Uncategorized

A farewell to LIBOR ARMs

admin | February 7, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Fannie and Freddie have drawn the first line in the sand for the transition from LIBOR to SOFR. The market for new agency single-family and multi-family LIBOR ARMs will be replaced by one for SOFR ARMs by year-end 2020. The transition from a forward-looking unsecured term rate to a nearly risk-free average of an overnight rate requires some adjustments. Single-family SOFR-based ARMs will have shorter resets, lower periodic caps and wider margins than their LIBOR-based forbears. Multi-family SOFR ARMs have an additional hurdle to clear – they depend crucially on the successful development of the still nascent SOFR futures market.

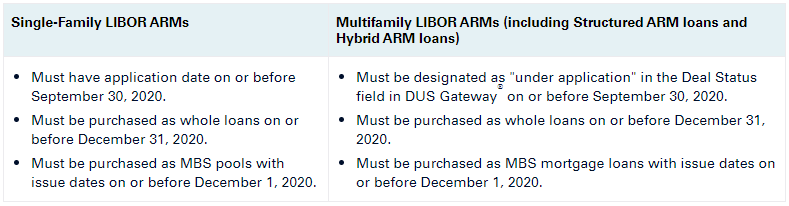

As part of the ongoing transition from LIBOR to SOFR, Fannie and Freddie recently announced that they will quit accepting loan applications and acquiring single-family and multifamily LIBOR ARMs by year-end 2020 (Exhibit 1). Both agencies plan to begin accepting applications and purchasing SOFR-indexed ARM loans sometime in the second half of this year. Originators and borrowers wary of SOFR will not find a safe harbor in CMT-based loans for long. The FHFA has issued guidance that Fannie and Freddie will also cease purchasing single-family CMT-indexed ARM loans sometime in 2021.

Exhibit 1: Transition deadlines for phase-out of LIBOR ARMs

Source: Fannie Mae

Structuring a single-family SOFR-based ARM

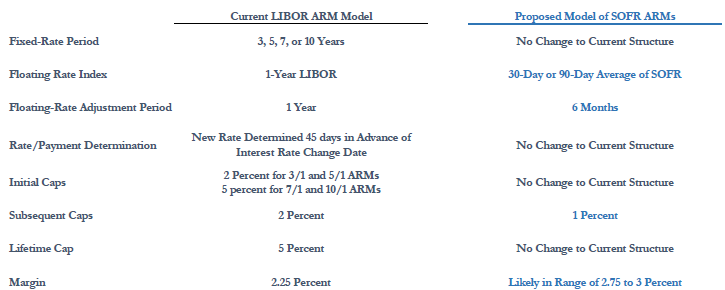

ARRC published a summary table of proposed models for SOFR ARMs in its whitepaper Options for Using SOFR in Adjustable Rate Mortgages, published July 2019 (Exhibit 2). These recommended adjustments have been adopted by Fannie and Freddie in its new SOFR ARMs.

Exhibit 2: Summary of the proposed models of SOFR ARMs

Source: ARRC whitepaper of July 2019

These adjustments are designed to satisfy ARRC’s guiding principles outlined for consumer loan products. In a nutshell the new SOFR-based ARMs are designed to be attractive, easily understood and ensure transparent outcomes to both borrowers and investors; provide a product that is fair, consistent and competitive with existing LIBOR-based ARMs; and minimize disruptions, disputes and basis risk during the transition from LIBOR to SOFR.

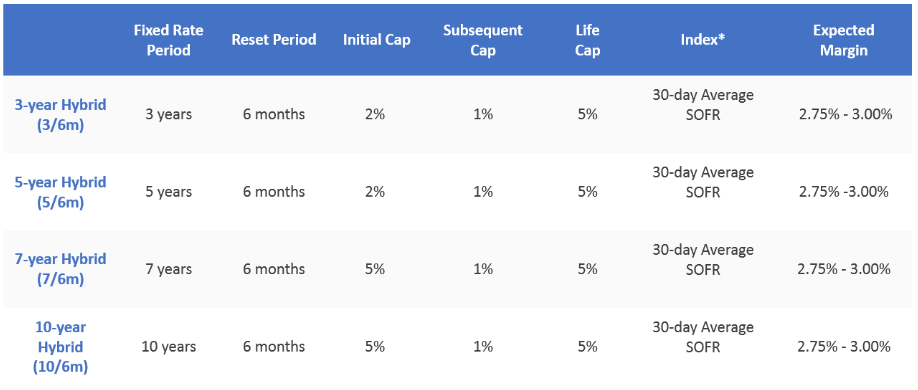

Features of the new agency-eligible SOFR-based ARMs are outlined in Exhibit 3. Not surprisingly, the adjustments adopted by Fannie and Freddie in its new SOFR ARMs are consistent with the ARRC recommendations.

