Uncategorized

Sizing up the Fed’s balance sheet

admin | January 17, 2020

This material is a Marketing Communication and does not constitute Independent Investment Research.

The Federal Reserve took quick action when the repo market started acting up in September, first injecting liquidity through repo operations and then embarking on a campaign to buy Treasury bills to increase reserves. While central bankers have been deliberately vague, the fourth consecutive month of heavy T-bill purchases should refocus attention on the Fed’s targeted size for the balance sheet, and whether a tapering of purchases will have consequences for monetary policy.

The mandate from the FOMC

The New York Fed has its marching orders from the FOMC. As of the October 2019 FOMC meeting, the NY Fed Open Market Desk was directed to buy Treasury bills at least into the second quarter of 2020 “to maintain over time ample reserve balances at or above the level that prevailed in early September 2019.” In addition the Desk was directed to conduct overnight and term RP operations “at least through January of next year to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation.” The guidance was updated at the December FOMC meeting to include scaled-back repo operations through the tax season in April.

The Desk just announced a fourth month’s worth of purchases of $60 billion in Treasury bills to grow the balance sheet. Meanwhile, since year-end, the Desk has only modestly shaved the maximum amount of repo operations on offer, perhaps hoping that as conditions normalize, dealers would simply curtail their bids. However, the outstanding amount of Fed repo operations has yet to shrink markedly.

How big of a balance sheet does the Fed want?

The most important question surrounding these issues is how much the Fed wants to grow the balance sheet. The directive quoted above is quite vague, only committing to keep the balance sheet at least as large as it was in September 2019, when the repo market acted up. However, policymakers clearly want a balance sheet that is substantially larger than that to provide an ample cushion of liquidity for the banking system and money markets.

The sentiment in late 2019 seemed to be that the risks were skewed drastically toward repo market tightness, so that the larger the balance sheet, the better. A few hawks were sounding off about easy monetary policy (both rates and the balance sheet) creating financial stability risks (Fedspeak for bubbles), but most officials seemed content to allow a continuing accumulation of excess reserves. However, comments on January 15 by Dallas Fed President Robert Kaplan, a centrist on the Committee, suggest that concerns may be beginning to build. A growing consensus of financial market participants and analysts are discussing the fact that stock prices have been zooming since the Fed began to grow its balance sheet. While that correlation may be coincidence, it harkens back to a common refrain heard during QE. Kaplan seemed to offer some validity to that argument, noting that “my own view is it (balance sheet growth) is having some effect on risk assets.” He goes on to argue that “I think we’ve done what we need to do up until now. But I think it’s very important that we come up with a plan and communicate a plan for winding this down and tempering balance sheet growth.”

These comments suggest that a growing portion of the FOMC may be beginning to think that it is time to come up with an endgame for balance sheet expansion.

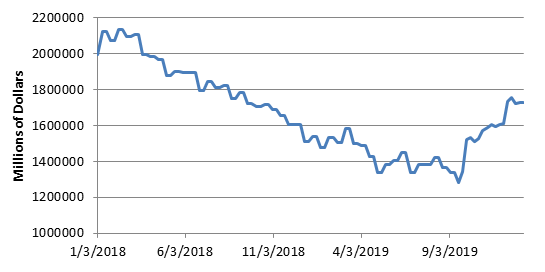

Evolution of the Fed’s balance sheet

As recently as mid-2019, the Fed was still rolling off securities, allowing its balance sheet to shrink. The original plan was to end that approach after September, but the Fed immediately halted balance sheet runoff at the end of July, when it implemented its first rate cut of the year. From there the balance sheet was roughly stable for a short time before the events of September led to the program laid out above. The evolution of the balance sheet can be seen in Exhibit 1.

Exhibit 1: Fed liquidity provision – excess reserves plus outstanding repos

Source: Federal Reserve, Amherst Pierpont Securities calculations.

