Uncategorized

As Ginnie Mae II prices collapse, opportunity knocks

admin | January 24, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Price spreads between Ginnie Mae II MBS and UMBS have collapsed lately, driven by fears of increasingly fast Ginnie Mae prepayment speeds. A substantial pipeline of FHA and VA loans looks set to become very refinanceable in the next few months, pushing speeds up and MBS carry down sharply. Ginnie Mae II coupons may have repriced fairly with the exception of 1 WALA 3.0%s. Those pools trade at a price premium to TBA of around 1/32 and have a much lower likelihood of accelerating. And for extra protection, 1 WALA 3.0%s pools with 0% VA work well, too.

Price spreads between Ginnie Mae’s and UMBS have collapsed

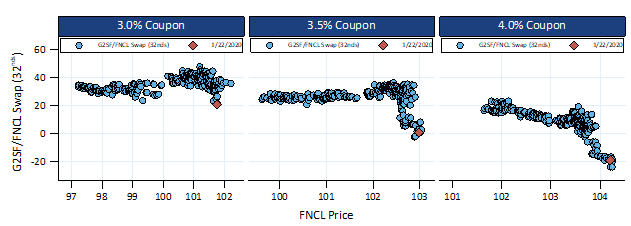

Since November the price spread between Ginnie Mae II and UMBS 30-year pools has plummeted. For example, the spread on 3.0%s has fallen roughly 17/32s since the end of November with the price spread on 3.5%s down nearly 30/32s and 4.0%s down 28/32s. The swaps in 3.0%s, 3.5%s and 4.0%s are all well below levels seen over the last year even after adjusting for dollar price (Exhibit 1).

Exhibit 1: Price spreads have dropped to the lowest level since the start of 2019

For each coupon the exhibit shows the price spread between Ginnie Mae II TBA and Fannie Mae TBA (Ginnie Mae minus Fannie Mae) against the price of the Fannie TBA. The data run from the start of 2019 until January 22, 2020, which is marked as a red diamond. Source: Fannie Mae, Freddie Mac, Ginnie Mae, eMBS, Amherst Pierpont Securities

Fear of increasingly fast Ginnie prepayment speeds is hurting Ginnie prices

Ginnie Mae MBS in the last few months have shown much worse convexity than conventional MBS. Both the FHA and VA offer easy-to-use low-cost streamlined refinancing. VA borrowers are especially prone to refinance, since they tend to have much better credit than the typical FHA borrower and are more likely to take advantage of refinancing opportunities. Neither GSE offers a streamlined refinance program. In some cases the appraisal can be re-used or potentially waived, but this is not nearly as beneficial as the two government programs.

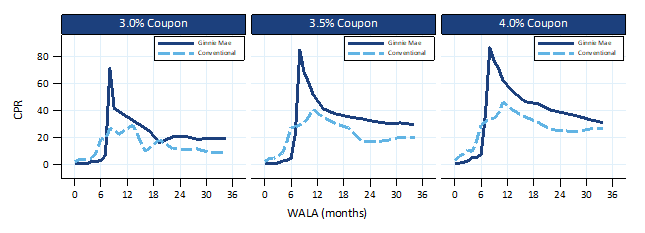

Seasoning ramps from the January prepayment report, reflecting December prepayment speeds, illustrate how much faster Ginnie Mae pools are prepaying than conventional pools (Exhibit 2). FHA loans cannot use streamline refinancing for at least six months after origination, while VA loans cannot use any VA refinance program for at least seven months after origination. Ginnie Mae MBS prepayment speeds on pools with more than six or seven months of seasoning spiked in December above 80 CPR while speeds on comparable conventional pools didn’t exceed 40 CPR.

