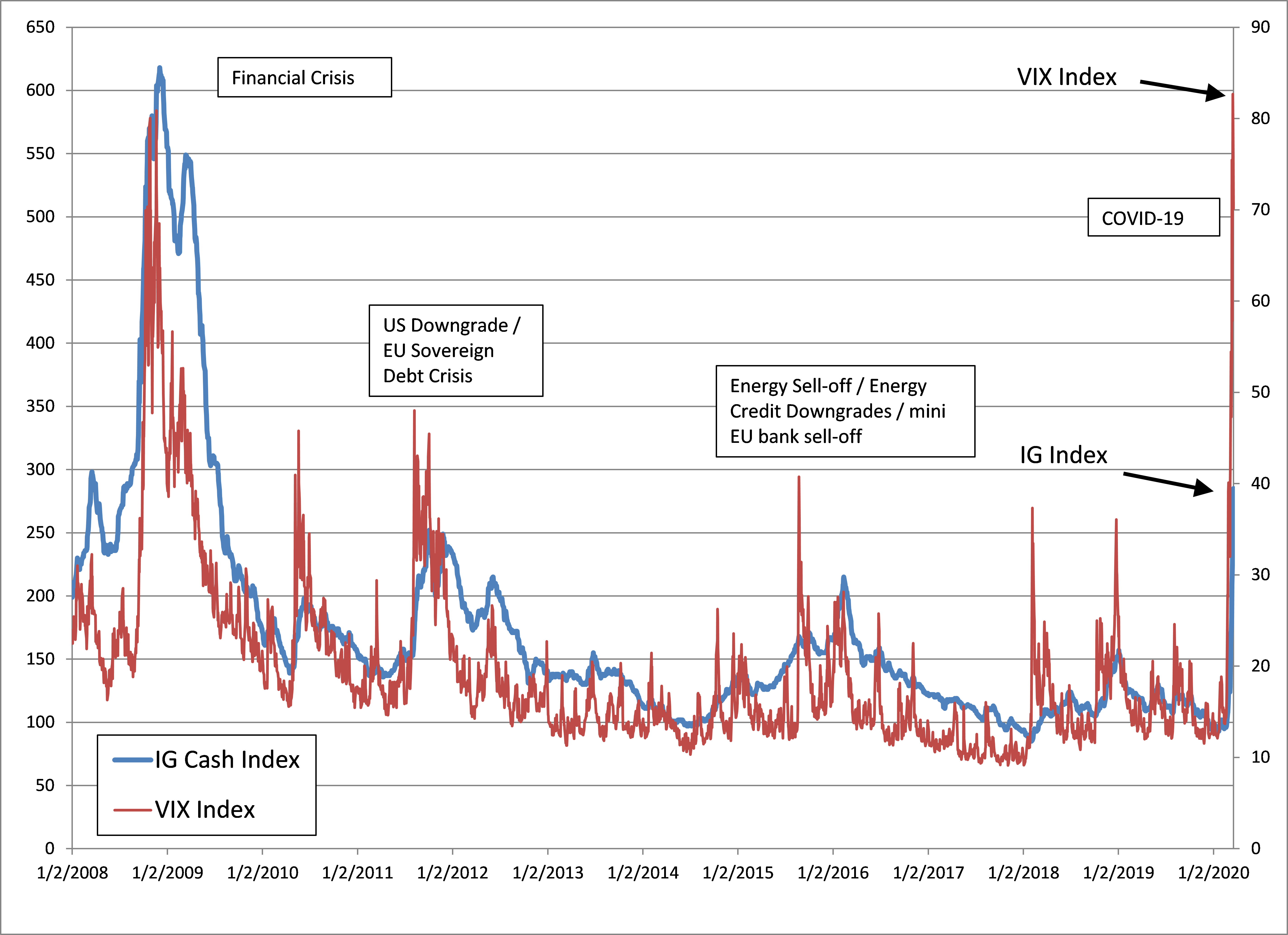

Exhibit 4: Corporate Bond Spreads vs VIX Index (historic)

Source: Bloomberg/Barclays Corp Agg Index, CBOE Volatility Index, Amherst Pierpont Securities

Source: Bloomberg/Barclays Agg Index, Amherst Pierpont Securities

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.