Excess reserves dwindled from a peak of over $2.7 trillion in 2014 to below $1.4 trillion by mid-2019. An abrupt drop in excess reserves in September led to the repo market debacle. While there were immediate causes for the dip in liquidity in mid-September (Treasury securities settlement and a quarterly corporate income tax payment both drained cash from the banking system on September 16th), there were other medium-term forces that converged as well. The Treasury’s cash balance surged in September once the debt ceiling standoff was resolved, jumping from less than $150 billion in August to $300 billion by mid-September, on its way back to a “normal” range of $350 billion to $400 billion. This also siphoned cash out of the banking system (via a jump in Treasury bill borrowing by the government), as did growth in the Fed’s reverse RP program for foreign official accounts, which expanded by about $50 billion in the months leading up to mid-September. So, it took an unusual confluence of events all pulling cash out of the money markets to create the conditions that led to the alarming spike in repo rates.

By the end of September, the Fed had injected about $170 billion in repo operations, helping to get the money markets back on a firmer footing. By the end of the year, excess reserves had increased by close to $250 billion, mainly reflecting T-bill purchases, and repo operations were adding another $240 billion or so in liquidity. In fact, the combined amount of liquidity, excess reserves plus repos outstanding, ended the year at the highest level since September 2018 (see Exhibit 1).

Where does it end?

The presumed course for Fed liquidity provision in early 2020 is that the repo operations will gradually be scaled back, with the effect on overall liquidity provision neutralized by ongoing Treasury bill buying. What no one knows, including arguably Fed officials, is what the “right” level of excess reserves is. President Kaplan has introduced a consideration that had not been expressed by anyone outside of the hawkish minority of the FOMC before – that the balance sheet could become too big, i.e. the Fed could provide too much liquidity and stoke frothy asset valuations. Does the economy really need the current level of Fed liquidity, about $400 billion more than the readings during the late summer, for money markets to behave?

If the answer is “yes,” then the Fed will need to keep buying Treasury bills for several more months, as it will need to grow excess reserves by enough to offset the shrinkage of its repo footprint. If the Fed’s repos outstanding shrink from the recent $240 billion down to, say, $50 billion on a sustained basis, then the Fed would need to buy about $190 billion more in Treasuries to keep the overall liquidity levels steady. Coincidentally, three more months of $60 billion per month would more or less match that need, which would imply a continuation of the current buying pace through April, matching the expectations of many market participants.

My personal sense is that such a big step-up in liquidity might prove excessive, but I suspect that the Fed will err on the side of too much, rather than too little, cash in the system to avoid a repeat of mid-September. After all, the Fed can easily shrink the balance sheet if it sees the need, as it proved from 2017 to 2019.

Flows vs. levels

There was an ongoing debate during the multiple rounds of QE about whether the impetus for economic growth and/or the provision of financial stimulus came from the level of the Fed’s balance sheet or the pace of new purchases. Most Fed officials, drawing on the academic literature, argued that the level of the balance sheet was the most important factor, but market participants tend to focus more on flows. This question becomes important again if you believe that the recent liquidity provision has had a noticeable impact on asset valuations. Does the stimulus wane as soon as the pace of buying begins to slow? For example, does a modest taper in Treasury bill purchases, say from $60 billion per month to $50 billion, constitute a modest reduction in the degree to which the Fed is stimulating or does it represent a step toward monetary restraint?

If President Kaplan’s view is widely held on the FOMC, then a discussion of tapering could begin as soon as the next meeting at the end of this month, and the directive to the NY Fed Open Market Desk could begin to change as soon as February. Perhaps a slowdown in bill purchases does not occur quite so soon, but it will be operative at some point in 2020. The Fed is highly unlikely to want to grow the level of excess reserves much beyond the current level of combined liquidity (excess reserves plus repos outstanding). If you believe the argument of Chairman Powell and most of the FOMC that the purchases of T-bills has been a purely technical move and has no implication for monetary policy, then the tapering or halt of buying should not impact asset values. However, most market participants and, now, President Kaplan (and perhaps others on the Committee) think otherwise. It is hard to imagine that we could see a 2013-style “taper tantrum” in the Treasury bill market, but weaning the markets off of the heavy injections of liquidity provided over the past few months may not be as straightforward as Fed officials would like.