Exhibit 2: Ginnie Mae pools prepay much faster than conventionals after 6 to 7 WALA

Source: Fannie Mae, Freddie Mac, Ginnie Mae, eMBS, Amherst Pierpont Securities

Ginnie Mae speeds also tend to be slower than conventional MBS before seasoning six to seven months. Conventional lenders typically attempt to prevent refinancing at low WALAs but their methods are less effective than the FHA’s and VA’s. For example, a bank might prevent their employees from refinancing a loan before six months of seasoning. However, that same bank can’t easily enforce that requirement on a correspondent lender or broker; these third-party originators could process the refinance through a different lender to bypass any restrictions. Or the borrower could work with a different lender. However, in Ginnie Mae MBS the restriction is enforced by the FHA or VA, and the agency knows whether or not the original loan is eligible to refinance even if the lender is different. Therefore, at very low WALAs Ginnie Mae MBS actually prepay more slowly than conventional.

A large amount of Ginnie production is about to become very refinanceable

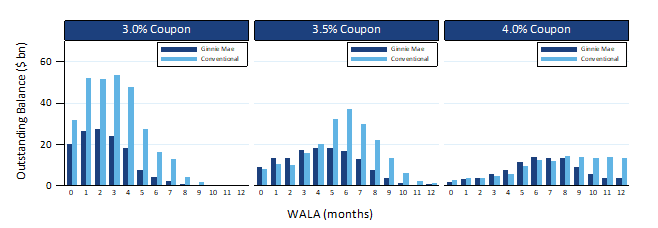

Since interest rates fell throughout most of 2019, many loans came to market in the middle and latter half of the year. So a large amount of Ginnie Mae MBS has not yet seasoned enough to be refinanced, but it is moving into a potential refinancing window over the next few months (Exhibit 3).

Exhibit 3: Many Ginnie Mae pools have not seasoned into the prime refinancing window

Fixed 30 year loans in Ginnie Mae, Fannie Mae, and Freddie Mac pools. Prepayment speeds are from December 2019. Source: Fannie Mae, Freddie Mac, Ginnie Mae, eMBS, Amherst Pierpont Securities

Some loans in Ginnie 3.5%s and 4.0%s have seasoned out of the refinance restrictions, which is why prepayment speeds have picked up relative to conventionals over the last few months. But many more loans are still less than six WALA, and the pending increase in speeds is weighing on TBA price spreads compared to conventional MBS. In conventionals, however, a far greater share of loans have already seasoned enough to easily refinance, so there is less risk of faster prepayments as the remaining loans season and therefore less pressure on prices.

In 3.0%s very few Ginnie Mae loans have seasoned enough to be able to refinance. The drop in the coupon swap represents investors pricing the risk of faster prepayment speeds, but the probability of faster speeds in this coupon may not be that high. The seasoning ramp suggests that 3.0%s will spike after 6 WALA, but they won’t reach the same levels as higher coupons unless interest rates also drop. Ginnie 2.5% production has started again but is still only about $5 billion a month, indicating not many borrowers are refinancing into that coupon at current interest rates. VA borrowers also face other hurdles to qualify for a refinance, such as a minimum 50 bp rate reduction. These hurdles might disqualify a 3.0% coupon VA borrower from refinancing. Therefore not many 3.0% borrowers should refinance unless rates fall.

Ginnie Mae II 3.0% pools with 1 WALA could be a sweet spot

An investor buying a 3.0% Ginnie Mae MBS pool at 1 WALA would have almost six months of prepayment protection. And if rates increase then the faster prepayment speeds priced into the coupon may never materialize. And there is the potential for significant upside if the price spread to Fannie Mae MBS returns to historical levels. The pay-up for 1 WALA 3.0%s for January is slightly below 1/32 and for February slightly above 1/32. The small pay-up seems inexpensive for the initial prepayment protection and the potential upside into a sell-off.

Investors that are able to buy Ginnie Mae custom pools, which are not TBA-deliverable, can consider even better convexity paper. For example, pools that do not contain VA loans should have much better convexity than those that do. The 3.0% coupon tends to have a heavier concentration of VA loans, so a 1 WALA 0% VA pool should prepay much better than the 3.0% TBA. These pools tend to trade at lower pay-ups than many other types of call protected collateral, so might be another inexpensive way to benefit from low Ginnie Mae prices.