Exhibit 3: New single-family SOFR-based ARM features

Note: The index is an average as calculated and published by the Federal Reserve Bank of New York. Source: Freddie Mac

The hybrid structures of SOFR-based ARMS are like those of existing LIBOR-based ARMs, with a defined 3-, 5-, 7- or 10-year fixed rate period, after which the loan converts to floating-rate for the remaining term to maturity. Adjustments made to the SOFR-based ARMs include the shorter floating-rate reset periods, lower periodic caps and wider expected margins compared to existing LIBOR-indexed ARMs.

Setting SOFR in advance of the coupon period

Although not specifically mentioned in the new offering features, presumably the 30-day SOFR average will be set in advance of the payment period, consistent with how coupons are set in current LIBOR-indexed ARMs. Using an in arrears method, where the floating-rate payments are based on averages of SOFR that occur during the current interest period, was judged inappropriate for consumer products and inconsistent with consumer regulations because it would provide very short notice of payment changes. The in advance method will use the SOFR average observed before the current interest period begins, so servicers can provide the required notice of payment changes to the borrower well ahead of the payment due date.

In this context in advance and in arrears refer only to whether the interest rate is set prior to the start of the coupon period, or just before the coupon period is over. It does not refer to whether the interest rate itself is forward-looking like 1-year LIBOR, or backward-looking like a 30-day average of overnight SOFR. ARRC acknowledges in its whitepaper that it would be more consistent to use an in arrears method with a backward-looking rate, but stakeholders agreed that it was contrary to consumer regulations to notify borrowers of a payment change only a few days before it was due.

Shortening the reset period and lowering the periodic caps

Existing agency LIBOR-based ARMs typically have a 1-year reset during the floating-rate period, while SOFR-indexed ARMS will reset every 6 months. The shorter reset period is an attempt to mitigate some of the potential mismatch when shifting from the forward-looking 12-month term LIBOR rate to a 30-day average of backward-looking overnight SOFR. Increasing the reset frequency is preferable for lenders and investors who need to manage funding and interest rate risk, so the loans will more quickly incorporate changes in market interest rates, expectations of future rates, the outlook for inflation and other macroeconomic conditions.

Borrowers still have the coupons set in advance so there is certainty regarding future payments, and the semiannual adjustment should marginally result in a lower initial rate. The more frequent reset allows the periodic adjustment cap for SOFR ARMs to drop to 1 percent, compared to the standard 2 percent periodic cap for agency LIBOR-based ARMS that reset annually. Based on historical analysis, ARRC concluded that these changes would result in SOFR ARMs having less volatility in the floating rate coupons and frequently lower payments for consumers compared to LIBOR-based ARMs.

Increasing the margin

Single-family conventional ARMs linked to 1-year LIBOR typically have a margin of 225 bp, whereas the standard margin for ARMS based on 1-year CMT is 275 bp. The difference in the margin is to account for differences in the levels of the two indices. Historical analysis showed that on average SOFR-based ARMs with margins in the range of 275 to 300 bp would have resulted in the loans resetting to a rate approximately equivalent to that of current products.

Multifamily SOFR-based ARMs

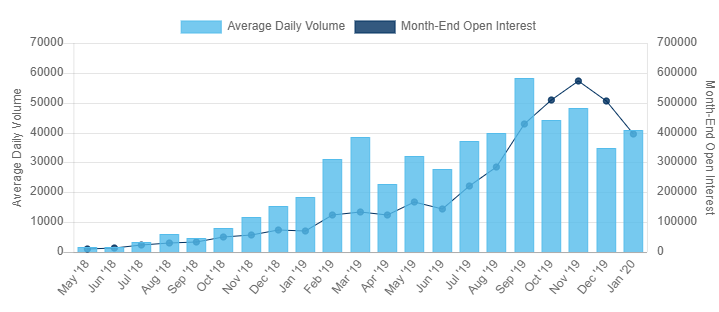

There is not a standard configuration for multifamily LIBOR-based ARMs, and neither GSE has released any detailed specifications or documents covering the product. The announced phase-out of multifamily LIBOR-based loans is intended to occur on the same timeline, but the transition to multifamily SOFR-based ARMs is significantly more complex. Multifamily floating-rate loans require the borrower to purchase the index rate caps themselves and deliver them to the lender. Currently SOFR-based derivatives are still a nascent market. SOFR futures are building in liquidity but average daily trading volumes and open interest (Exhibit 4) are miniscule compared to Eurodollar and Treasury futures.

Exhibit 4: SOFR futures (1-month and 3-month)

Source: CME

Reasonable pricing of long-dated SOFR interest rate caps depends crucially on the development of robust forward-looking and term SOFR rates. It will be a significant challenge to financial market participants and interest rate derivatives desks in particular to build and test the scaffolding before year-end so that agency multifamily borrowers have a SOFR-based ARM option when LIBOR-based ARMs disappear.