Uncategorized

GE operating turnaround mostly priced in

admin | January 31, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

General Electric (GE) beat 4Q19 and FY2019 earnings estimates, though the most important headline was the reported recovery in operating results across their core business lines, including a return to profitability for the beleaguered Power unit. The bullish view maintained on the GE recovery throughout much of the past year was further rewarded as the stock surged more than 10%, and corporate bond spreads were several basis points tighter in the two days that followed, aided by a firmer tone in the broader market. Investors overweight the credit should consider moving towards a market weight in anticipation of a flatter overall performance in the name.

Earnings evaluation

GE reported 4Q19 and FY2019 earnings this week with adjusted EPS of $0.21 vs the $0.17 consensus estimate. Management revised their estimate for $2-4 billion of free cash flow for F2020, well ahead of the low $2 billion estimates that analysts held before this quarter’s results. The return to profitability of the Power unit in 4Q19 was balanced by a substantial drop in orders on a year-over-year basis – a sign of its scaled down approach to the challenged business.

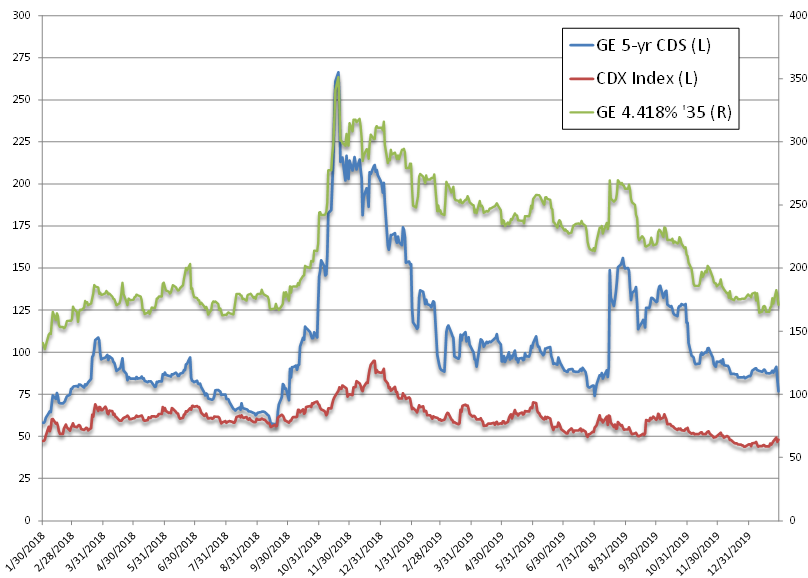

Cash bond and CDS spreads have also recovered sharply since their late August 2019 local wides (Exhibit 1). Execution on asset sales remains the key element for the credit story, but a return to operating success is a critical component to the long-term viability for GE, and the prospect of returning to single-A credit ratings.

Their target of 2.5x leverage remains ambitious, but they reported an improvement of net leverage to 4.2x at year-end 2019 from 4.9x in the prior year, with GE Capital moving to 3.9x from 5.7x on rapid asset dispositions. GE’s revised forecast appears contingent on customer Boeing’s projection for the 737 Max to return to service in mid-2020; for which the aviation unit manufactures the engines and represents a key revenue generator for the segment.

Exhibit 1: GE CDS and cash bond spreads

Source: Bloomberg/TRACE indications only, Amherst Pierpont Securities

Restructuring progress

While the story this week is largely tied to operating success, asset sales related to restructuring have been the important progress recorded to date since their difficulties hit a fever pitch in 2018. Reports emerged yesterday that GE may be close to selling their steam power unit, which is tied to the disastrous Alstom acquisition of 2015 that touched off many of its current challenges.

The Company’s core targets that have been in place since 2018, when Larry Culp was appointed as the new CEO, are as follows: $25 billion in net debt reduction, $15 billion cash balance, <2.5x leverage (A ratings), and for GECC $10 billion in asset reductions and 4x leverage. As stated above, they hit the latter targets for GECC, aided most recently by the $3.6 billion PK AirFinance sale to Apollo. Previous sales include: the Baker Hughes (BHGE) stake for $3.7 billion, the Wabtec stake – $2.9 billion, Appliances businesses to Haier ($4.8 billion in 2016), Water & Process business to Suez for ($3.1 billion in 2017), Industrial Solutions business to ABB ($2.3 billion in 2018). Some more recent smaller sales included Equity Energy Assets to APO (amount unknown), Solar Energy Assets (amount unknown), MRA Systems ($500 million), GE Ventures (amount unknown), and Healthcare Equip ($1.5 billion).

Paramount to the fate of the GE’s restructuring has been the healthcare business, which GE was first considering to spin-off in its entirety in cancelled move announced June 2018, which was hoping to achieve 20% to debt reduction, 80% to shareholders. Instead, GE chose to sell its BioPharma unit to DHR for $21.4 billion in a deal announced in February of last year. The deal is now expected to close by the end of the first quarter, and will provide the bulk of the heavy lifting when executed. Also off the table appears to be reports of a potential sale of the roughly $40 billion aircraft business, GECAS. Management has repeatedly shot down the prospect of a sale, despite rumors about APO coordinating a bid last year, as it is often viewed as the crown jewel of the few remaining components of the old GE Capital.

Though GECC has been in wind-down since 2015, potential charges remain an uncertainty for the credit. Management took a $15 reserve build last year that felt as though it had addressed many of its legacy issues, but there is no certainty regarding their legacy insurance exposures and the prospect of poor reserve development leading to additional charges. GE provided some guidance in that regard last March, but it was a bit murky. Within the remaining insurance book, 60% of LTC book is individual (vs group) and the company maintains about $30 billion statutory reserves for LTC, $46 billion total. On the plus side, GE benefits from a recent account change, which could potentially curb charges from the legacy insurance operations until next year, giving them additional time to execute before potentially disappointing investors again.

Bottom-line for bondholders

As GE comes closer to the final sale of the BioPharma unit, and subsequent debt reduction, much of the juice has been squeezed out of the GE trade that was available in late 2019. There isn’t currently much risk premium over the previous spread levels available ahead of the emergence of GE’s biggest fundamental problems (in 2018). Investors that have been overweighting the credit since last year should consider moving down to a more market weight posture in anticipation of a flatter overall performance in the name, and recognizing the prospect for negative headlines in the quarters ahead. There likely is some tightening still to be experienced on the final execution of the big healthcare sale, but it does appear much of it is already priced in.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.