Uncategorized

A historic rush to cash

admin | March 20, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

The list of historic efforts to address coronavirus and its impact on economies and markets seems to grow almost daily. Central banks have signaled almost no limits, if necessary, to deploying their firepower. Fiscal policy is starting to wind up. Rather than a crisis of monetary policy, however, it increasingly looks like a crisis of confidence in the credit of acutely distressed borrowers—both companies and individuals. Connecting dots across markets, these borrowers seem to be making a historic rush into cash.

The crunch is coming from a sudden stop in economic activity around the world. Quarantines and social distancing have cut off businesses that could be viable once the coronavirus pandemic passes. Transportation, restaurants and bars, theater and entertainment, retail shopping and a long list of other business will likely see revenues evaporate. Our chief economist, Stephen Stanley, estimates that US GDP in the second quarter could drop by an annualized 11%, with other economists projecting drops of more than twice that amount. But these same forecasts anticipate sharp rebounds later in the year. The businesses most affected by coronavirus are just trying to make it through the revenue desert. They are out looking for a cool, clear stream of cash.

Unfortunately, monetary policy is ill-equipped to meet the needs of temporarily distressed but otherwise creditworthy borrowers. Almost no commercial bank, no matter the cost or terms of money, will pass it along to a borrower about to see revenues fall off a cliff. Central bank liquidity is likely pooling in the financial system and on the balance sheet of companies and individuals already equipped to make it through. Distressed businesses and individuals seem to be conserving their own cash and selling everything they can.

Prime money market mutual funds for the week ending March 18 saw net outflows of $85.4 billion while municipal bond money market funds saw net outflows of $5.3 billion. US domestic bond funds for the week ending March 11, the most recent data, saw $32.3 billion in net withdrawals, the most in one week since at least 2007. Municipal bond funds saw $3.1 billion in net withdrawals that week. Only equity funds saw net cash come in the week of March 11. But the big winner has been government money market funds, with net inflows the week ending March 18 of $249.3 billion.

Benchmark corporate issuers still have access to the capital markets and continue to build cash. Berkshire Hathaway, Progressive, Coca Cola, PepsiCo, Disney, UPS and Exxon all launched multi-billion deals within the last week.

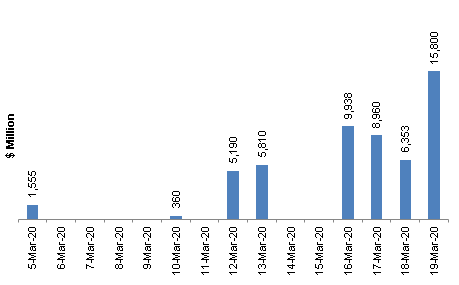

In the $1.2 trillion US leveraged loan market, borrowers have started drawing down bank lines of credit. SEC filings show $54 billion in draws in March alone, with more than three-fourths since March 16 (Exhibit 1). The median leveraged loan made in 2018 and 2019 went to a company with a ratio of earnings to interest expense of only 3.5x. A 70% drop in earnings would leave the median company able to cover debt but little else.

Exhibit 2: Leveraged companies have started tapping lines of credit

Note: new draws on lines of credit by SEC-registered borrowers in the leverage loan market. Source: S&P Global Intelligence, Amherst Pierpont Securities

Markets in agency debt, agency MBS, ‘AAA’ CLOs, ‘AAA’ CMBS and other fundamentally sound cash flows have traded in wide and often disorderly markets, presumably a sign that portfolios needing cash have chosen to sell whatever can be sold most easily.

Despite calls to equip the Fed to buy corporate debt and possibly other assets, the market still faces the challenge of getting cash to temporarily distressed but otherwise creditworthy borrowers. Federal governments should consider guarantees on emergency bank loans to these borrowers. The federal guarantee solves the problem of lending to a temporarily distressed borrower. The commercial banking sector has relationships with many of these borrowers and often knows their balance sheets well. The banks could determine creditworthiness based on 2019 or other trailing financials. And bank regulators, already in place, could monitor execution of the program. The banking system becomes an efficient channel for distributing relief.

The visible toll of economic damage already underway only looks likely to rise in the coming weeks and months. Demand for cash should continue, and markets should remain volatile.

Investors with the luxury of ample cash on hand have opportunities to buy fundamentally sound cash flows at often historically wide spreads. Beyond cash flows guaranteed by governments or federal agencies, a range of public and private issuers have enough cash to make it through this crisis and come out on the other side stronger. That is exactly what every liquid investor should be looking for now.

* * *

The view in rates

The current 0.85% rate on 10-year Treasury debt implies an average real rate of 9 bp and inflation of 76 bp. Futures now imply policy rates at zero-bound for at least the next year. Fed policy is likely to only get more pronounced unless fiscal policy gets traction. Given the tremendous monetary and fiscal stimulus working its way into the economy, a quick ebb in the coronavirus pandemic should threaten the rates market with visions of inflation and continue to sharply steepen the yield curve.

The view in spreads

Spread products remain almost complete at the whim of demand for liquidity. Eventually, portfolios with cash will begin buying fundamentally sound cash flows at wide spreads. That should start the process of returning some order and a framework for relative value to the market.

The view in credit

The immediate risk in credit is from companies with high fixed costs and a sharp drop in revenue from current efforts to avoid coronavirus infection. Companies with the highest leverage are first in line. Until the arrival of pandemic, the consumer balance sheet has been extremely strong. The coming sharp rise in unemployment should change that.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.